Recently I had a conversation with a family friend of mine, who also happens to be a CFO in a leading Infrastructure company. Since I was working for a wealth management firm, he casually asked me on how much returns do our clients generally make. I answered “mostly around 12-15%”. For a minute he stood shocked. “What?? Just 12-15% …I thought you guys must be making at least around 30-35% returns for your clients”..It was my turn to be shocked !!

This question serves as an inspiration for this post. Now before we move on, pause for a second and answer this. How much return do you expect from your investments (real estate, stocks or mutual funds or gold etc) for the next 20 to 30 years. Is our current expectation in line with reality? If no, what returns can we reasonably expect from our investments. The following post will try to address these questions. Have you heard about the magic of compounding? I know this concept has been beaten to death, but somehow intuitively most of us tend to find it extremely difficult to appreciate its relevance in our lives. Let’s understand its beauty, by taking an example of someone who expects to make 15% annualized returns.

Compounding formula:

Final value = Invested amount * (1+returns)^no of years

Did you see that!!

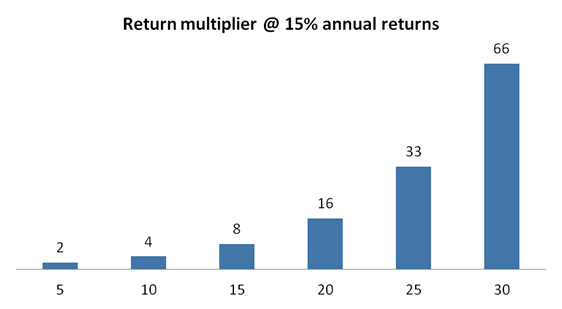

While the effect of 15% returns on your investment is gradual in the initial years the impact magnifies dramatically as your investment period increases.

The logic is pretty simple – you can see that the money approximately doubles every 5 years. As you move past the first 20 years, in the next 5 years your doubling effect is phenomenally magnified given that you already have a 16 times initial amount as your base. Similarly between 25 to 30 years the multiplying effect is doubling on a 33x base which gives you a 66x returns. So as seen, an additional wait of 5 to 10 years brings about a significant change in your final investment value or put in other words, the earlier you start the higher is your future wealth.

Hence the key thing to remember is:

Compounding or the multiplier effect is back ended

To benefit from compounding we need to have 3 things in place:

- Adequate savings to be invested

- A reasonably long time horizon for investing – Start early !!

- Consistently generate superior returns over a long period

For a much better and deeper understanding on the topic, please refer to the link by a brilliant blogger called Jana – https://janav.wordpress.com/2015/10/03/lecture-notes-the-joys-of-compounding/

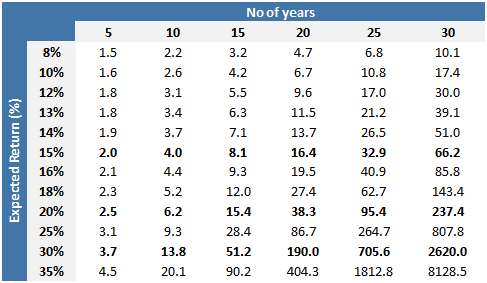

Now that we can appreciate the effect of long term compounding better, let’s go back to the initial conversation that I had. Remember the shock that someone couldn’t earn even 30-35% returns. Now to put that in perspective, if I could consistently earn 30% return, it implies a multiplying effect of 2620 times in the next 30 years or 190 times in the next 20 years. Just take some time to register the impact of these nos. It means if I have 1cr and I can generate 30% returns I am staring at 2,620 cr in 30 years and 190 cr in the nest 20 years. Phew !!

So the next time someone tells you he made 30% or more (blah blah) in a year investing in this land, property, xyz stock etc… Pause. Ask him “Boss..Will you be able to do this for the next 10-20-30 years. Do you have any idea what that means in the long run ?”

The idea is not to conclude that generating high returns (lets say >20%) is not possible. But the fact that generating higher returns consistently over the long term is definitely not easy.

You had also started with some expectations in your mind. Check with the table to appreciate the true long term impact of your expectation. Is it too high? Will you be able to do that consistently over the long term?

While there will be several investments which do well in the short run, what really matters is not the returns we make over a 1 or a 3 year period, but the ability to “consistently “ generate superior returns over a long term. Hence it is extremely important that we do not get carried away by abnormal returns in the short run but rather have a reasonable idea on the long term potential of your investments.

This leaves us with a few questions:

- How do I know if I am setting the bar too high or low with respect to my expectation on future returns?

- How do I put in place a plan to generate “consistent and superior returns” over the long run

- Given my requirement and needs, what is the adequate amount to save and invest?

- Does it require a lot of knowledge and time?

- Is it possible to improve my returns?

(to be continued)