Honestly, this is a category which I have not completely understood for a long time. So for the last few weeks, I have been trying to research and improve my understanding of the category. This post is an attempt to share my perspectives on this category.

Backdrop

Arbitrage funds pre-tax returns historically has been very close to liquid funds. Hence, till date, I have only used debt funds for all my short-term requirements (less than 5 years).

Source: Value Research as on 08-Sep-2016 – Link

But in recent times, arbitrage funds have been gaining popularity for addressing short-term needs between 1 to 3 years, as they are taxed like an equity fund and hence have zero tax after one year. On the other hand, debt funds (post July 11, 2014 ) have relatively unfavorable taxation as the returns are added to your total income and get taxed as per your current income tax slab for holding periods less than 3 years (after 3 years debt funds are taxed a 20% of inflation adjusted returns).

So given the tax advantage, we need to understand the arbitrage fund category and find out if they can be used as an alternative for debt funds.

How do Arbitrage funds work?

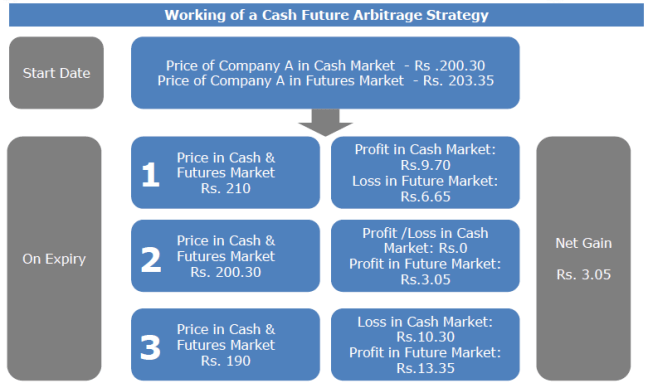

Arbitrage funds generate returns by taking advantage of the difference between the stock price in the cash market and the futures market.

In an arbitrage fund, a particular quantity of a certain stock is bought in the spot market and the same quantity of the same stock is sold in the futures market simultaneously. On the day of expiry of the futures contract, the cash and futures prices coincide, thus generating positive returns for investors. The difference between the cash market price and the futures market price is the return of the arbitrage fund. Since the position is perfectly hedged, any movement in the underlying stock price does not impact the return of the fund.

The returns from an arbitrage fund are thus dependent on the spreads available between the cash and futures position.

Example 1.a

Source: SBI Mutual Fund Presentation

As seen above, irrespective of the direction of the underlying stock price movement, the funds will be able to capture the spreads on the day of expiry (last thursday of every month)

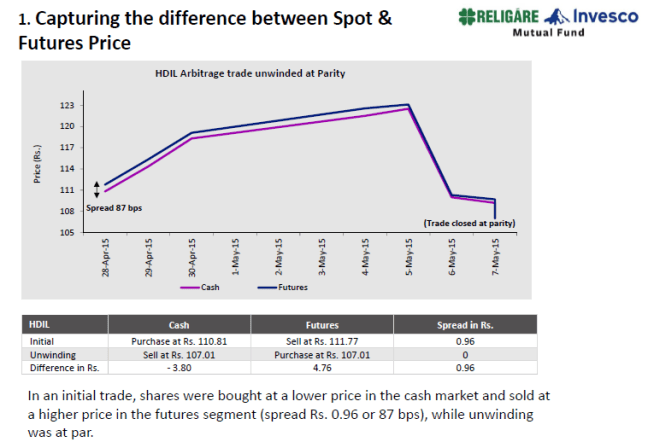

Example 1.b

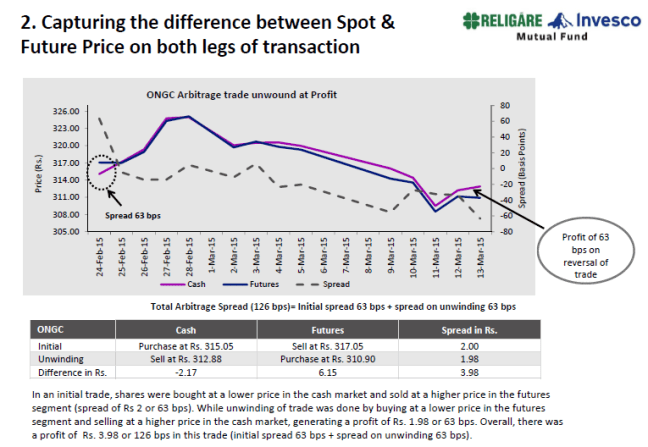

Example 1.c

Source: Invesco Arbitrage Fund Presentation

Source: Invesco Arbitrage Fund Presentation

While I have kept my explanation very basic here as there are several other articles which cover the working of arbitrage funds in detail. So instead of repeating them over here, let me provide a few links which can help us get our basics sorted: Link 1 Link 2 Link 3

So now we have some reasonable understanding of how an arbitrage fund works.

The next key question to answer is

What are the factors which influence the returns of an arbitrage fund?

The return potential of an arbitrage fund basically boils down to the spreads available between the cash and futures position every month

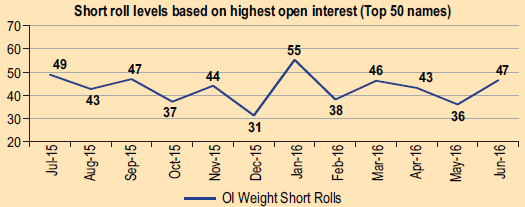

This keeps changing as seen below, based on several factors.

Source: DHFL Pramerica Fund Presentation – Link

(The above chart shows the average short roll spreads of 50 companies

with the highest open interest in the stock futures market for that

particular month)

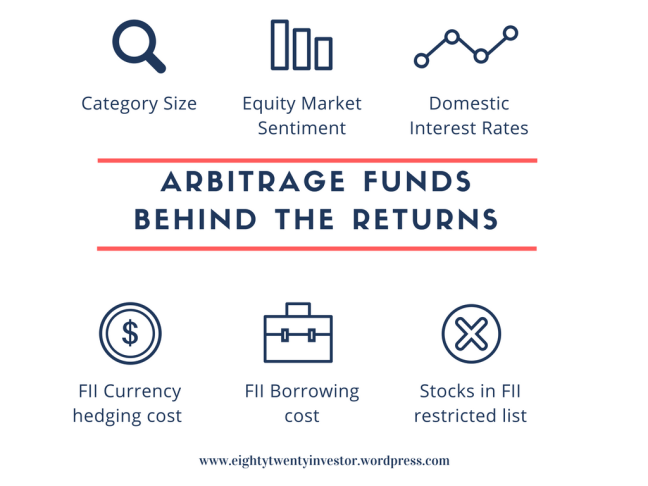

Returns of the funds in the arbitrage category are dependent on spreads and these are in turn impacted by the below 5 factors

- Size of the industry

- Sentiments in equity markets

- Domestic Interest rates

- Currency hedging costs and borrowing costs of FIIs

- Stocks in the FII restricted list

1.The size of the industry

The returns of arbitrage funds is inversely proportional to the size of the industry.

There are a limited number of stocks permitted to trade in the derivatives segment by Securities and Exchange Board of India (SEBI), which in turn means we only have limited set of arbitrage opportunities. So every time the size of arbitrage fund category increases, this puts pressure on the spreads as more money starts chasing the same arbitrage opportunities.

In a way, arbitrage funds suffer from a strange paradox, where if the category does well, it attracts more money and in turn causes the performance to come down!!

Hence every time the category does well we must become cautious and monitor the category size.

As expected, given the tax advantage over debt funds and reasonable past returns, money has started to move into arbitrage funds – which means that at some point in time size will start impacting spreads and hence future returns.

Source: Capitalmind

2.Sentiments in equity markets

Bullish and Range-bound-but-volatile equity markets are generally favorable while bearish equity markets are not favorable for arbitrage funds

Equity arbitrage funds typically do well under these two market conditions:

- Bull markets

- In bullish equity markets – people become very positive on stocks and someone going long on futures has a higher probability of making money. Hence investors are generally willing to pay a higher premium in bull markets. This implies higher spreads which in turn leads to higher return potential for arbitrage funds.

- Range Bound but volatile markets

- Volatile markets allow the arbitrage funds to unwind their trades intra month at a profit and thereby, increase the returns by increasing the churn. Refer to example 1.c for an illustration.

Equity arbitrage funds however will face a problem in:

- Bearish markets

- Since investors have become negative on the stock markets, the futures will generally trade at a lower price compared to the spot market. In this situation, arbitrage funds will not be able to carry on with their usual trade of buying spot and selling future. Since there are restrictions on short selling in the spot market, arbitrage funds cannot execute the reverse trade of “selling the spot and buying in the futures”. Thus arbitrage funds will find it difficult to perform in times of bearish equity markets.

3.Domestic Interest rate

If interest rates decline then arbitrage fund returns also tend to decline

There are 2 reasons

- Investors going long on futures (who are responsible for the premium spread) can now borrow at a lower cost and hence take larger positions with the borrowed money. leading to lower premium in futures

- If interest rates comes down then future debt fund return potential also comes down. But if the arbitrage spreads continue to be high, then money will move from debt funds to arbitrage funds, leading to more money chasing the same arbitrage opportunities and hence eventually leading to lower spreads and returns subsequently.

4.Currency hedging costs and borrowing costs of FIIs

The cost of borrowing and currency hedging cost impact participation of FIIs in the Indian arbitrage segment

In India, debt markets are not completely open to FIIs yet. Hence most of the FIIs use the equity market cash-futures arbitrage option to generate debt like returns. FII proprietary arbitrage books have traditionally formed a significant portion of the arbitrage market in India.

In the last few years, FIIs generally have made around 6-7% return on arbitrage trades and pay around 4-5% currency hedging cost. So, they make around 2% on a net basis. Since this is higher than their borrowing cost, they make money.

So, the cost of borrowing and the currency hedging cost play an important role in determining the extent to which FIIs are active in the arbitrage market.

Whenever currency hedging costs or borrowing costs for FIIs increase, their participation in the Indian arbitrage market will reduce thereby allowing domestic arbitrage funds to take advantage of the arbitrage opportunities.

5.Stocks in the FII restricted list

Trend in increase of FII restricted stocks augurs well for domestic arbitrage funds

Many sectors in India don’t allow 100% foreign ownership and there is generally a ceiling on the extent of FII ownership in the company. As FII’s have continued to increase their exposure in Indian equity markets a lot of these stocks have hit their ceiling limits. Eg HDFC Bank, Lupin etc. Therefore, FIIs cannot take fresh positions in these stocks and as a result, cannot participate in arbitrage trades in these. So, the arbitrage available in these stocks can only be exploited by domestic prop books and domestic mutual funds. Further, these stocks in the FII restricted list provide better spreads than the rest of the market.

Thus, the more the number of stocks in the restricted list, the better the opportunity for domestic arbitrage funds.

In a nutshell

- It is extremely difficult to forecast the returns of arbitrage funds as the returns are impacted by a host of factors:

- Size of the industry

- Interest rates

- Sentiments in equity markets

- Currency hedging cost and borrowing costs of FIIs

- Stocks in the FII restricted list

- Any sudden change in any of these factors can impact the returns of this category in a positive or a negative manner

- Returns from arbitrage funds will never be as linear as a liquid fund

- Returns will generally be a combination of few good and not-so-good months

- Advisable time frame: Greater than 1 year

Parting thoughts on the arbitrage funds vs debt funds debate

Large out performance over liquid funds on a post tax basis should not be expected from arbitrage funds because if that happens even in one month, more money will come into this category which, in turn, will put pressure on the spreads. Sample this – at the end of August 2016 liquid fund category size stood at approximately Rs 3 lakh cr compared to Rs 32,000 cr in arbitrage category. Now you can imagine what will happen if even a small part of liquid funds move to the arbitrage category.

So my sense is that returns for both these categories will remain very close to each other even on a post tax basis (most often with arbitrage funds having slightly higher returns over a 1 year period predominantly due to their tax advantage).

Hence you can continue with either liquid or arbitrage funds or a combination of both based on your comfort and understanding. Since the periods of investing is more than 1 year, even ultra short term funds can be considered (which will provide slightly higher returns over liquid funds).

And if you are wondering about me, given my inability to evaluate the underlying return drivers for an arbitrage fund, I shall continue with my simple liquid fund or ultra short term fund 🙂

As always happy investing folks

Disclaimer: No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments.

Well articulated , thanks.

LikeLike

Thanks a lot for your kind words, Satish

LikeLike

It makes a lot of sense for someone in 30% tax bracket based on personal experience. I have had this (and other UST funds) for last 2 years. Returns are 7.3% and 9.4% for arbitrage and UST. CAGR. So post tax return is still better than UST for me. Want to buy a car in 2 yrs? boom – I park the money here. Best part is that it’s tax free so really easy when filing taxes. One less headache.

Wont recommend for folks in 10-20% brackets.

LikeLike

Thanks for your inputs Gov. I have done a separate post addressing the taxation advantage in arbitrage funds. Do check it out here https://eightytwentyinvestor.wordpress.com/2016/10/27/do-you-know-the-answer-to-the-arbitrage-funds-vs-debt-funds-debate/

LikeLike