In our earlier posts, here and here, we found to our dismay that, our natural inclination to choose the top mutual fund performers of the past 1 & 3 years hasn’t worked too well.

That leaves us with the obvious question..

What actually goes wrong when we pick the top funds of the past few years?

The rotating sector winners..

Below is a representation of the best performing sectors year over year. What do you notice?

The sector performance over each and every year varies significantly and the top and bottom sectors keep changing dramatically almost every year.

Sample this:

- 2007 – Metals was the top performer with a whopping 121% annual return

- 2008 – Metals was the bottom performer with a negative 74% returns & FMCG was the top perfomer (-21%)

- 2009 – The tables turned! FMCG was the bottom performer (47%) while Metals was the top performer (234%)

- 2010 – Oops! Metals reversed to become the bottom performer (1%)

- 2012 – IT was the bottom performer (1%)

- 2013 – Reversal of fortunes – IT was the top performer with a huge 55% return

Now if you want to seek some pattern/connection out of this I am afraid it might be a futile attempt. It’s just our pattern seeking brains at work!

The simple takeaway is this: Sectoral winners and losers keep rotating randomly and drastically across short time frames

Thus, when we start picking funds based on their last 1 year return, for the fund manager to get into the top yet again, he/she has to exactly know which will be the new sectors which will be on top for the next year and has to rotate back into them.

This in my opinion, unless the fund manager has some supernatural ability to predict the future, is impossible to pull off consistently year after year.

Going by this, it is natural to expect fund rankings to be extremely random in the short run and hence we must not give too much importance to short term performance.

This brings us to our next question:

If the sector performance of the short run is anyone’s guess. And logically since the long run is nothing but the accumulation of the short run, is selecting funds a huge gamble. How in the world do we evaluate fund managers then?

Understanding Market Cycles

Let us turn to one of the most experienced Indian fund managers for some possible answers.

Now for those, who are running short of time, the gist of what Prashant Jain has to say is:

- Indian stock markets historically has moved in 6-8 year cycles

- Sectoral leadership in the market changed with every cycle

- In every cycle, one or more sectors that were often correlated with each other assumed leadership and vastly outperformed the broad market

- The next cycle then brought with it new leadership

- Between 1995-2016, markets have witnessed 3 broad cycles

- 1995-2000:

IT sector was the leader (stocks up by 96-97x); S&P BSE SENSEX (Sensex) moved from 3,000 to 4,000 - 2001-2007:

Capex/Banking/Commodities/Auto led the market (stocks up by 8 to 30x) (; Sensex moved from 4,000 to 20,000 - 2008-2015:

Pharma/FMCG/Auto were the new leaders (stocks up by 3 to 15x); Sensex moved from 20,000 to 26,000

- 1995-2000:

Source: HDFC Equity Fund presentation

Source: HDFC Equity Fund presentation

You can also read his interview on the same topic here

A similar view is also echoed by another experienced fund manager Sankaran Naren of ICICI Prudential Mutual Fund

“Whenever we raise a toast to outperformers, we tend to forget the role of market cycles. Companies become outperformers because of the sector becoming an outperformer. That part is forgotten by people very often.

In the 1990s, we were in an export cycle. After that, there was a very strong boom in technology. Between 2001 and 2003, there was a lull phase and then from 2003 to 2006, there was a mid-cap cycle, followed by an infrastructure cycle that went on till 2008. Post that we had a consumption rally.”

“When the cycle is on an upswing, it doesn’t really matter if a company is great or not — companies in the sector outperform because of the upturn in the business cycle.”

Source: www.outlookbusiness.com

Now before all this goes over our head, let us try and make some sense out of this..

While it is impossible for the fund manager to get the sector calls right year after year, reasonable long term outperformance can still be provided by fund managers who can broadly position their portfolios for sectors which lead the cycle but at the same time not get carried away by the euphoria and can reasonably transition portfolios across cycles.

Now what does that mean for us?

Short time frames end up capturing only a small part of the cycle and hence it is difficult to evaluate if the fund performance is sustainable as an when the cycle turns.

For past performance to make sense, we need to increase our evaluation periods to cover an entire cycle (i.e not just the bullish phase or bearish phase in isolation). The more the cycles over which we can evaluate the fund manager’s performance the better.

Great..but is it just the sectors that tend to move in cycles??

Even investment styles tend to exhibit cycles..

As seen above, historically in India (and also in other global markets), different investment styles tend to perform at different periods and go through similar cycles as seen in sectors.

You can learn more about this from this video

In the period between 2004-07 moat investing (popularized by Warren Buffet and Charlie Munger) did not work, but instead growth-without-moat worked brilliantly. So naturally funds which did not have growth without moat style, would have suffered.

So in addition to evaluating returns over a complete cycle, we also need to place in context the investment style of the fund manager and ensure that our evaluation period covers an entire cycle from an investment style perspective too.

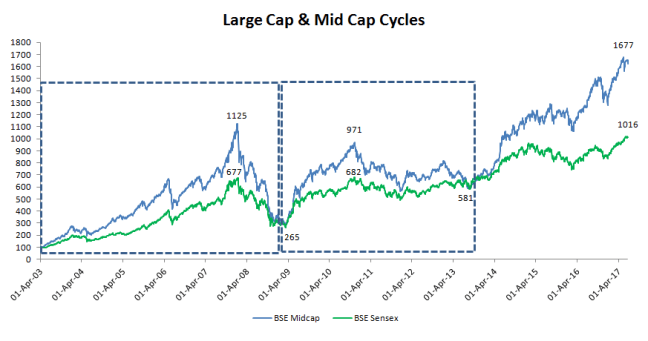

The large cap vs mid cap cycles..

Mid caps (11x) trounced large caps (7x) during the bull run of 2003-07. But the interesting part came post that. For the same investor, in another 1.5 years, the returns of large caps and mid caps stood similar for the period 2003-09..Call it the power of cycles!!

As seen above, large and mid caps tend to converge over cycles, with mid caps outperforming in bullish phases and large caps outperforming in bearish phases.

This again is extremely important when we look at past returns of a fund manager as we have to make sure that our evaluation period covers an entire cycle and not just the bullish or bearish phase.

This becomes extremely relevant in today’s context as most of us tend to prefer mid cap funds based on their last 3-5 year performance. A casual look at the above graph will indicate the trap that we might be getting into. (this deserves a separate post on its own. so will reserve it for another day)

Summing it up..

- The cycles across sector, investment style and market cap segment more or less seem to coincide with the bull and bear phases for most of the periods, as seen from historical evidence

- Returns over short time frames are not a great indicator of future returns as most of the times they only represent performance over a small part of the cycle and the true color of the fund manager is known only when the cycle turns.

- To derive meaningful evidence from a fund/fund manager’s past performance we need to increase our evaluation periods to cover at least an entire cycle (obviously the higher the no of cycles the better)

- Thus while it is impossible for any fund manager to consistently perform over the short term, we can look out for fund managers who are consistent in performing across cycles

- When putting up a portfolio of funds together, we also need to diversify across investment styles (value & growth) and market caps (large & mid caps) as different styles and market cap segments tend to perform over different periods of time.

All this is fine. But how do we exactly define a cycle and how have funds performed across various cycles?

Hang on. We will save that for the next week 🙂

And just in case you like the contents,

Consider subscribing to the blog along with the 1400+ awesome people, so that you don’t miss out on the free weekly investment articles & other interesting updates delivered straight to your inbox.

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments

Very good analysis.For the common investor, who does not know technical analysis like this, how it will be useful to him/her?Which Fund house/fund manager adopted such strategy should also reflect in this article.May be you may cover in your next blog.

LikeLike

Reblogged this on softwaremechanic.

LikeLike

Hello sir! I’m a layperson in the world of finance.

How do I evaluate the fund manager in cycles? As in, how do I know which years should make up a cycle? What should be my starting point of reference and ending point as reference?

LikeLike