Just like in a video game, to get better in any field, there is usually a sequence of skills and problems to be mastered/solved progressively, one level at a time.

Managing your money is no exception.

But unlike a video game, where the levels are clearly defined and you don’t move up until you clear the current level, the “levels” in personal finance are unfortunately too vague.

And here begins the confusion..

- Is HDFC Top 200 better than Reliance Large cap?

- Is Nifty ETF better than a large cap fund?

- Should I directly pick stocks or stick to mutual funds?

- What is the impact of rupee depreciation on Indian equity markets?

- Will elections have an impact?

- Why do debt funds suddenly give negative returns?

- How do I exit before the top of the market?

- Is there a way to improve my SIP?

- Small caps vs Mid Caps vs Large Caps – which one?

- Direct vs Regular plans?

- Dividend vs Growth plans?

- and the story continues..

No doubt, there are too many questions. But which one do we solve first?

Not knowing where to start and which level a question belongs to, we confuse ourselves into thinking that we need to have answers for all these problems before we actually start investing.

So we end up trying to solve each and ever problem by endlessly debating, listening to CNBC anchors, watching interviews, reading newspaper articles, blogs, asking for advice from friends and family etc.

By the end of all this intellectual exploration, we fall into two categories with regards to our money:

1. Bogged by the complexity, we completely ignore taking any sort of a decision and feel guilty

2. We continue to obsess over finding a perfect solution by arguing over minor details and don’t take action.

Sadly, both the options yield the same results – None.

So what is the solution?

JUST START!

Yup, you heard it right. That is exactly the solution.

Now, this means we need to take a step back from all the confusing overload of jargon and information thrown at us, and just like a video game need to solve it one level at time.

As Eighty Twenty Investors, we shall first solve for the simple yet critical problems which will help us build a 80% good enough money solution. Over time we shall gradually progress and improve over and above the 80%.

No while this is an evolving thought process, if I were to personally start it over all again, this is the hierarchy I would go about to manage my money.

Level 1: Spend less than you earn = Save the remaining

When I first started my fitness journey, I deep dived into a quest of finding the best exercise routine, best protein powder, best diet, best shoe, best time to workout blah blah.

6 months later still trying to find out the best solution, I realized the problem was much more basic – I had to first solve for inculcating the habit of regularly going to the gym!

Similarly, when it comes to investing, the starting point is fairly basic and simple – if you can’t save enough, all other things don’t really matter.

Yet ironically, most of us focus on all the complex nuances of investing conveniently forgetting the starting point.

Now if you are wondering why in the world am I making such a big issue out of this. Check these two earlier articles to realize who we are up against and why incrementally saving money is going to become a huge problem..

- The secret war on your savings has already begun

- This behavioral scientist has the surprising answer to our spending habits

So the first ground level problem to solve – How to save enough regularly?

Level 2: Emergency Fund

Once you are done solving for the habit of saving regularly, we come to the level 2 problem – building an emergency fund.

As we all know, emergencies are a fact of life. A sudden job loss, medical emergency, unexpected home repairs, car accident, dropping your mobile phone and the list goes on.

Saving up for an emergency fund is a simple way of acknowledging “Shit happens! Let me be prepared”

A good starting point would be to build around 6 months of your monthly expenses in a safe, liquid and stable investment option such as

- Separate Savings Account

- Bank Fixed Deposit

- Liquid Fund (preferred option)

Level 3: Insure your life and family’s health

The next step is to go ahead and get

1.Health Insurance for you and your family

2.Life Insurance: Simple plain vanilla Term Cover

This is an extremely confusing exercise given the myriad of choices and features and maybe sometimes in the coming months I will do a separate post on how to choose health and term insurance.

Remember: Never ever mix your investments and insurance

The best part is all the decisions till now – emergency fund, health insurance and life insurance are usually one time decisions. Once you decide on the product, then all you have to do is to regularly pay your premiums in case of insurance and in case of an emergency fund, keep investing a small amount monthly till you reach the required savings to cover 6 month expenses.

Level 4: Simple Goal based Financial plan

The 4th level, is to create a simple goal based financial plan.

Find below the required steps:

- List your financial goals (kid’s education, early retirement, buying a house, starting a business etc)

- Estimate the time frame for every goal

- Approximate the current costs

- Adjusting for inflation calculate the future costs

- Calculate the amount to be saved (either one time or monthly or a combination of both)

The below articles can be a good starting point on how to get this done..

- A simple trick to estimate your future costs in 2 minutes (Link)

- Create your own financial plan while you are waiting at the traffic signal (Link)

- See how easily you can create your own financial plan in 15 minutes (Link)

Level 5: Get short term goals (<5 years) sorted

Since the time frame is very low, it is not advisable to use long term asset classes such as equities given the significant ups and downs in the short run. Hence the idea would be to stick to a safe debt or arbitrage oriented portfolio.

- Build using a short term debt mutual fund or arbitrage fund – you can invest the entire amount if you have or start an SIP

- You can refer the link below for details on how to pick funds

- Now with near term money requirements out of our way, we are left with our long term investments.

Level 6: Long Term goals

Once you have solved for all the above levels, this is the final level which is simple yet not easy to master. This level has to be broken down into sub levels and solved one piece at a time

Let us check out the sub levels..

6.1.Investor Behavior

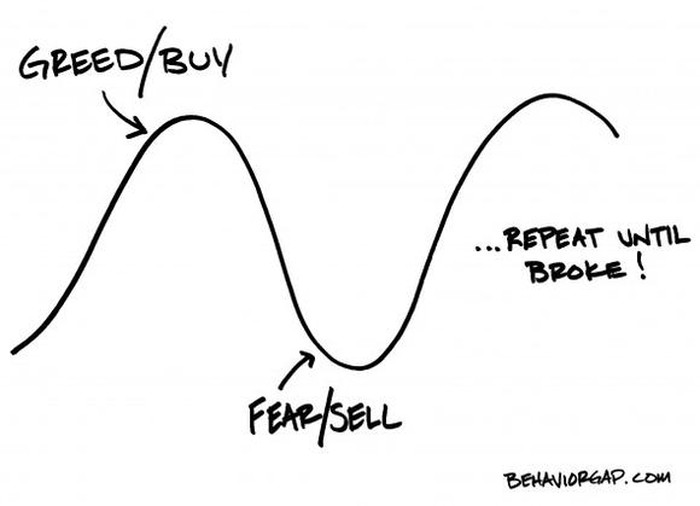

Time and again it has been observed that investment returns and investor returns are almost always different.

You earn the investment return if you invest your money and then don’t touch it. No buying, no selling, just holding.

But in reality, people rarely invest this way. They sell in fear when markets fall and buy in greed when markets move up. Most of us chase performance and invest by looking in the rear view mirror.

This gap in investor returns vs actual investment returns is called as The Behavior Gap.

The key is for the investor not to get carried away in greed during a bull market and in fear when the markets are falling.

You can read this post to get a sense of a real life example of how greed played its part in luring investors.

- Seat Belts, Condoms and the Indian Equity Investor (Link)

Also you can refer to these posts to understand how to handle a falling market.

- Three ways to make sure this stock market correction is not wasted (Link)

- If you panic during a market fall it’s not your fault. Blame it on.. (Link)

- A guilty father who shot his own kid, ancient Greek philosophers, US Navy Seals and the art of handling a market fall (Link)

- “What if things go wrong” Investment Plan – (Link)

- 6 reasons why we panic during a market correction (Link)

Finally it all boils down to this..

The most important part of an investing strategy is your ability to stick with it. A subpar investing strategy that you can stick with and apply consistently will nearly always outperform a brilliant strategy you give up on. Your final investing results probably won’t be determined by whether you currently use a strategy that historically delivers an extra 50 basis points of return. What will matter is whether you had the disposition to stick with investing, however you chose to do it, through thick and thin.

Morgan Housel

6.2.Asset Allocation

Different asset classes come with different return expectations and risk (i.e how wild they fluctuate in the short run)

A quick rule of thumb for setting return expectations would be

Equity: Inflation + 5-7%

Real Estate: Inflation + 3%

Gold: Inflation + 2%

Debt Mutual Funds or FD: Inflation+1%

The choice and the mix of assets in your portfolio will have the largest influence on your long term returns.

Now typically equities are the best choice for long term allocation but the cost that you pay for higher returns is the sharp falls the asset class goes through in regular intervals. In fact a 10% fall once a year, 20%-30% fall once in couple of years and 40-50% fall atleast once a decade is unavoidable.

So depending on the extent to which you are comfortable with seeing your long term portfolio decline, decide on your equity allocation.

A rough rule of thumb would be:

Equity Allocation = The maximum near term % decline you are ok to see in your portfolio * 2

So if you are ok with upto 30% decline then go for around 60% in equities. The remaining 40% can be in debt mutual funds.

6.3. Risk Management

This is where you try to put “investment behavior” part into practice.

The philosophical question goes like this:

Should you try changing the investor or investment?

While in the “Investor Behavior” part we try and address the investor, in this section we try and evolve the investor portfolio to adapt to the behavior of the investor.

This is based on the reality that – the ability to take risk (or what is called risk tolerance) of the investor is not a constant. The recent market performance has a huge influence on the risk tolerance where usually investors become high risk takers in a bull market and low risk takers in a bear market.

Thus we need to introduce risk management. This in normal human language means – we need to actively adjust the equity allocation based on our evaluations of risks in the market (a combination of valuation, earnings growth, sentiment etc)

If you find this going over your head, no worries, just stick to simple process of re-balancing back to original asset allocation – either annually or whenever equity allocation deviates by more than 10% from the decided allocation

6.4.Geographic Allocation

Once you have decided on the asset allocation, the next decision is to decide on which countries businesses (equity) do you want to bet on. Logically, most of us will start of with our home country (India in my case).

But sometimes, there is always the rare possibility of what if it turns out to be like Japan!

So while many people argue on why you shouldn’t bet on equities citing Japan’s case, but I think the actual takeaway is to diversify your equity exposure across global businesses.

6.5.Category Choice

This is where you solve the question of mutual funds vs direct stocks.

My suggestion would be to start predominantly with mutual funds and have a small portion of your portfolio to direct stocks. If you enjoy the process of stock investing, can spend time to research, then based on your evolution and performance over a 5 year period you can gradually move towards a stock based portfolio.

For the majority 95% of us, mutual funds will do the job.

- Within mutual funds again there comes the question of: Passive vs Active

- Within active funds comes the question of: Diversified vs Sector Funds.

- Within diversified funds comes the question of: Large Cap vs Mid Cap vs Mutlicap

You can read my thoughts on the above topics via this article

6.6.Security Selection

In this stage, you figure out how to choose equity and debt funds from various categories.

You can refer to these posts to get a fair idea on how to go about with this

- Selecting an equity mutual fund is a pain in the neck! Find out why? (Link)

- What if Steve Jobs was an Indian Equity Investor (Link)

- How do we experience good performance (Link)

- How to select equity mutual funds the eighty twenty investor way – Part 1 (Link)

- How to select equity mutual funds the eighty twenty investor way – Part 2 (Link)

- How to select equity mutual funds the eighty twenty investor way – Part 3 (Link)

- Here’s how I finally set up my investment portfolio for the next 10 years (Link)

You can also refer to these posts to pick debt funds

- A primer for investing in debt mutual funds (Link)

- 8 factor framework for analyzing any debt mutual fund (Link)

- Investing Chitra Katha – Understanding the impact of modified duration on debt fund returns (Link)

- The ultimate guide to liquid funds (Link )

- Here’s a quick way to select Ultra Short Term Funds (Link )

- Making sense of Short Term Debt Mutual Funds (Link)

- Credit funds – Don’t count your returns before they hatch (Link)

- Here’s why I don’t invest in credit funds (Link)

- Figuring out a simple do-it-yourself framework for short term investing (Link)

Stock selection is an ocean in itself. I would suggest you start with websites such as https://www.drvijaymalik.com/ , https://www.safalniveshak.com/ etc

6.7.Cost

In Investing, You Get What You Don’t Pay For

John.C.Bogle

Globally passive investing (via ETFs) have gained significant popularity in recent times. Their pitch is simple – Buy an entire index covering all major stocks and get it at the lowest cost.

In India, while we are still some time away from active funds losing their edge, large caps is a segment where there are initial signs of passive funds giving a tough competition.

Direct vs Regular?

SEBI in 2013, introduced a new option in mutual funds – “Direct” option

to provide an option to invest in mutual fund schemes directly, without the involvement of any agent, broker or distributor as the case in “Regular” mutual fund plans.

Regular and Direct plans are just the two options of the same mutual fund scheme, run by the same fund managers who invest in the same stocks and bonds.

The only difference between the two is that in case of a regular plan your AMC or mutual fund house does pay a commission to your broker as distribution expenses or transaction fee out of your investment, whereas in case of a direct plan, no such commission is paid. Instead, in case of direct plans the commission is added to your investment balance, thereby reducing the expense ratio of your mutual fund scheme and increasing your return over the long-term.

The advantage of direct funds is that their expense ratios (the charge of the mutual funds for managing your money) is usually lower by 0.5% to 1% compared to regular plans.

So always chose a direct plan (and even if being advised by an advisor pay his fees directly which keeps both your incentives aligned)

6.8.Tax

Once you are done with all the above steps, then you can also evaluate the taxation for various investment options and choose a tax efficient vehicle to access the underlying asset class.

Summing it up..

Now the next time you are caught up in a debate of say which fund to choose, passive vs active etc, relax, take a deep breath and ask yourself if you have solved for the levels before that.

If not, get the basic ones sorted first.

Most importantly, don’t get into the never ending loop of debating the minor things in search of the perfect solution.

Solve these levels one step at a time and in a few weeks you will have your 80% solution ready. Trust me, you will be much better off than the majority who still are in search of that elusive perfect investment solution.

And anytime you catch your friends getting caught in this trap, send them this article.

As always, Happy Investing folks…

If you loved this post, do share it with your friends and don’t forget to subscribe to the blog via Email (1 weekly newsletter) or Twitter along with the 5000+ awesome people. Look out for some fresh, super interesting investment insights delivered straight to your inbox.

If in case you have any feedback or need any help regarding your investments or want me to write about something, feel free to get in touch at rarun86@gmail.com

You can also check out my other articles here

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments.

kmenvy@yahoo.com

Sent from Yahoo Mail on Android

LikeLike

Fantastic article, as always, Arun !!

LikeLiked by 1 person

Thanks a ton and glad you like it 🙂

LikeLike

Nice one da. Good for new investors as well as a good course correction chart for existing ones. Too many links though, a bit distracting.

LikeLike

Thanks Pravin. I will try and reduce the links.

LikeLike

In my opinion, equity returns instead of “inflation + 5-7%” as given by the author, it should be “nominal GDP growth (which includes real GDP growth + inflation) + 3-5%”. Because just getting or even getting less than what is our nominal GDP growth is not worth investing in equity and taking risk. Debt return is OK at “inflation + 1%”, could be “inflation + 2%”. This is as per RBI assumption and report also that the “real” interest rate should be around 2-3%.

LikeLike

Fantastic Post Arun, Congrats! I recently read that best way to retain learning on specific topic is to Share the knowledge with others. I hope putting this framework in place is helping you build more solid understanding.

LikeLike

Thanks Puneet. What you told is 100% true. One of the best ways to truly understand a topic is to write and explain it to others.

LikeLike