In our last post here, we took inspiration from Steve Jobs and had decided to simplify our investment portfolio.

The key conclusions were:

- Limit the total number of equity funds in a portfolio to less than 4

- Only 3 categories for fund selection process

- Multi-cap Category (core) – 4 funds

- Mid Cap Category – 2 funds

- Small Cap Category – 2 funds

This week, we shall move on to the next step of “setting the right expectations”.

Setting the right expectations

Now before we move on to choosing funds (which in my opinion is really not the game changer it is made out to be), we need to answer the most important yet ignored question.

- How do we experience “good” performance? How do we know if we are in the right or wrong portfolio?

When it comes to evaluating investment performance, there are two types of people based on their expectations.

Let us call them

- Mr Absolute Abhijit – he needs absolute positive returns come what may

- Mr Relative Raju – he needs relative out-performance i.e either to beat his benchmark index or peer group

So whenever the above two open their portfolios and evaluate their returns their perception of good and bad performance will vary as shown below

Both Absolute Abhay and Relative Raju agree that beating the markets in a rising market is good while under performing during a falling markets is bad. However both disagree on out performance in falling markets and under performance in rising markets.

Now the sad truth is that all of us have shades of “Absolute Abhay” and “Relative Raju” within us. We also keep shifting between these two frames – focusing on absolute performance in negative markets and relative performance in positive markets.

Thus our evaluation of portfolios ends up looking like this..

We are happy only when we outperform in a positive market and remain unsatisfied at all other quadrants!

This personally to me, is by far the biggest problem in equity investing as given our unreasonable expectations and short time frames for evaluation, we end up being unhappy investing in equities for most of the time periods.

How do we solve this ?

Let us delve into each and every quadrant in detail..

Quadrant 1: Positive markets + Outperformance

This is a no brainer. This is exactly what we want and naively wish for every time we evaluate our portfolios.

So no problem as long as it is in this quadrant!

But just to be on the safer side, if the outperformance is dramatic then do investigate as to what is causing this (sector calls, concentration, stock picking, market cap allocation, asset allocation etc)

Quadrant 2: Negative markets + Outperformance

Let us be honest. While we might have outperformed on a relative basis, no one loves to see their hard earned money fall in value and this obviously is painful.

But the reality is that short term declines are inevitable in equity investing. The holy grail of moving out just before a decline and entering just before an up move just doesn’t exist.

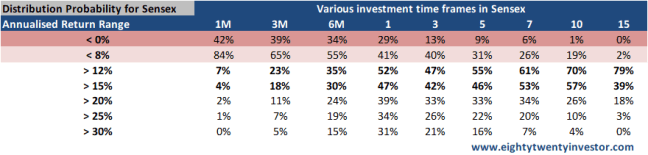

Historically, for someone who evaluated his equity portfolio every month, roughly 40% of the time, he would have found that his portfolio had fallen from his previous evaluation point value.

If he extends his evaluation period to 1 year, then still 30% of the times his portfolio would have been down from the previous evaluation point.

Thus if you are evaluating in shorter time frames, you will definitely see losses a lot more often and as a result your overall investment experience will mostly be unsatisfactory despite the fact that the odds are on your side for a good outcome in the long run..

Once you have decided to live with the fact that temporary declines are inevitable, you can decide on the extent of decline you can take and adjust your equity exposure accordingly (what is called asset allocation)

Takeaway: This entire quadrant of a falling market cannot be wished away and most importantly cannot be addressed by mutual fund selection.

It can only be addressed by

- Extending Time frame

- Asset allocation

- Tactical Asset allocation – if you have the expertise, then equity allocation can be adjusted (increased on decreased) based on market conditions (extremely difficult in practice)

If you have the time here is an interesting article on how even if god was your fund manager you wouldn’t be spared of this quadrant’s pain – Link

Quadrant 3: Negative markets + Underperformance

This I believe is a quadrant we must be worried about if our funds fall here. While we have no control over the markets, however if our funds are falling much more than the benchmark or peer group, then this may indicate that our chosen fund has taken higher risks.

Consider this an initial warning signal and we might have to deep dive into the portfolio and find out what exactly is happening.

Again the time frames shouldn’t be too short but at the same time unlike a longer time frame in our previous quarter, a 1 year time frame can be used to evaluate this quadrant.

“Over time, bad relative numbers will produce unsatisfactory absolute results.” – Warren Buffet

Quadrant 4: Positive markets + Underperformance

This is the quadrant where most of us tend to make mistakes and in a knee jerk response quickly exit and mover to newer funds.

Unfortunately, this happens as we don’t appreciate the fact that

Even good funds will inevitably have to undergo periods of underpeformance in the short run to perform in the long run

Let us listen to what Corey Hoffstein has to say about this phenomenen in this interesting article here

- In an ideal world, all investors would outperform their benchmarks. In reality, outperformance is a zero-sum game: for one investor to outperform, another must underperform.

- If achieving outperformance with a certain strategy is perceived as being “easy,” enough investors will pursue that strategy such that its edge is driven towards zero.

- Rather, for a strategy to outperform in the long run, it has to be hard enough to stick with in the short run that it causes investors to “fold,” passing the alpha to those with the fortitude to “hold.”

- In other words, for a strategy to outperform in the long run, it must underperform in the short run.

- We call this The Frustrating Law of Active Management.

Now don’t go by my words or Coreys. Let us go with facts.

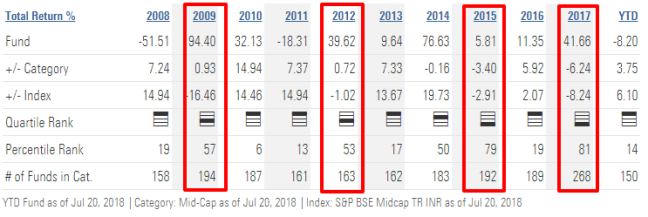

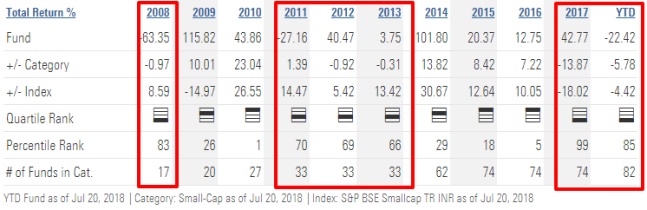

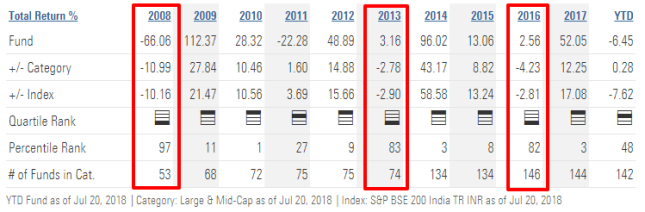

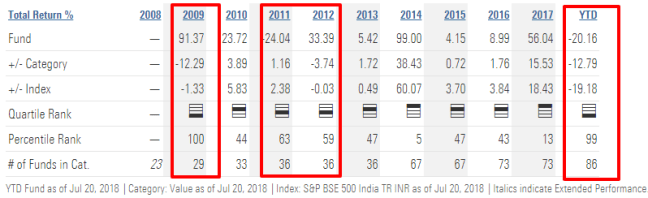

Let us pick the top 5 funds of the last 10 years (as on 20-Jul-2018)

Assuming you had the foresight to correctly pick them, would Quadrant 4 (under performance) still happen to these top performers at different points in time?

HDFC Mid Cap Opportunities

DSP Blackrock Small Cap Fund

Canara Robeco Emerging Equities Fund

IDFC Sterling Value Fund

Aditya Birla Sun Life Pure Value Fund

Source: Morningstar

As seen in all the above cases, it is inevitable that all these funds though gave good returns over the long run had to go through under performance in the short run.

(the above examples are just for illustrative purposes and I have conveniently ignored other issues such as size, change in fund manager, strategy etc which may have impacted performance)

Now this will be the case irrespective of whichever decent fund you consider in India or across the world. In fact, even the Warren Buffet has lagged the market one out of every three years.

So for us what this means is when we hit this quadrant – Underperformance needs to be put in context

- Underperformance of funds is not necessarily always bad

- Occasional underperformance in equity funds is inevitable

- Understanding when the fund manager’s style is expected to do well and when it may struggle is the key to evaluate the underperformance

- Evaluation of performance across a complete market cycle (covering a bull and a bear market) gives us a better picture

Performance evaluation framework in a nutshell

Thus now that we have a much better understanding of the 4 quadrants our new evaluation process looks like this

Summing it up

- While picking good funds is important, even more critical is our discipline to stick to the fund during periods of under performance in the short run

- This boils down to setting realistic expectations – which can improve our outcomes by reducing the possibility of us panicking and taking emotional decisions

- We usually have an absolute reference in falling markets and relative reference in positive markets – implying most of the times we will be unsatisfied

- Performance can be viewed in four quadrants – outperformance and underperformance in falling and rising markets

- Outperformance in a falling market is still painful; cannot be solved by fund selection – longer time frame + asset allocation is the solution

- Underperformance always needs to be put in context – it is not necessarily always bad as occasional underperformance is inevitable even for good funds

- Understanding when the fund manager’s style is expected to do well and when it may struggle is the key to evaluate a fund

- Evaluation of performance across a complete market cycle (covering a bull and a bear market) gives us a far better picture to evaluate the process

- This implies a good fund selection process must address two things

- Performance and risk measured across a complete market cycle

- Understanding of the fund’s investment style and process

- A fund’s communication to us on its style and process hence will form a key part of our evaluation

This is an evolving framework to evaluate performance and would love to hear your thoughts so that we can further improve on it.

In the next week, I will take you through my process of picking the funds.

Cheers and happy investing!

If you loved what you just read, share it with your friends and don’t forget to subscribe to the blog along with the 4500+ awesome people. Look out for some fresh, super interesting investment insights delivered straight to your inbox. Cheers!

If in case you have any feedback, need any help regarding your investments, want me to write about something or discuss regarding job opportunities, feel free to get in touch at rarun86@gmail.com

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments.

Hey Arun, Good post.. was wondering where are the MF screenshots from (apart from the first one)

Thanks,

On Sun, 22 Jul 2018 at 12:29 PM, The Eighty Twenty Investor wrote:

> Arun posted: “In our last post here, we took inspiration from Steve Jobs > and had decided to simplify our investment portfolio. The key conclusions > were: Limit the total number of equity funds in a portfolio to less than 4 > Only 3 categories for fund selection proces” >

LikeLike

Thanks Ankur 🙂

These screenshots are from Morningstar

LikeLike

Nice article Ankur!

LikeLike

Lovely blog. Revisited after few months and the recent 3 posts are awesome. Your content delivery style is refreshing, seeing things through a clear lense. Thank you very much.

If you don’t mind taking requests for new posts, then I have one and would love to read your views on :

– Asset allocation and rebalancing strategy in different market conditions (high or low from average index PE) for an investor, who may be just starting (portfolio building) vs someone in later stage.

LikeLike

Thank you so much Shree! Appreciate your suggestion and I will definitely write about asset allocation and rebalancing strategy in the coming weeks. Cheers 🙂

LikeLike