In recent times, there has been a significant interest in equity markets thanks to the strong returns of the last few years. The best thing to have happened is the new culture of SIP (systematic investment plan).

Source:AMFI, Link

A SIP is a simple investing process, where you invest a particular amount each and every month regularly. This is extremely convenient as the SIP amounts are automatically debited every month and also coincides with our cash flows (monthly salary). The SIP also supposedly solves the major issue of trying to time the equity markets as the investments are equally spread out and hence average out the ups and downs in the equity market.

All this is good.

But going by the numbers above it looks like a lot of us are entering the equity markets for the first time and SIPs seem to be the preferred route for many.

Given the great returns of recent times, there is a possibility of misplaced expectation if SIPs are not understood or sold properly.

Hence before you jump in, it is extremely important to understand some of the underlying nuances in the SIP concept (which are not generally talked about) so that you end up with a good experience and most importantly decent returns over the long run.

Expectation: I will continue my SIP for 10 years in a few equity funds. Life is taken care!

Here is an interesting article, which explores this question – Link

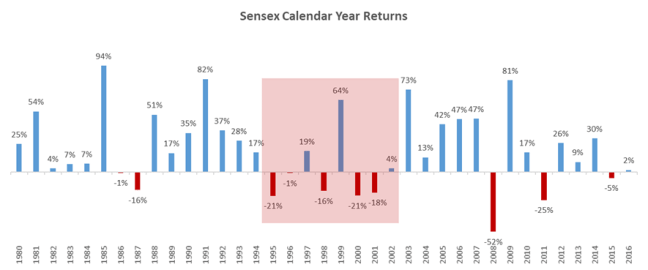

This is the long term 10Y SIP returns for Sensex over different periods as per the article.

And yes, here is the shocker –

There are periods when the Sensex 10Y SIP returns have been negative!

How is that possible?

- Doesn’t an SIP stagger my investments thereby saving me from volatility?

- Isn’t 10 years a reasonably long horizon for equities?

Now before you panic and redeem your SIPs, let us explore this further..

Never forget the underlying equity portfolio

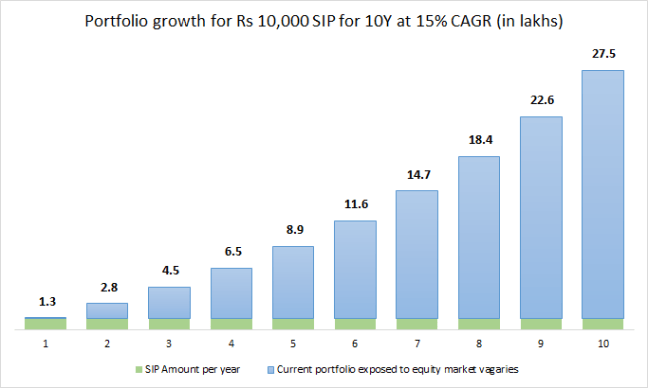

Let us start with an hypothetical example. Assume I invest, Rs 10,000 every month for the next 10 years in a few equity funds and my returns are 15% annualized. This is how my portfolio would have grown.

I end up with around 27.5 lakhs at the end of 10 years.

But what is the blue and green component?

The good part of an SIP is that as we invest our money across several months, even as equity markets go up or down we end up averaging our buying price. And hence the notion that we don’t need to be worried about market ups and downs as the SIP will take care of it and in fact take advantage out of volatility.

A quick glance at the above chart and you know what we are missing.

The green bar represents 1.2 lakh invested via SIP (Rs 10,000*12 months) into our portfolio every year. The blue bar is our overall portfolio which grows in size.

Now the key is to realize that as time progresses, the incremental amount which gets invested via an SIP over a year becomes small compared to the overall portfolio (Sample this – In the above example, the incremental SIP component after the 6th year contributes less than 10% to the existing portfolio).

And hence, while the incremental amount is staggered across 12 months, the existing portfolio is completely exposed to equity markets.

Thus the larger portion of the portfolio will be susceptible to equity market ups and downs in the later years and SIP will have little impact in reducing overall volatility.

Now armed with this simple insight, let us get back to solving the problem of 10Y SIP returns in equities sometimes being low.

Key Insight: The equity market returns in the last 3 years become very critical in a 10Y SIP calculation as almost 50% of the final portfolio value gets created in the last 3 years.

Going by this logic, the periods of low 10Y SIP returns should mostly be the ones where the last 3 year equity returns were dismal.

But nothing like concrete data. So let us check our thesis with actual evidence..

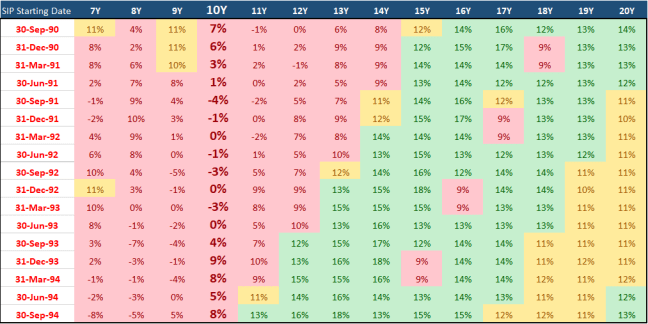

Given below are the SIP returns for different holding periods (7Y to 20Y) in Sensex across different starting dates starting from 1980 till date covering almost 28 years.

The SIP returns below 10% has been shaded in red, 10% to 12% in yellow and above 12% in green.

Now if you are like the rest of us, you must have switched off seeing the complex table above. No worries, just relax, take a deep breath and focus only on the 10Y column. Take a note of all the periods where the returns were lower than 10Y (i.e the ones shaded in red)

You would have noticed that, 10Y SIP returns have been low for investors who started their SIP between mid of 1990 to 1994. Going by our last 3 years being bad logic, most of the returns between 1997 to 2004 must have been really bad for Sensex.

Let us check..

As expected, the returns of Sensex has been poor between 1995 to 2002 – which has led to weak performance in the 10Y SIPs started between 1990 to 1994.

What does this mean for us?

For all those who have started or are planning to start their SIPs now – the Sensex returns of 2025-27 will be the critical determinant of overall returns (the previous 7 years of course do matter but of slightly lower significance).

So at this juncture, don’t break your head over near term concerns of whether the market is expensive or not today as your overall portfolio has not yet been built and your incremental money via an SIP will get averaged out over the ups and downs of equity market..

But what if we end up as the unlucky lot and the returns of 2025-27 goes for a toss?

Unfortunately, we have no way of predicting what will happen to the markets after 7 years.

But, all is not lost..there are a some investors who have actually experienced this situation earlier..Maybe we might find some clues there..

Let us go back and find out what happened to to the unlucky 1990-94 SIP investors.

Now with the benefit of hindsight, what would have been your advice to them?

Let me guess your magic words..

“Boss..Hang on for a few more years”

I know it sounds outrageously simple and dumb. But truth be told it is, perhaps emotionally the most difficult to pull off.

As seen above, the unlucky investors by simply extending their time frame to around 11-15 years, could have reversed their fortunes!

Takeaway: When doing a long term SIP in equities a time frame of 10-15 years is required for reasonable returns (and always be prepared to extend your time frame)

Even if you manage anything above 10% in Sensex, funds managed by good fund managers should be able to provide an outperformance of around 2-4% which implies a 12-14% return which is good enough.

Any other solution?

The other way especially for large portfolios, is to practice asset allocation (i.e allocate between equity, debt and gold and re-balance based on market conditions. This is easier said than done. But no worries I will address them someday in the future.)

Summing it up

- SIP will take advantage of equity market ups and downs only in the initial years, when the underlying equity portfolio is just about getting built

- As years progress, the underlying portfolio in most cases will grow and will be subject to equity market ups and downs

- Even 10Y SIPs can have lower returns as equity market returns in the last 3-4 years have a large bearing on overall returns

- Simple solution is to be prepared to extend your investment time horizon (to around 11-15 years)

- For large portfolios, asset allocation while behaviorally difficult to implement is a great solution (if you have a good advisor to help you out)

Good article! But doesn’t STP often suggested while withdrawing, solves the mentioned issue? “You can not time the market” is as valid at the time of returns as at the time of investing. What do you think?

LikeLike

Very interesting thought. Never occurred to me. Let me work on this and possibly do another post on this. Thanks for your inputs Sainath

LikeLike

Another way to ease this would be to increase your SIP amount by 5 to 10% each year.

LikeLike

The underlying corpus would still be exposed to equity market ups and downs

LikeLike

What an amazing article, with perfect illustrations and simple language. I’m a fan of your work. Please don’t stop educating others like us. Much like the SIPs you will experience tremendous good fortune, in your later years, if you keep up with your writing. Cheers!

PS- I seriously think you have the potential to write in newspapers.

LikeLike

Humbled by your kind words Shiv. Thank you so much for the love and support. Glad that my articles were of some help to you.

LikeLike

Amazingly written with lot of thought and hard work in collating the data.

Asset Allocation is a crazy thing to implement and quite hard to move funds from E to D or vice-versa given the tax implications and the headache of withdrawing to bank and again investing when amounts involved are on the higher side. Is AA the best of the worst approaches and there is no other way out? Will the MF re-classification by SEBI make the job easier?

SIP is the new buzz word and most times buzz words are replaced with new ones. I wonder what would be next!

LikeLike

Will having increasing allocation to Balanced Funds and Dynamic Asset Allocation Funds be a good strategy after 15 years of SIP?

LikeLike

Yes. Increasing dynamic asset allocation funds as portfolio value increases is a good strategy.

LikeLike

Does this mean that the SIP should be continued even after 10 years or let the corpus thus accumulated run for another 4/5 years?

LikeLike

That’s definitely an option. Else if the timelines for the goal is non negotiable, then you need to reduce equity exposure in the last 3-5 years. One option is to move into dynamic equity allocation funds 5 years before the goal ends. The other simpler option is to transfer 20% every year into liquid funds. Also a plain vanilla STP into liquid funds is also an option. You can choose one of these based on your comfort and requirement.

LikeLiked by 1 person