Let me start with a warning. This post is going to be longer than usual and may get a little technical. But trust me, it would be totally worth your time.

Before we start, a little bit of a backdrop story..

Once upon a time..

I had been running asset allocation strategies at my firm for the last few years. Given my inclination towards value investing, in line with most other Indian peers, I was also using a valuation based asset allocation model.

The valuation model was meticulously built after back testing hundreds of different combinations of various valuation and fundamental parameters.

Now while the back test performances were really good (as is obvious to be expected), when you start running these models real time there are some practical problems which is not too obvious in the back tests.

Let us take some time to understand it.

The basic logic behind any valuation model is mean reversion (i.e valuations over long periods of time move in cycles, from high-to-average-to-low-and-again-from-low-to-average-to-high).

Higher the valuation, lower the return that an investor should expect over the long-term and vice versa.

In line with this thought process, majority of value based asset allocation models work by reducing equity at higher valuations and increasing equity at lower valuations.

But here is the catch.

Over the short run,

An overvalued market may become more overvalued

An undervalued market may become more undervalued

Why?

High or low valuations only indicate the degree of investor expectations built in the prices. High expectations can get even higher and low expectations can get even lower.

Thus valuations (read as investor expectations) on its own can’t immediately cause mean reversion.

For mean reversion to happen, the high/low valuations have to meet with an unexpected negative/positive market event which has not been factored in the expectations, yet.

As we all know, the markets are frequented by both negative and positive events regularly. While it is impossible to predict when the event will hit in the near term, as we extend our time frames to 3-5 years, the probability of some negative or positive event hitting the market is very high.

Hence high or low valuations usually predict mean reversion, but over slightly longer time frames.

If you only go by expensive valuations more often than not you will be early and will move out of the markets much before a crash. This means missing out on the rally till mean reversion happens and under performance for some time.

On the same lines, if you go only by cheap valuations you may sometimes be very early in moving into the markets, much before the recovery. This means participating in further falls till mean reversion happens and under performance for some time.

Now if it is your own money, while the wait for mean reversion is emotionally painful, it is still doable. But suddenly when you are managing other people’s money, then it becomes damn difficult.

Day in and day out, you will be questioned on the efficacy of the model, and at some point in time you yourself would start doubting it. The emotional stability and the capacity to suffer needs to be at a different level.

Since most of the clients are acting based on derived conviction, it becomes even harder on their part. Thus as the pressure increases, there is always the danger of tweaking your model – just before the reversal happens.

So, unless and until you have enough experience, proven yourself and are in a position where your firm and clients stand strongly behind you, translating back test results into actual portfolios and most importantly into client portfolios is a tall ask.

Check out what is happening currently to some of the best value investors such as Jeremy Grantham, James Montier, Howard Marks, Prem Watsa, John Hussman etc who have been calling the US markets expensive for some time. Even they have to go through the pain of looking wrong and harsh criticisms till their call comes right.

An easy solution is to move to the “Buy and Hold” stance where you don’t need to take a view on equity valuations. But handling draw downs of 50%-60% is far easier said than done.

Another, straightforward solution could be – a simple asset allocation strategy divided between equity and debt (to reduce volatility) with annual re-balancing back to the same allocation.

But what if there is a better solution which is also a little less difficult for clients to hang on to.

In search of a better solution

In my quest to find out a better solution, I started testing several other combinations of valuation parameters and looked at adding few more fundamental parameters.

But somehow all models had the same issue of being too early. The solution kept eluding me.

And then one fine day, out of the blue, I bumped into this profound Charlie Munger quote:

Wow.

All this while I was trying to improve valuation led models. I had conveniently ignored investors who followed the opposite strategy – the trend following/momentum folks.

Do I know their rationale well enough to disregard them?

This was my Eureka moment!

Enter the world of Momentum and Trend Following

What is momentum?

Momentum is the tendency for assets that have performed well (poorly) in the recent past to continue to perform well (poorly) in the future, at least for a short period of time.

A lot of great folks out there have done some amazing research and published their work.

Evidence

- Avoiding the Big Drawdown with Trend-Following Investment Strategies – Link

- The World’s Longest Trend-Following Backtest – Link

- A Century of Evidence on Trend-Following Investing – Link

- Trends Everywhere – Link

- Why financial trends persist – Link

- Protect, Participate, Managing drawdowns with trend following – Link

Now obviously I don’t expect the majority of you to go through these articles.

No worries the gist is, there is ample evidence across asset classes, across long periods of time, across countries that momentum or trend following provides decent returns with lower drawdowns.

All this is fine. I can guess the question you are itching to ask

Does it work in Indian equity market?

Let us put this to test

I have chosen 3 equity indices: Nifty, Nifty Next 50 and Nifty Midcap 150

The above three broadly cover the majority of Indian market capitalization.

For representing debt, I have considered HDFC Liquid Fund

The strategy would be simple

Each and every month beginning apply these re-balancing rules

- When the last 3 month returns of equity index>3 month return of liquid fund –> move 100% to equity

- When the last 3 month returns of equity index<3 month return of liquid fund –> move 100% to liquid fund

This is called time-series momentum and usually it is done on a look back period in the 3-12 month range globally. In this case I have used 3 months (In Indian context it works better in the range of 3-6 months).

The data has been considered from 01-Apr-2005 (the mid cap index values are available only post this). This period covers around 14 years which is reasonable to test the strategy.

Let us check the results

3 month time series momentum applied to Nifty 50

3 month time series momentum applied to Nifty Next 50

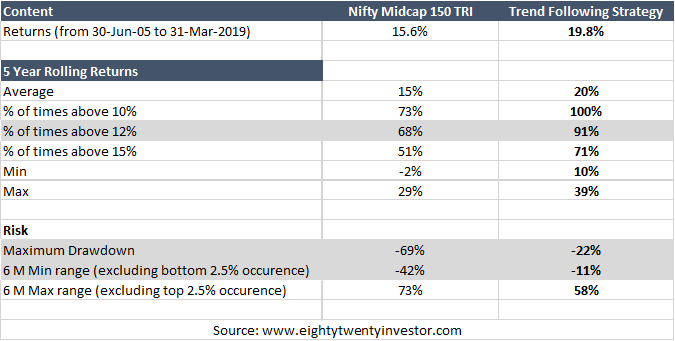

3 month time series momentum applied to Nifty Mid cap 150

While I try to sound nonchalant about this, the results are downright amazing.

The returns have improved and at the same time the drawdowns are also much lower!

Now obviously there are a few things we haven’t considered – like tax, transaction cost, expense ratio etc. Even this can be addressed to a large extent by choosing the right structure (more on that in future posts).

But, before you get all excited and jump into a trend following strategy, hang on. This at the end of the day is a back test. All said and done, my biases how much ever I try will exist and some form of pattern/data fitting possibility is always there.

So the key question you need to ask is

- What explains this outperformance?

- Will the reasons hold on for the future?

Let us explore

Why does momentum work?

Stock markets go up and down in the short run.

But more often than not, their direction is up in the long run.

This statement invokes a very naive yet intuitive question.

“All 40-50% falls don’t happen in a single day. The market usually will have to first fall 5-10% before becoming a larger fall. Similarly huge rallies don’t happen in a single day. The market usually will have to first go up by 5-10% before becoming a large rally. So why don’t we move out (in) of the market as soon as we get the first sign of market fall (market rally)?”

I am sure most of you would have asked this question, the first time you were introduced to the stock markets. Unfortunately, we were cut short by the rude answer.

“True. But the unfortunate part is markets move up and down randomly in the short run. What if after a 10% fall you move out and then the market moves up 5% immediately. You will re-enter at a higher level and hence capture the loss. In the short run, as described by the random walk theory (an academic one) market movement is similar to a drunkard’s walk. So with no patterns, this strategy will mean you will keep losing, a lot of times”

With that our naive market timing strategy was thrown into the dustbin.

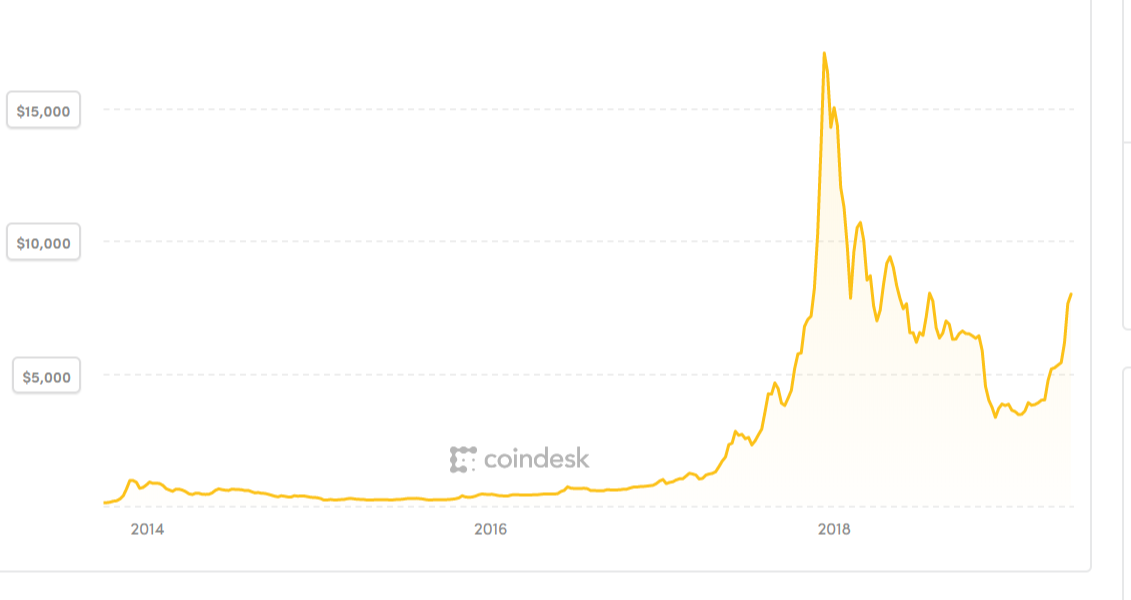

But hey! What if markets were not always walking drunk.

Let us check out the price patterns of Nifty and Bitcoin.

Did you notice a common pattern.

The markets seem to trend both up and down regularly!

A trend occurs when the market keeps moving strongly in a particular direction (either up or down) over a period of time.

The remaining periods they are volatile and range bound.

If you still have your doubts, check out this page for more charts. You can find that trends have existed across asset classes.

Further historical data and research also show that trends have existed pretty much everywhere in financial markets – stocks, bonds, currencies, commodities, etc.

Now we have a part of the answer

If market movements are not drunk always, and for extended periods of time they trend, then our naive “move out (in) of the market as soon as we get the first sign of market fall (market rally)” will work whenever they trend and lose out when the markets become range bound and volatile.

The occasional but large outperformance captured during a trend will compensate for the regular but small underperformance captured during a volatile, range bound market.

So that explains why trend following works.

But wait. You have another question.

Why in the world, do trends exist in the first place? That too across asset classes?

The clue lies in the charts that you saw above.

What is common to all the asset class prices.

Take a guess?

Yup! It’s us – humans.

Our buying and selling drives the prices of all these asset classes. Hence the answer should lie hidden in some of our repeated behavior patterns.

Let us explore this further.

There are two behavioral reasons why markets trend.

Whenever there is a new information or event causing reversal of price direction, investors first under-react and ignore the initial signs of reversal in the market prices. Then as the reversal in price persists, they over-react and herd (buy/sell) into the new direction of price leading to trends.

Why do they first under-react?

Anchoring effect – investors are still anchored to the old trend in prices and are slow to react to new information.

Why do they then overreact?

Herding effect – a positive feedback loop happens where buying and higher prices leads to more buying and selling and lower prices leads to more selling so that trends persist.

Ok, now before you switch off. Let me explain this in a simple manner with an awesome video (no worries, it’s just 3 minutes and I promise you, it will blow your mind)

Did you notice what just happened?

While the video was actually focusing on leadership, there is more to learn about human behavior from it.

Initially it was just one guy dancing like crazy. For sometime no one else was interested to join. This is the “under-reaction” I was talking about.

And suddenly, the second guy joins. This is the tipping point. Soon the third one joins and the momentum begins.

In the next minute, everyone is running like mad to be a part of this dancing crowd. Suddenly it isn’t weird or risky – if they’re quick they can still be part of the ‘in’ crowd, rather than feeling left behind. This is the classic “over-reaction”.

The behavior changes suddenly from one of “under-reaction” to “over-reaction”.

Imagine if you were rewarded a large amount for participating in such movements and penalised a small amount for movements which don’t take off. What would you do?

For example, you may develop a simple rule say, you will join immediately when the no of followers increase to 10. You will exit when the followers decrease by 10.

The idea is that you don’t know which one will end up into a movement. While there will be a large no of false starts where the initial 10+ members are not able to gather momentum, and you will get penalised. This is ok and a part of the plan.

But for the ones which make it into a movement your gains will compensate for the small but regular losses.

Voila! This is exactly what we are attempting via a trend following or momentum strategy to exploit the same human behavior.

Trend followers basically set some rules to indicate that market has started falling or started going up. It maybe 3-12 month absolute return below a threshold, current price above or below the 100 day/200 day moving averages etc.

The beauty of the strategy lies here – since investors under-react at the earlier stages, it provides enough time for the rules to kick in and catch the trend early. (the corollary being if the trend happens super quick, then trend following will be late and miss out the early moves).

“We tend to hang onto our views too long simply because we spent time and effort coming up with those views in the first place. This leads to confirmation bias and an anchoring to strongly held beliefs even if the evidence fails to support them anymore.”

James Montier – The Little Book of Behavioral Investing

Now the most important thing to note here is that: the indicators don’t predict that the markets will definitely move up or down.

They simply work on the innocent logic that that a large upside (downside) will have to start with a small upside(downside).

There will be a lot of false starts where the market suddenly moves up only to fall back and vice versa. This is not a bug. The trend followers will take these small hits as a part of their process.

Whatever they lose in all these false starts (called whipsaws), they make up for it by staying out of a large declining trend and participating in a large upside trend.

Compared to a pure buy and hold investor, trend followers primarily create outperformance during a large bear market.

The intuition is that most bear markets have historically occurred gradually over several months, rather than abruptly over a few days, which allows trend followers an opportunity to move out after the initial market decline and stay away from continued market declines.

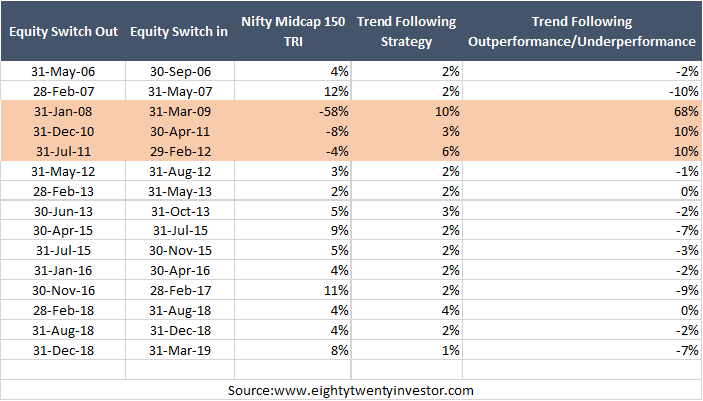

Let us see how this actually works with our earlier example of trend following applied to the Nifty Midcap 150 index.

I have shown all the periods in which trend following has caused us to move out of the index into a liquid fund.

Now it would be clear that trend following gets it wrong regularly (10 out of 15 times) and takes small hits in performance. But as seen it makes up for this during a large fall (3 out of 15 times).

Thus the whole idea is that:

Trend following is not a market timing magical solution. It is a simple intuitive strategy that tries to play on human behavior. It takes on a lot of regular small hits to give the occasional knock out punch!

Since I don’t expect human behavior (herding in response to emotions of greed and fear) to suddenly change in the immediate future I believe trend following is a strategy that will continue to do well even in the future.

Summing it up:

- Trend Following has been endorsed as one of the strongest and most robust factor in financial markets by top academics – many of whom are traditionally skeptical of active management.

- Trend Following strategies have worked across asset classes

- Trend Following strategies have been used effectively by some of the best money managers in the world

- Research has shown that Trend Following has been a durable strategy for over hundreds of years of market history

- Most importantly, a trend following approach can be easily quantified into an objective set of rules that can be easily applied to any investment universe.

- Trend Following can work in the future as it is based on human behavior

- Under-reaction: Anchoring + Confirmation Bias

- Over-reaction: Herding

- Trend Following strategy works in the Indian context!

While the evidence is very strong, I would still prefer to test it out before advising you to invest. In the coming months, I will be personally running a momentum strategy portfolio. I will review and update on how the strategy works in real time.

The idea behind the post, is not to ask you to discard value investing. While value investing works and has got enough coverage, I believe momentum strategies are yet to receive its due. A part of the reason is because the logic as to why it works has not been communicated well which I hope to address with the current post and more posts in the future.

The key intent is to start off a conversation on how we can improve our asset allocation strategies by using trend following/momentum along with value based strategies.

Now for those who survived me till here, let me leave you with an interesting problem to solve.

If you noticed, the trend following strategy assumes every small fall can lead to large fall and hence moves out.

But what if you can train the system to identify periods where a large fall is more likely and use trend following only in those periods?

I did test a solution for this and the results are significantly superior in terms of returns. While the drawdown profile increases its still far lower than a pure equity strategy.

Instead of revealing the strategy which is no fun, I want you to think on how you would approach this problem of training the system to identify periods where a large fall is more likely.

Mail me your thoughts at rarun86@gmail.com. I am always open for a conversation or a coffee:)

I believe given the tax advantages of mutual funds, these type of strategies need to be explored further and provided for Indian investors via different products.

The existing momentum funds are black boxes with hardly any meaningful communication on how they work (SBI and Edelweiss have one fund each).

Hope somebody from the mutual fund space reads this and comes up with an interesting product. You can also reach out to me and I would be super happy to help 🙂

As always happy investing folks 🙂

If you loved this post, share it with your friends and don’t forget to subscribe to the blog via email (1 article per week) or Twitter so that you don’t miss out on future interesting posts.

You can also check out my other articles here

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments.

I think all investment vehicles have their own place. Be it momentum, value, passive using indexes, active using funds, technical analysis etc. The devil is always in the details. How well was the strategy tested? What were the parameters used? What kind of losses/draw downs? How much is your win/loss ratio? What is the risk to reward ratio? etc. One of the most egregious thing an investor can do is take everything on faith and failing to recognize authority bias. For example, people often quote Buffet or Munger without understanding the context/situation. Many use P/E or some metric to calculate under valued companies without understanding the constraints within that calculation.

LikeLike

Yes, Momentum investing is very popular with many good investors. But I think it is game of active investors.

There are not many good index funds in India especially for Midcap Indices.

Arun, What is the way to invest if we go by above article as there is lack of good options for index investing.

Also, do you know any options in smallcase investing for indices.

Expenses like transaction costs, taxes will affect returns too much. Looking forward for your article on how to efficiently do that.

LikeLike

To be honest even I am breaking my head on how to do this efficiently as the taxation would be an issue. Hoping to see some mutual fund come up with something similar.

LikeLike

Interesting analysis. Do let us know how the experiment fares..

LikeLike

The recent super fast market fall due to Corona in the month of March-2020 must have failed professionals momentum investors also. Obviously, a retail investor cannot act in this kind of fall. If one big downfall is not captured, this kind of investing ,it seems, will hugely under perform in the long run.

LikeLike