We had earlier explored Fixed Deposits in detail and found to our dismay that F.Ds are a bad way to save our hard earned money as generally post the taxation impact, the returns do not even cover up for inflation.

So let’s look at our next asset class – Fixed Income (which we will be participating through Fixed Income mutual funds also referred to as Debt mutual funds).

This can be viewed as a close replica of a Fixed Deposit but with few important differences.

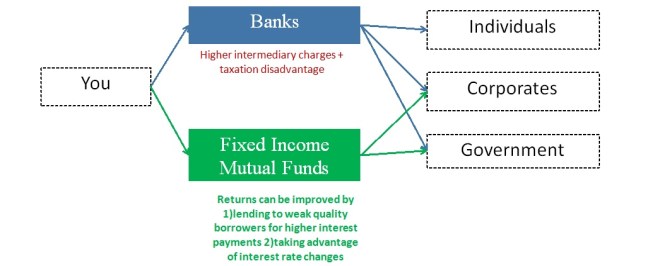

Now at a very basic level, both Fixed Deposits and Debt Mutual Funds are simply intermediaries who connect lenders and borrowers.

Every time you invest in Fixed Deposits or Debt Mutual Funds, you are essentially lending your money. This is extremely important to remember as most of us forget this fact.

This money will be lent to borrowers in need of money such as individuals (only in F.D and not Debt mutual Funds) or companies or government. The interest which the borrowers pay for borrowing the money, is passed back to you after the intermediary (i.e banks or mutual funds) takes the inter-mediation charges.

So in simple terms,

- If the intermediary connecting you and the borrower is a bank it is called Fixed Deposit

- If the intermediary connecting you and the borrower is a mutual fund it is called Debt Mutual Fund

As on 31-Dec-2015, Source: Crisil

As on 31-Dec-2015, Source: Crisil

You can also view the various debt fund category returns aggregate on a daily basis from https://www.valueresearchonline.com/cat_index_returns.asp

As seen above the Debt funds (short term will be our preferred long term category) have provided around 8% returns over the long run.

Taxation Advantage

A significant advantage over F.D is derived from the way the debt funds are taxed.

Investment period less than 3 years

The taxation for Debt Funds and Fixed Deposits are almost the same for a holding period less than 3 years where the interest income is taxed as per your tax slab in both the cases. One small advantage that Debt funds have here is that you need to pay the taxes only at the time when you withdraw while in an F.D you must declare and pay taxes on interest income every year (read as additional headache).

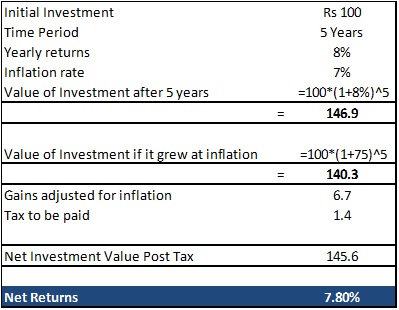

However for investment periods more than 3 years, Debt mutual funds have a significant taxation advantage over Fixed Deposits.The long term capital gains or gains from investments over a period of 3 years in a debt mutual fund (i.e your final value – initial investment value – if you invested Rs 100, 4 years back and now it is 135 then the capital gain is Rs 35) will be adjusted for inflation and then taxed at 20%.Let us take a little more time to understand this. Essentially the government is telling you that if the returns you make is lower than inflation, then the government won’t tax you and will tax you only if your returns are above inflation. So inherently debt mutual funds ensure that you are not taxed unfairly like a Fixed Deposit where you are taxed at your income tax slab irrespective of whether your returns are below or above inflation.Lets assume that the returns from a Debt mutual fund that you had invested was 8% for the last 5 years. Assume inflation was 7% for that period. Hence your tax component will be 20.6% of 1% (8% return – 7% inflation) i.e ~0.21%. Thus the net returns that we make post tax will be around 7.8%.

Summary:

- Debt Mutual funds provide a decent alternative for Fixed Deposits

- For investment periods of greater than 3 years, they offer better taxation advantage

- The returns from this category can be expected to be ~Inflation+1%

- Historically its been around 7-8%

Nice article.

LikeLike