Asset Allocation refers to how you split your money between different assets such as equity, debt, gold, real estate etc.

This is probably the single most important decision when it comes to investing. But unfortunately, this decision somehow never gets the required attention.

In fact, academic research demonstrates that approximately 80-90% of your long-term investment returns can be traced back to asset allocation.

The Usual Approach…

Usually when you are asked to decide on your asset allocation, you are shown some variation of 4-5 models with fancy names such as conservative, moderate, aggressive etc. All these models will usually have varying degree of equity exposure with the broad assumption – higher the exposure higher the risk and vice versa.

Here is a rough version:

- Risk Level 1: 10% Equity: 90% Debt

- Risk Level 2: 30% Equity: 70% Debt

- Risk Level 3: 50% Equity: 50% Debt

- Risk Level 4: 70% Equity: 30% Debt

- Risk Level 5: 90% Equity: 10% Debt

Now let us assume you have Rs 1 cr to invest and a 10 year time frame. I will now project the future potential value of your portfolio based on expected returns from equity and debt and ask you to choose what you want.

For eg let us assume 12% for Equity and 6% for Debt over the next 10 years.

- 10% Equity & 90% Debt: 6-7% return expectation i.e ~ Rs 1.8 to 2 crs after 10 years

- 30% Equity & 70% Debt: 7-8% return expectation i.e ~ Rs 2 to 2.2 crs after 10 years

- 50% Equity & 50% Debt: 9-10% return expectation i.e ~ Rs 2.4 to 2.6 crs after 10 years

- 70% Equity: 30% Debt: 10-11% return expectation i.e ~Rs 2.6 to 2.8 crs after 10 years

- 90% Equity: 10% Debt: 11-12% return expectation i.e ~ Rs 2.8 to 3 crs after 10 years

Now what will you pick?

Obviously, the higher return version!

Think about it this way. If you are coming for a weight loss programme and I ask you – Do you want to lose 3 kgs or 5 kgs or 10 kgs or 15 kgs?

What will you answer?

Of course, 15 kgs!

The catch here is that we are being sold only on outcomes.

This is perfectly fine from a marketer’s point of view, who will vouch for the cardinal rule – ‘Never sell the process but sell the outcome’.

But the real problem lies here. Sometimes we forget that, there is a corresponding effort required from our side.

Higher weight loss will also mean we need to put a lot more effort – cutting junk food, eating veggies, regular workouts etc

Most of us recognize this ‘higher effort’ part when it comes to fitness. But when it comes to investing, we conveniently forget this!

In investing, we take the outcomes for granted. It is assumed that if you stay long term and put up with volatility you get the returns. The word “volatility” is little vague and understates the emotional pain and uncertainty that we need to go through.

Outcomes, no doubt are an easier way to make you buy. However, understanding the actual journey and emotional pain that you will have to go through and then deciding on an asset allocation plan will ensure you stick on with the plan and realise the intended outcome!

Thankfully, since I am under no obligation to sell you anything, I would prefer to flip the process and start with helping you understand the journey first and outcome later.

The Eight Twenty Approach to Asset Allocation – TTT Framework

I call my approach the TTT Framework

- Time Frame

- Tolerance to Declines

- Tradeoff

Let us dive into it…

1.Time Frame

The first thing I would like to know is the approximate investment time frame.

The logic is simple:

Debt returns while they provide relatively lower returns over long run, they are stable and consistent over the short term. Equity returns while they have the potential to provide higher long term returns, in shorter time frames their returns can be much lower than debt fund returns or even negative.

So as time frames increase we can have higher allocation to equity.

Why haven’t I included anything above 70% equity?

Over the years, after seeing several clients, I have realized that 80-90-100% equity allocation is extremely difficult to pull off for most of us. Unless you have experienced 2 market cycles and fairly hands on with equity investing, I would suggest at least 30% in debt allocation.

Also when I tested over the last 30 years, in the long run, a 70:30 portfolio with yearly rebalancing, provides returns which is almost on par with a 100% equity allocation.

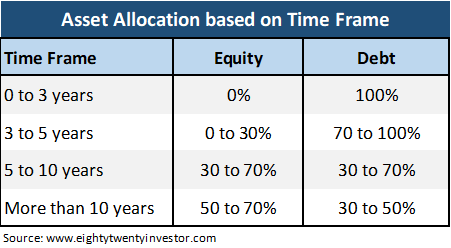

In our example, you have a time frame of around 10 years and hence let us go by the bucket 5-10 years. This implies an allocation between 30% to 70% in equities.

Now how do I decide whether it is 30% or 40% or 50% or 60% or 70%?

Phew! Too many choices and this may paralyze our decision making.

Let us simplify our choices to 30%, 50% and 70%. (for the precision freaks, relax. We will address the 40% and 60% too, but a little later)

2. Tolerance to Declines

Don’t get put off by the fancy jargon. In simple words, the question you need to answer is “What extent of portfolio falls will you be ok with?”

While long term is fine, in reality all of us measure our portfolios in short term. So unless you have a clear understanding of what is ok and what is not ok in the short term, long term returns will just remain a theoretical aspiration.

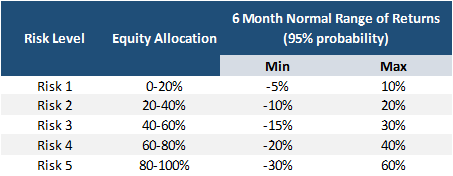

I like to view portfolios in 6 month blocks. So a 10 year period will be viewed as twenty discrete 6 month blocks.

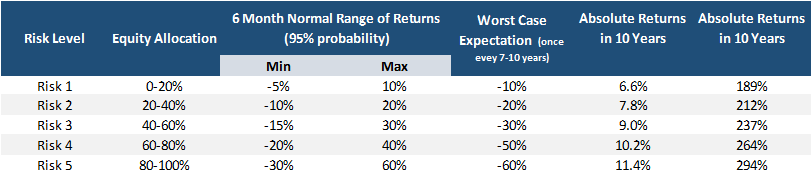

When I went back and looked at long term history of Nifty, I found that 95% of the times the 6 month range of return outcomes were between -27% to 61%.

I also did a similar analysis for different asset allocation ranges and here is how it roughly looks

Cool!

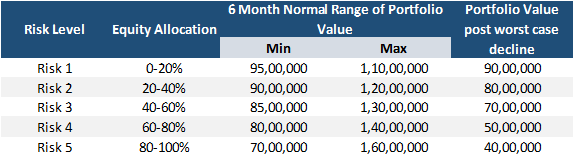

Now let us say you want to choose, Risk 4. For a decline of upto 20% in the next 6 months, or in other words Rs 20 lakhs, you must be like “Nothing to worry. This is exactly what I signed up for!”

If you noticed, I had stealthily used the word “normal”. If you thought 20% is all that you have to tolerate for a Risk 4 asset allocation hang on.

Here comes the killer.

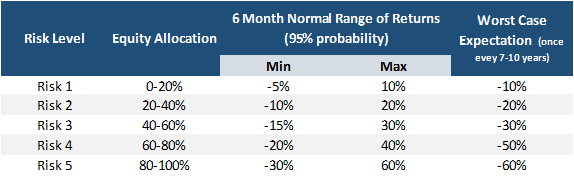

There are also extreme falls (read as bear markets) which usually happen once every 7-10 years. While I have no clue when or what will lead to the next bear market, I am reasonably sure we will definitely see a lot of bear markets in our investing lifetime.

After going through 40 years of Sensex history, the highest equity fall has been around 60% (in the 2008 crash). So as a part of our expectations we must also be ok with suffering a large crash once every 7-10 years. The extent of decline will depend upon the equity allocation as shown below.

Now I need to add one more scarier line to your expectation:

If you choose Risk 4 portfolio, over the next 7-10 years, it is highly likely that your portfolio can temporarily go down upto 50%.

Percentages make it a little less scary. Let me confront you with the reality.

If you choose Risk 4 portfolio, over the next 7-10 years, it is highly likely that your portfolio can temporarily go down upto a whopping Rs 50 lakhs at some point in time.

Would this be ok with you?

Like I mean, seriously, think through those values and what it would mean to you.

At this juncture, you can decide to reduce your expected declines and make your investment journey less painful by moving to Risk Level 3 or Risk Level 2.

Let us assume you have moved down to Risk 3 (i.e 50% Equity Allocation).

You are comfortable with accepting a 15% fall or Rs 15 lakh fall over the next 6 months as normal behavior from the portfolio. Also in the worst case, you are mentally ok putting up with a temporary decline of 30% or Rs 30 lakhs.

Taking into account reality…

While you have chosen your allocation. Let me also remind you of few other realities.

During such falls, usually it takes around 1-3 years to get back to original levels and for the entire period, your portfolio returns may look dismal. Thoughts of “I should have simply stuck to FD”, “Have I done the wrong thing” etc will haunt you and test your faith in the asset allocation that you have chosen. Several experts will call for moving from equity to debt or cash till there is clarity, and will further add fuel to your uncertainty and doubt. As market falls, you will look dumber with each passing day. Your hard earned money will keep going down every day.

Now it is impossible for you to imagine how this really feels and predict whether you will really be able to pull this off. Your past behavior in bear markets is the closest you can get to understand your tolerance to downside.

What did you do in Feb-Mar 2020 when the equity markets fell by ~38%?

If you sold your entire equity allocation: You may be overestimating your tolerance levels. Reduce equity levels by 20% (in our example, you will move from 50% to 30%)

If you sold a part of your equity allocation: You may be overestimating your tolerance levels. Reduce equity levels by 10% (in our example, you will move from 50% to 40%)

Held Steady or Bought more: Your chosen asset allocation is good to go!

Now you have a rough estimate of your asset allocation. Let us move to the final step.

3.Trade-off between risk and returns

Lowering the expected declines in the short term as with everything else in life comes with a long term trade-off – Lower Returns.

Let us put some rough nos to see what do we lose in the long term for a more comfortable short term.

Let us see that as actual nos…

Ah! Now it becomes clear. Our move from Risk 4 to Risk 3 will cost us around Rs 28 lakhs in the future. But that’s fine. This is the cost for reducing our anxiety and sleeping well.

There is no right or wrong answer. The simple idea is to think through the tradeoffs between short term pain and long term returns and pick an allocation which suits you.

While moving back to Risk 4 might seem tempting, the key is that you need to really introspect if you will be able to stay through the journey to enjoy the outcome. This maybe the “paleo diet” version of portfolio for you. Good results but damn tough to follow over the long run.

I hope you got the gist. This is how we come up with an asset allocation decision.

Putting it all together

So here is how your allocation looks

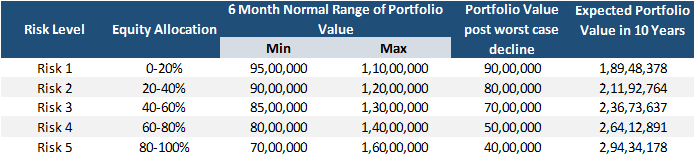

Money you want to invest: Rs 1 cr

Long Term Asset Allocation: Risk Level 3 – Equity 50% + Debt 50%

Expectation (to be revised every 6 months in 1 st week of January and July)

- Next 6 month Return Range which will be considered as normal behavior from your portfolio: -15% to +30% i.e the portfolio value can be anywhere between 85 lakhs to 1.3 crs over the next 6 months

- Worst Case Expectation: -30% decline i.e the portfolio value can be temporarily down to Rs 70 lakhs.

Long Term Return Expectation: ~2.4 crs in 10 years and return expectation around 9% (based on assumptions Equity:12% and Debt:6%)

Summing it up

Our TTT Framework

- Time Frame

- Higher the time frame higher the equity allocation

- Not more than 70% Equity Allocation

- Tolerance for Declines

- Expected Normal Declines

- Expected Worst Case Declines

- Check in actual values and not percentages

- Adjust chosen asset allocation based on past behavior

- Tradeoff between risk and returns

- Understand the long term trade off in returns

Hurray! You have your Asset Allocation ready. With this you have got 80% of your investment plan sorted.

Now before you get too happy, there are three powerful forces out there which will try to get you off your plan – Greed, Fear and Envy. Trust me – it’s extremely tough to resist them.

So we need to have a plan to handle them as well or all this asset allocation mumbo jumbo is of no use.

Ok. But what about valuations? What if equities are damn expensive? What if equities are damn cheap ? Should we still go 50% in equities? How should we invest – all in at one go or should we stagger? How do we rebalance? How to build equity and debt portfolios? How should we reduce risk as we near our goal?

So many questions remain…

No worries, as always, I have got you covered.

Stay tuned and in the coming weeks we will figure a simple way to handle these three enemies and our other questions.

Meanwhile, make sure you subscribe to the blog so that you don’t miss out on the future posts and you get to read them directly in your mail. I won’t spam you and that’s a promise.

Till then, happy investing as always

If you have any feedback you can also mail me at rarun86@gmail.com.

If you loved this post, share it with your friends and don’t forget to subscribe to the blog (1 article per week) or Twitter along with the 8000+ awesome people. Look out for some fresh, super interesting investment insights delivered straight to your inbox.

You can also check out my other articles here

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments.

Very well articulated Arun. Thank you for the write-up.

LikeLike

Very informative article sir, this is more practical approach towards investing. Thanks for sharing.

LikeLike

Nicely written article !

LikeLike

Well Written, Loved concept of risk levels & TTT approach. One question regarding the calculation of final return, 2.4 Cr can be achieved if we maintain the same asset allocation throughout the course of 10 years, but as per first `T` i.e time frame , we need reduce equity allocation during the course and keep to 30-70 mode in the last 3 years , Won’t that reduce the final amount as the interest rate will drop to 7.8% in the last leg?

LikeLike

Great insight. I overlooked this. So will need to make a slight modification. T used can be the actual time frame minus 2 or 3 years ( so that it gives us enough leeway to reduce risk in the last 2-3 years).

LikeLike

Yep, I agree that will be the best plan.

The half yearly review of T -3 year will be the most crucial one I think, we may be up by 30% or down by 30 % that year, In case of latter may have to settle down with a lower amount.

LikeLike

Absolutely great article and practical insight. In theory, we all want best/highest returns but not able to under the risks associated with it and leave the investment journey midway at the first fall/crash of the market. TTT framework is quite good and innovative.

LikeLike

Great article. Investors should read refer this article before investing.This is a more practical approach towards investing.

LikeLike

Thanks Poornima

LikeLike

This article clarifies the 80/20 standard is a reasonable and adequate way. Armature financial backers ought to without a doubt allude to this article prior to beginning their investment journey. Very well curated. A debt of gratitude is in order for sharing.

LikeLike