You have been comfortably investing a part of your salary regularly through an SIP into few good equity funds. This works perfectly fine as the monthly investments average out the equity market ups and downs. Typically, going by history over the long run you would make decent returns mirroring the underlying growth of Indian businesses.

But we have another common occurrence, which unfortunately has not received much attention.

What if you suddenly receive a large amount of money?

Think bonus, property sale, inheritance, ESOP etc

A large amount is basically whatever is large enough for you. There are no hard and fast rules. I personally consider any amount more than 24 times i.e 2 years of my regular monthly savings as a large amount.

Now you have a problem.

How do you invest this in equities?

- Do you go all in and invest everything into equities in one shot – but what if the markets crash immediately after you invest – think Jan-2008.

- Keep it in cash (read as liquid funds) and invest the money when equity markets fall – but what if markets go up like crazy – think 2009, 2014, 2017

- Equally splitting your investments over a time frame (of around 6 months to 3 years) – this is a midway path where you try to average out your buying price. Again you will miss out if there is a sharp up move or the fall happens exactly after you are done staggering your investments. Imagine equally splitting your investment amount into 12 portions and investing for 1 year till Jan 2008.

Now while all the above are extreme examples, the take away for us is that irrespective of which strategy you use to invest your money, there will always be instances where you would have regretted not using the alternate strategy.

The only way out is to predict how the markets will move in the short run.

Unfortunately there has been no one who has been able to do this on a consistent basis.

“The idea that a bell rings to signal when investors should get into or out of the market is simply not credible. After nearly 50 years in this business, I do not know of anybody who has done it successfully and consistently. I don’t even know anybody who knows anybody who has done it successfully and consistently.”

― John C. Bogle

Minimizing regret..

This means, throughout your life as you keep getting large amounts at different points in time, regret will also be a regular companion. It may either be regret of missing the upside or regret of participating in a downside.

If you think there is some secret parameter which will let you know what the markets are going to do in the short run and help you identify the perfect strategy, then the article ends here for you. I am not aware of any.

But if you are someone who agrees with me that the markets are too random and can’t be predicted in the short run, I have a solution for you.

It all starts with the humble acceptance that we cannot completely eliminate REGRET.

Rather the only thing under our control, will be on how to minimize regret and live with it.

Let me explain with an example.

Case study

Assume you have got a large inflow of Rs 1cr. Your existing portfolio is around Rs 50 lakhs (entirely in equities).

Here is how you can go about adding this Rs 1 cr to your existing Rs 50 lakh portfolio.

First you need to answer the simple question:

What is the maximum short term loss you are willing to tolerate in your portfolio?

This will be the decline in portfolio value beyond which you might find it extremely difficult to stay with the existing portfolio. In other words, this is your freak-out point!

For the entire Rs 1.5 cr portfolio (Rs 1 cr new money + Rs 50 lakhs in existing portfolio), you understand that some bit of risk (read as short term declines) needs to be endured for better long term returns.

While it is definitely painful, you are willing to tolerate upto Rs 25 lakhs loss. Anything beyond that might be really hard on you.

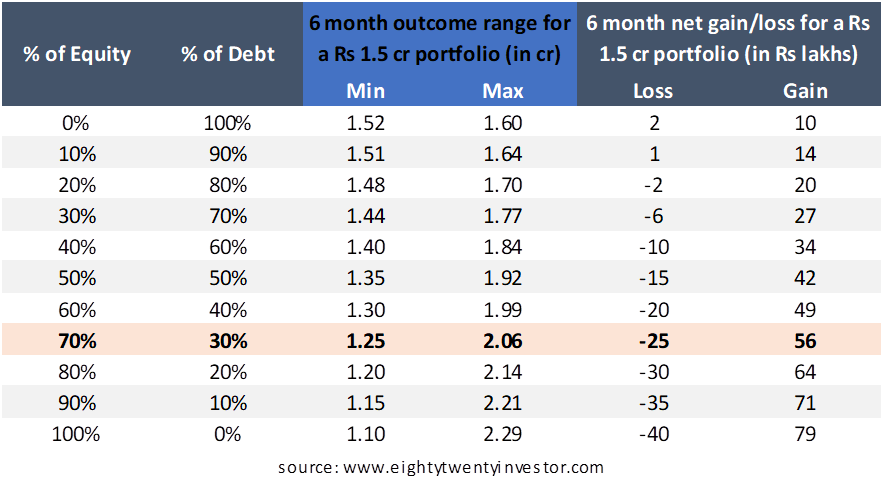

To get an idea on how past declines have been, let us check the historical range of outcomes for different asset allocation between equity and debt over a 6 month period.

The workings have been calculated for the last 18 years with a large cap fund (Franklin India Bluechip Fund) representing equity allocation and a short term fund (IDFC Bond Fund – Short Term Plan) representing debt allocation.

The table can be interpreted as:

Over the next 6 months, there is a 95% probability that the returns from a 70% Equity + 30% Debt portfolio will be between -17% to 30%. This range describes the “comfortable zone” for the particular asset allocation. In other words, this is the normal behavior to be expected from the particular asset allocation.

It is hard to quantify 5% of the market, which can involve black swan events like housing bubble, dot com bust, war, earthquake etc. However you can control for 95% of the risk by choosing the appropriate asset allocation.

Why six months?

There has been elaborate research done by the US firm Riskalyze which concludes that 1 year is too long a period for investors to stay calm during a market fall while 3 months is too short. They have found that 6 months is the sweet spot where most of us want to take a decision on portfolio performance. In fact they have built an entire business around this concept. Do check them out.

Let me apply these ranges to your Rs 1.5 cr portfolio:

Since you had decided on a maximum tolerance of upto 25 lakhs loss, a 70% Equity: 30% Debt portfolio would be ideal for your risk tolerance.

This implies that going by history, it is normal to expect the portfolio to be anywhere between Rs 1.25 cr to Rs 2.06 cr in the next six months. In other words the outcome can range from Rs 25 lakhs loss to Rs 56 lakhs gain over the next 6 months.

While we have no clue where it would be in this range, but if it is in this range then everything is normal and it is behaving exactly as per expectation.

The Rs 1.5 cr will get split into 30% i.e Rs 45 lakhs in debt and the remaining 70% i.e Rs 1.05 cr in Equity.

Since there is no timing risk in low duration debt funds, immediately invest Rs 45 lakhs in your chosen debt funds. I prefer Ultra Short Term or Short Term Funds.

Rs 50 lakhs is already in equities. So we have to deploy the remaining Rs 55 lakhs in equity.

While we have addressed the 95% of expected normal outcomes via the asset allocation, we are yet to address the 5% probability of abnormal outcomes. These events though rare, will definitely happen at some point in time. Historically these events have occurred once every 8-10 years.

So how do we address these 5% probability events?

Enter the Asset Allocation Traffic Signals

While the short run is unpredictable, we can roughly approximate the long run returns. You can refer my earlier post here to evaluate where equity markets are in the current cycle. Based on the framework to estimate returns, you can classify the markets into three zones Green (very attractive), Yellow (average) and Red (very risky).

Green: Expected 5Y Returns above >15%

Yellow: Expected 5Y Returns between 8 to 15%

Red: Expected 5Y Returns less than <8%

If it is in the Green zone, then the odds are in our favor and it is better to invest the entire Rs 55 lakhs at one go. Choose 2-4 equity funds and invest immediately.

If it is in the Red zone, then the markets are extremely risky and the odds are not in our favor. We will invest in 2-4 Dynamic Asset Allocation Funds which auto adjust equity allocation based on various valuation parameters. We will shift this portion back to pure equities when the markets go back to Green zone.

If it is in the Yellow zone, then the markets are neither too risky nor very attractive. We will invest Rs 27.5 lakhs in 1 or 2 Dynamic Asset Allocation Funds and another 27.5 lakhs in 1 or 2 Equity Funds. We will shift the Rs 27.5 lakhs in Dynamic Asset Allocation portion back to pure equities when the markets go back to Green zone.

These valuation and earnings based asset allocation calls, to a certain extent help us manage the 5% abnormal market conditions.

Now for those of you who think this is a lot of work and complicated, worry not. I have a workaround for you.

What if we instead, gave the job of taking Asset allocation calls to an experienced veteran with 30 years of investing experience. Someone who has been running asset allocation strategies for the past 10 years and has a solid track record. Someone who has an experienced team tracking several parameters day in and day out and has established a good enough model which has worked so far.

What if I told you, all this comes free for you – if you can spend 5 minutes every month!

Wow!

Let me reveal the secret for you – ICICI Prudential Balanced Advantage Fund

This is an auto adjusting asset allocation based fund which moves its equity allocation between 30% to 80% based on a valuation model.

The fund is managed by Naren (read about him here). After a lot of trial and errors in the model between 2008-2010, the model in its true avatar was live and running from 2011.

The fund has had a solid track record since then and had basically pioneered the entire category. After seeing its success almost every AMC has launched its own version in recent times.

You can see that the equity allocation calls have worked well for the last 8 years. The best part is that, the asset allocation is disclosed every month in the factsheet (which gets published around 12th of every month).

If you don’t want to go through the hassles of building your own allocation model, then you can go with Naren’s model. Here is how..

Red: If equity allocation is between 30% to 40%

Yellow: if equity allocation is between 40% to 65%

Green: If equity allocation is between 65% to 80%

Thus by spending 5 minutes every month to check the equity allocation of ICICI Prudential Balanced Advantage Fund, you can make use of Naren’s asset allocation model.

Now doing all this doesn’t mean we will be able to perfectly time the market. This is basically a method to the madness, where using history and valuations as a guide we are trying to tilt the odds in our favor. The idea is to minimize regret and get reasonable participation in the upside while reducing the participation during downside.

Why do we need a framework like this?

The biggest risk whenever we get large amounts of money is INACTION.

We somehow get scared by the possibility of going wrong and keep postponing the investment decision.

So here is the deal.

Whenever you get a large amount of money, give yourself 2 weeks to decide on a strategy to invest. If you are not able to take a decision, then go ahead with the plan that I have suggested. If you think you have a better strategy, great, just execute it.

The key is to not get into the “freeze” mode!

Make this Large Amount Investing strategy a part of your annual discussion with your advisor. If you are on your own, then make sure you have the plan written down every year.

Summing it up:

When you get a large sum of money to invest, use the following steps

- Decide on the maximum extent of loss you are comfortable to take on your portfolio in the next 6 months

- Based on this, choose asset allocation split between equity and debt based on the 95% probability 6 month return range (refer the table)

- Immediately deploy the debt portion in short duration funds (Ultra Short Term or Short Term)

- Equity Portion will be deployed based on asset allocation signals:

- Green – Invest in 2-4 equity funds immediately

- Yellow – Invest in 2 Dynamic Asset Allocation Funds and 2 pure equity funds – portion in 2 Dynamic Asset Allocation funds will be moved to pure equity funds when market goes back to Green zone

- Red – 2-4 Dynamic Asset Allocation Funds – will be moved to pure equity funds when market goes back to Green zone

If you feel the strategy can be improved, or there are views that you don’t agree with or perspectives that can be added do let me know either via the comments or by mailing to me at rarun86@gmail.com

Happy investing as always!

If you loved this post, do share it with your friends and don’t forget to subscribe to the blog via Email (1 article per week) or Twitter along with the 5000+ awesome people. Look out for some fresh, super interesting investment insights delivered straight to your inbox.

You can also check out my other articles here

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments.

Hi Arun,

Thanks for a Very practical and Great article, as always :-).

I have checked Fund factsheets of ICICI Prudential Balanced Advantage Fund of various mnonths. Under the Portfolio Details section, their equity shares is always about 65-68 % to NAV, but they have written Net Equity Level at the bottom which varies (i think this one you have depicted in your article above).

Can you clarify, what is this equity shares percentage which is about 65-68 % to NAV means?

LikeLike

Thanks Gaurav. Actually to be taxed as equity fund a fund needs to have more than 65% in equities. But thankfully arbitrage which behaves like debt is also considered as equity. So dynamic asset allocation funds based on their model build the equity exposure first (called net equity exposure). If it is less than 65% they fill the remaining with arbitrage so that they can get equity taxation. The net equity exposure plus arbitrage portion represent the equity shares percentage. For us, net equity exposure is what matters.

LikeLiked by 1 person

Thanks

LikeLike

Hi,

Thanks for your good article on investment strategy.

How one can find that the said fund / any fund come under equity taxation.

Thanks

LikeLike

Excellent article. Exactly what I needed. However, am I missing the link for the current allocation of icici prudential balanced advantage fund.

LikeLike

Hi Arun,

Just one doubt. In the example you have mentioned that for a maximum loss of Rs 25 lacs, 70:30 is an ideal ratio. So supposing if i were to apply the same rule to an investment of say 10 lacs, which ratio will apply? Because, if I consider a maximum risk tolerance as a percentage of total investment, in the example you gave, it is approx 17%. Applying this to my total investment of 10 lacs, my risk tolerance works out to Rs 1.7 lacs (which I am willing to take on). If i were to go by the % of investment basis, I could go upto an equity debt ratio of 70:30 as per your example. However, if i go by the absolute loss nos, the ideal ratio is coming to 10:90 as per your table.

Can you please explain which is the correct way to interpret it.

Thanks.

Rajesh

LikeLike

Hi Arun,

Just one doubt. In the example you have mentioned that for a maximum loss of Rs 25 lacs, 70:30 is an ideal ratio. So supposing if i were to apply the same rule to an investment of say 10 lacs, which ratio will apply? Because, if I consider a maximum risk tolerance as a percentage of total investment, in the example you gave, it is approx 17%. Applying this to my total investment of 10 lacs, my risk tolerance works out to Rs 1.7 lacs (which I am willing to take on). If i were to go by the % of investment basis, I could go upto an equity debt ratio of 70:30 as per your example. However, if i go by the absolute loss nos, the ideal ratio is coming to 10:90 as per your table.

Can you please explain which is the correct way to interpret it.

Thanks

LikeLike

Go by the percentage of total investment. The nos in the example are for a 1.5 cr portfolio. So won’t be applicable for your portfolio.

LikeLike

Nice One, Arun.

LikeLike

Thanks!

LikeLike

hi Arun

Nice article. Just one question, Why not stick to equity funds when investing via SIPS and choose only balanced dynamic funds when investing via lumpsum. Then we don’t have to really worry about splitting lumpsum portion into debt and equity portions. The returns of the portfolio can be slightly lesser but it will be lesser volatile for sure.

LikeLike

I am interested in getting new posts

LikeLike

Hello. Since I read this article, I have never seen the Net Equity Ratio exceed ~40%. So, is that the case? Is the market, in the past few years have never been good for pure equity?

LikeLike