This is the 3rd post in the debt mutual fund investing series. If you have the time, it would be great if you could go through the earlier posts in this series –

Part 1 – A primer for investing in debt mutual funds (Link 1)

Part 2 – 8 factor framework for analyzing any debt mutual fund (Link 2)

There are primarily 8 categories of debt funds:

- Liquid Funds

- Ultra Short Term funds

- Short Term funds

- Income Funds

- Dynamic Funds

- Accrual or Credit Funds

- FMP

- MIP

Phew..8 categories ..this seems to be complicated..

So instead of breaking our head over the complexities, lets try and break it down to the basics and nail down the few categories which will matter the most to us. In fact for my personal investments, I like to keep it extremely simple and stick to only the first three categories i.e Liquid, Ultra Short Term and Short Term Funds !! So hang on for a while and we will get this thing sorted.

If we strip down all the jargon, the underlying difference across the categories simply boils down to what type and extent of risk are the funds taking to improve returns via

- Interest rate risk (measured via modified duration)

- Credit risk (measured via the % of portfolio with lower than AA securities))

With this in mind, let us explore various categories..

For all temporary parking of money which we need within 1 year, we can consider

1. Liquid funds – upto 3 months

2. Ultra Short Term funds – 3 to 12 months

Liquid Funds (Think of it as an alternate to Savings Bank Account)

Liquid Funds invest with minimal risk in short term debt instruments with a maximum maturity of 91 days. This is captured in the “Average Maturity” and in practice, for most funds it averages to less than 2 months. They have the lowest risk and are ideal for parking temporary money.

(Ignore if you find it a little technical: The instruments where liquid funds invest generally include CBLO, certificate of deposits (i.e short term lending to companies), commercial papers (short term lending to companies) and treasury bills (short term lending to government) and term deposits (bank FD) )

While investing in Liquid funds generally returns are not the top priority. I mean have you ever worried about your savings bank account paying you only 4%. The priority is safety, liquidity (i.e can be taken out anytime) and returns – in that order.

So as expected, these funds do not take credit risk as they are predominantly invested in AAA equivalent bonds and also do not take interest rate risk (they have very low modified duration) to improve returns. This basically implies that liquid fund NAV returns will generally be very stable as the underlying returns are predominantly driven by interest income (from the underlying debt securities) which accrue everyday.

Approximate Return Expectation from a liquid fund = Net YTM = YTM-Expense ratio

Also remember that while investing in liquid funds, if interest rates increase our returns also increase and if interest rates decline then our returns will also decline.

Liquid funds for people like us can be used in several ways. For eg

- Temporary parking: For eg, every month when I get my salary, I immediately park my intended savings in a liquid fund. Then as and when I find time, I transfer it to equity funds or any other option which I like at that juncture.

- For systematic transfer plans into equity funds: Sometimes you may have a large amount of money which you don’t want to put in equities at one shot. So you may put it in a liquid fund and do a systematic transfer plan into equity funds or manually move it as and when you want.

So how do we select our liquid fund??

The first advantage when it comes to selecting a liquid fund is that the chances of a big mistake is not there. Since most of them prioritize liquidity, do not take credit risk (except for a select few funds which may take minimal credit risk to show better performance) and have very low modified duration, the returns across different liquid funds is generally in a narrow range and most of the return differential can be explained in terms of expense ratio and portfolio composition.

In terms of the portfolio composition, the returns are higher in the order of Commercial paper (CP) > Certificate of deposit (CD) > Treasury bill (T Bills). T Bills and Certificate of deposits are more liquid compared to Commercial Papers. A liquid fund with higher exposure in commercial papers is considered to be more volatile as these securities are generally not as liquid as CDs or T-Bill. So the fund may be producing higher returns but will also have a slightly higher risk. Hence if you are extremely conservative choose a fund which has a lower % of Commercial Papers).

Simple steps to choose our required liquid fund

- Stick to large AMCs

- Check credit quality

- Go for a fund size above 1000 cr

- Lower the expense ratio the better

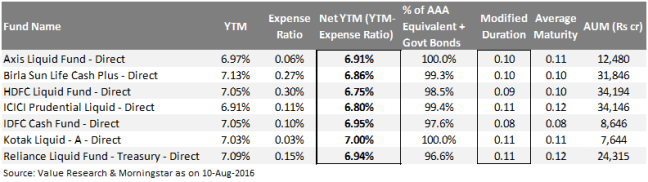

When it comes to Debt funds, I generally prefer to stick to major AMCs such as ICICI, HDFC, Reliance, Kotak, IDFC, Axis etc. Is there something wrong with other AMCs. Of course not but given the narrow range of return outcomes I am more comfortable investing via the larger names. Some funds under the large AMCs are ICICI Prudential Liquid Plan, Reliance Liquid Fund – Treasury Plan, IDFC Cash Fund, HDFC Liquid Fund, Kotak Liquid fund, Axis Liquid fund. You can consider any of the above. I generally use IDFC Cash Fund. If you want more options you can check here – Link

Snapshot

Most importantly, let’s not get too lost in the tendency to over analyse (which yours faithfully gets caught into often), as anyway the return differential is not going to be too high and the primary reason for using liquid funds is for safety, liquidity, convenience and of course some reasonable returns.

In fact when I was researching for this article , I found that there is a new app called Finozen which has just started with the premise of letting you switch back and forth between a savings bank account and liquid fund. I never thought someone could build a business model around liquid funds. But nevertheless simplicity always has its charm. They have a nice 30 second video on liquid funds. Do check if you have the time – Link (by the way I have no clue on who they are..nor am I recommending them..Found the idea to be interesting and hence the mention 🙂

At the current juncture the Net YTM (i.e YTM- Expense ratio) for most of the liquid funds work to be around 7%. So the daily returns going forward assuming interest rates remain the same will be roughly 7%/365 = 0.019%. This implies that if I invest Rs 1 lakh, I can expect approximately Rs 19 to get added everyday.

Now while liquid funds are for all practical purposes extremely safe and provide better returns than an SB account, we also need to be aware of some possible risks.

- Sharp increase in interest rates:

On 16-Jul-2013, India was going through a currency crisis due to the announcement of Fed Taper. As a result there was a sharp increase in interest rates of up to 2% leading to negative returns in liquid funds for a day. Kindly go through the articles to understand what really happened – Link 1 Link2

Now what if we had a similar scenario like that repeat and interest rates went up by 2%. Taking the example of IDFC Cash Fund, it currently has a Net YTM = YTM-Expense ratio of 6.95%. Therefore daily returns from interest accrued is 6.95%/365 = 0.019% or Rs 19 added per day for every 1 lakh invested. It has modified duration of 0.08 years – which means that the negative NAV impact in our fund for a 2% increase in interest rate would be a -2%*0.08 =-0.16%. Now if you adjust for the interest income everyday (i.e 0.019%) then the negative impact will be -0.14%. Or in other words, Rs 1 lakh investment would be roughly down by Rs 140 to Rs 99,860. This is equivalent to 0.16%/0.019% = 9 days of usual returns in the fund. Now remember that our Net YTM has now increased from 6.95% to 8.95%. Therefore daily returns from interest accrued post the interest rate increase is 8.95%/365 = 0.025% or Rs 25 added per day for every 1 lakh invested. So to compensate for the loss of -0.14%, we will need to wait for 0.14%/0.025% (or Rs 140/Rs25) i.e approximately 6 days. While these are rare events, whenever they occur there will be a lot of panic which will be disproportionately exaggerated by the business news channels. So if in case something like that happens, the most important thing is not to panic as we clearly know how liquid funds derive their returns and to remember that its only a matter of waiting for 7-10 days before we tide over our temporary decline. - Crisis scenarios leading to significant redemption from the funds and the fund not able to sell underlying securities due to low liquidity (read as no buyers):

When this scenario happened last time during 2008, since redemptions were high from liquid funds and buyers were not there, few funds were forced to liquidate their underlying debt securities at lower prices thereby taking an NAV impact. The larger AMC’s were able to tide over this as they arranged for temporary loans/support from their sponsors after which RBI came to the rescue. So this is the reason why I generally stick to large AMC’s with strong debt fund management teams.

Parting Thoughts:

- Think of Liquid funds as an alternative to our Savings Bank account

- Typically used for parking of money for time periods upto 3 months

- No credit risk and extremely low modified duration

- Returns are predominantly from interest income – hence daily NAV movement is extremely stable

- Returns across different liquid funds is generally in a narrow range

- Hence, opt for well established funds with strong pedigree

So with that we come to the end of our liquid fund analysis and I hope you found it useful. Next week we shall discuss the remaining categories.

Happy investing 🙂

Disclaimer: No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments

Hi,

Well articulated article. Could you please throw some light on taxation part of liquid funds. IMO when one keep amount in Saving account he doesn’t bother about the taxation part, but in the case of investing and redeeming in a liquid fund, one has to keep track for taxation purpose. This is the only thing that pulling me back fro investing in a liquid fund. For example, if I keep 1 L in my saving account that gives an interest of 4% I’ll earn a profit of 4,000 by the year end that will be tax-free (as it is less than 10,000). But if I keep 1 L in a liquid fund that gives an interest of say 8% then by the year-end my profit would be 8,000 but if I am redeeming it then this 8,000 will be added to my income and will be taxed as per my tax slab.

LikeLike

Thanks Alok. You are absolutely right on the taxation part. However on the need to track for taxation purposes, though your interest from savings bank account is not taxed when it is less than Rs 10,000, when filing for taxes, you still need to declare the interest received from your savings account to “Income from other sources” and then claim deduction under section 80TTA. So irrespective of whether it is liquid funds or savings bank account we still need to track the interest income received for filing taxes (most of us don’t do that is a different issue :))

LikeLike

Hi Arun,

Thanks for writing this 3 series post on Debt Funds investing. I have a question regarding Liquid funds. You have mentioned that with increase in Interest rates, the returns of the Liquid funds should increase and with decrease in interest rates, the returns should decrease.

In case of IDFC Cash fund, which we discussed above in the event of interest rate increase, the returns had gone negative for one day. But will the returns be higher eventually because of the interest rate increase?

And likewise for any fund, where the modified duration will be a smaller number the returns will be higher with high interest rate?

Thanks,

Amar

LikeLike

Hi Arun,

How come YTM increases 2% if interest rates increase 2%. All the portiolio under liquid fund matures in 91 days. I don’t think YTM should be impacted by interest rate increase, it should remain same.

Thanks,

Narasimha

LikeLike