In the earlier article (Gold Returns – Making sense of history), I had discussed on the historical returns from Gold for Indian investors. Now the most important question is what should investors expect from Gold going forward.

First and foremost, let me start with an honest submission. It is next to impossible to exactly predict the returns of gold or for that matter any asset class. But that being said we need to have an approximate idea on the broad direction and possible returns, which would allow us to reasonably plan our investments.

For Indians,

Price of Gold = International price of gold (denominated in USD) * USD INR Exchange rate

So, for us to have a sense of future gold returns (in Rs) we need to have a view on the International Gold Prices and USD INR.

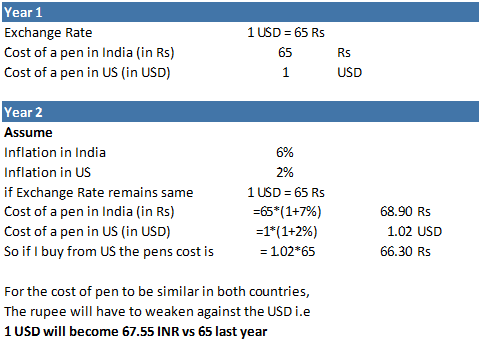

USD INR:

Generally over long-term, the currency weakening or strengthening vis-a-vis another currency is primarily based on the inflation differential between the two countries. The crude version of the logic is that, price of an item should be approximately equal across countries (i.e if a pen costs 65 in India and 1 USD is equal to 65 Rs then the pen in US must cost USD 1) . So if the price of the same item is increasing at different rate (read as inflation) then there has to be some adjustment mechanism to bring the prices to same level. This adjustment mechanism is what leads to currency weakening or strengthening.

See the below example for a better understanding

Therefore people will start importing from the US rather than buying from India. This will lead to increased demand for dollars and reduced demand for Rupees and therefore the rupee will weaken and adjust to become Rs 67.55 per dollar (compared to last year exchange rate of Rs 65 per dollar) to ensure the price of the pen is the same in both the countries. This is an extremely simplified version of what actually happens, but the broad idea is that “USD INR movement will be significantly influenced by the inflation differential between both the countries over the long run”.

So let us analyse what has historically been the inflation differential across both the countries:

Source: http://www.usinflationcalculator.com/inflation/historical-inflation-rates/

The average differential in inflation between US and India has been around 4%. Lets us make an assumption that this trend will continue and therefore whenever we buy gold for the long term, one of its return component, USD INR exchange rate can be expected to add around 4% annual returns. (USD INR annual depreciation was around 3% in the last 25 years)

Gold Returns:

As I had earlier mentioned, since gold has no underlying cash flows it is extremely difficult to come up with a prediction for gold. Generally gold tends to do well when there is a major crisis in the global economy. It’s perceived to be a safe asset and has been a store of value for several centuries. Hence whenever there is a significant crisis like event, investors move towards gold leading to higher Gold prices. Gold price also to a certain extent are inversely proportional to US interest rates i.e if US interest rates go up then gold price generally comes down and vice versa. This is because US Government bond (read it as lending to the US govt for a regular interest payment) interest rate is perceived to be the closest alternative for Gold in terms of safety. So when interest rate of US govt bond moves up , people will find US govt bond more attractive vis a vis Gold and hence might prefer to move towards US Government bonds.

Historically Gold prices in USD terms have averaged around 5-6% returns, but the returns have a wide variation between -4% to 19%.

One simple way to evaluate the possibility of decline in gold prices, is to find out how much it costs to produce an additional ounce of Gold at the current level. The cost according to various estimates is around 1000-1100 USD/ounce. This implies if the prices go below these levels then gold producers will be forced to cut gold production and eventually lower supplies will lead to demand supply mismatch which will force the prices up. Hence at the current price levels of around 1200 USD/ounce levels there is some comfort in terms of not much downside potential for Gold.

Assuming 5% from actual gold returns and 4% from currency returns, I would expect around 9-10% from Gold over the long term. If there are crisis events, the expectations will be surpassed and gold will have higher returns. And if the global economy recovers and international stock markets perform extremely well then you will find gold returns to be lower than our expected returns.

I guess SGB tilts the balance further in favour of gold investments. However I am late to the party. Would be good if you do similar analysis now. Is it worth to allocate 5% of gold to portfolio for someone who currently has 0% gold allocation ?

LikeLike

2025 – so far it has been good hedge to equity, worth 10% imo

LikeLike