I have been running a live SIP portfolio of Rs 30,000 per month since Aug-2018 with the intent of motivating you to start yours. You can find the details here

I had planned to do a review every six months. But due to my brother’s marriage recently and some other unexpected commitments, I couldn’t stick to the time line. I am really sorry about this and hope to stick to the 6 month reviews regularly in the future.

Here goes the 1st review of my existing SIP..

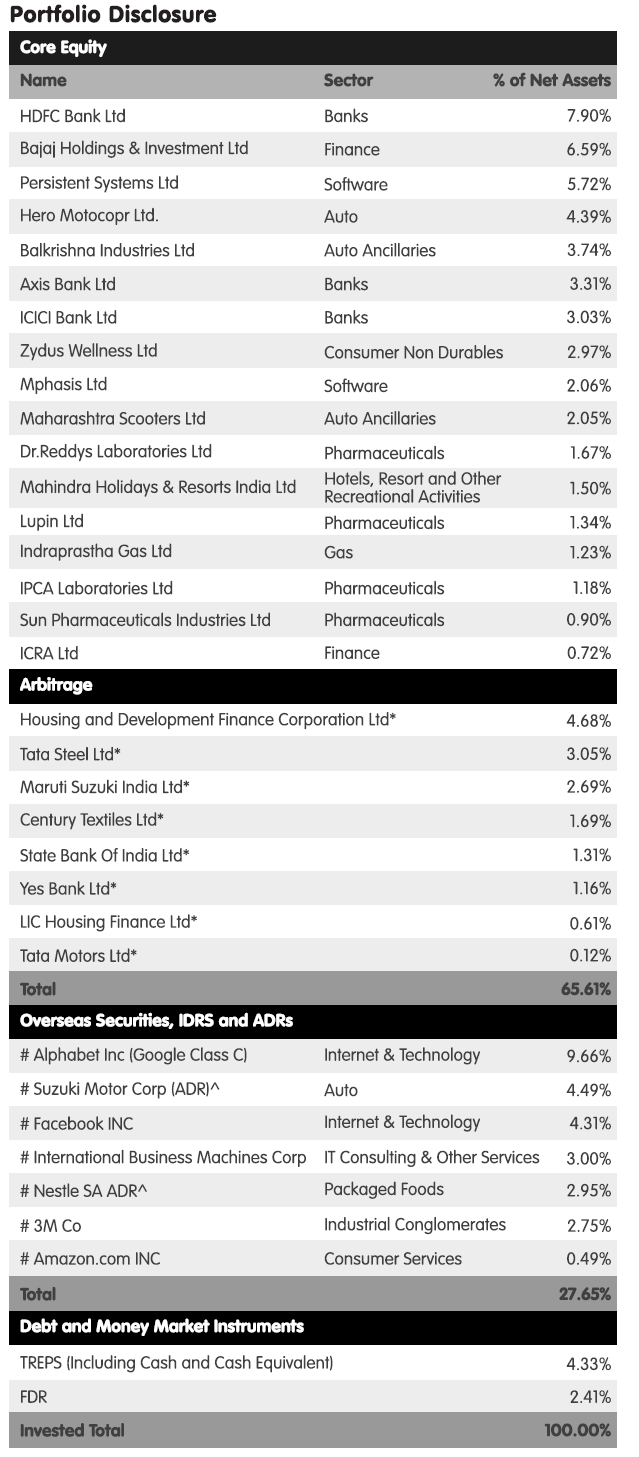

Fund 1: Parag Parikh Long Term Equity Fund

You can refer to the earlier rationale here

Latest factsheet (as on 28-Feb-2019): Link

- High Conviction

- Original Rationale: The entire fund house just has one single equity fund – and this single fund runs a concentrated portfolio of around 20-25 stocks. So all the resources will be focused on this single fund and shows their conviction and belief. This is a welcome change from the majority of AMCs where they have several funds running different strategies so that at all points in time there will be one fund or the other performing.

- Current View: Logic continue to hold true. They might launch an ELSS fund which will be very similar except for the global exposure (which again is because regulation doesn’t allow global exposure for ELSS category)

- Skin in the game

- Original Rationale: Their own employees own around 10% of the scheme

- View: While this has no prediction capabilities on the future performance, this is a sign that we are partnering with people of integrity. Currently it is at 7% as the scheme size has also grown (Rs 1,618 cr as on 28-Feb-19 vs Rs 1,186 cr in 31-Jul-2018).

- Simple to track

- As there are only 20 stocks and churn is low

- View: The current portfolio has around 25 stocks and is very easy to track

- Clear communication

- These guys are way ahead of the industry and have phenomenal transparency in communicating their views and process. They have a good youtube channel (link) where the fund managers regularly communicate their views and also their annual investor meeting is available where they talk about the investment thesis behind their stocks.

- View: They continue with their frequent communication via their youtube channel.

- Portfolio Construction:

- Fund Managers:

- The fund managers Rajeev Thakkar and Raunak Onkar continue to manage the fund which was my original thesis. So no worries!

- Exposure to global stocks

- The fund provides diversification via 1/3rd exposure to global stocks

- View: The global equity exposure remains around the same levels. Amazon stock has been added recently and all other stocks remain the same

- Expense Ratio:

- Their expense ratio has reduced from 1.5% to 1.4%. Lower the cost the better for us!

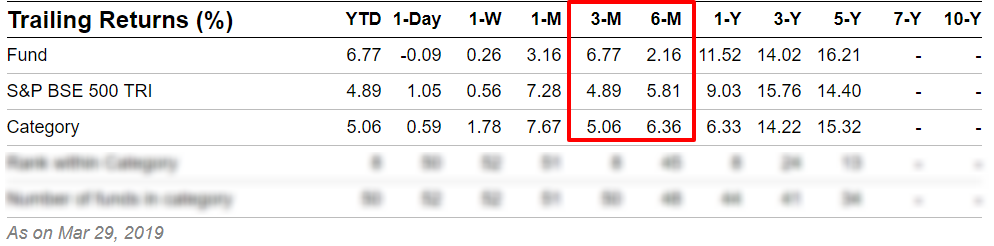

- Performance:

- 6 months is too short a period to evaluate. At least 3-5 years is needed to evaluate performance metrics. But nevertheless, just to get a sense of what has happened..

- Worry Points:

- Around 20% is in Cash positions (arbitrage and cash). While they have clearly communicated that they will be taking cash calls, personally I don’t prefer fund managers taking cash calls. However, given their overall positives, this is an issue that I will live with.

Overall, our thesis remains intact and I will continue with my SIP in Parag Parikh Long Term Equity Fund

Fund no 2: ICICI Prudential Large and Midcap Fund

The primary thesis (refer here) was based on the fund manager Naren. Here is a snapshot of why I like him

- 27 years of Market experience covering 3 cycles

- 13 years of fund management experience

- Robust long term performance track record

- Consistent Investment Style = Value investing + Contrarian + Evaluating Cycles + Top Down (using the big picture to arrive at stocks to invest in) + Bottom Up

- Macro overlay + takes advantage of cycles

- Knowledge of credit markets and credit cycles – its interplay with equities

- Ability to withstand and stick to investment process during occasional periods of short term under performance

- Widely read

- Investment Gurus – James Montier, Howard Marks, Michael Mauboussin

- Deploys checklists for investing – inspired from Atul Gawande’s Checklist Manifesto

- Communicates strategies and thought process regularly on public forums (making our lives a lot more easier)

To play the contrarian style, you need to be willing to look wrong often in the short term, before the mean reversion takes place. This means you need the support and trust from both the AMC and investors. Naren’s experience and stature allows him the rare luxury to take near term pain and stay patient till the contrarian call plays out (which a lot of new fund managers will never have as the short sighted industry won’t let him/her survive)

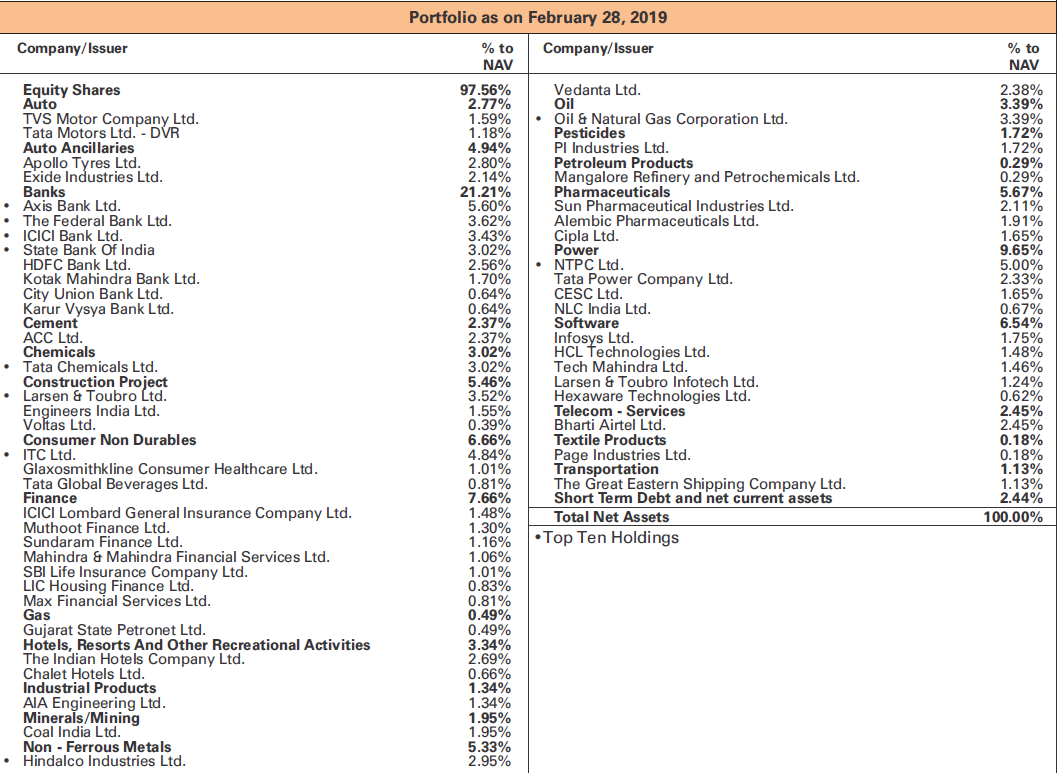

Current Positioning:

” Our earlier large-cap bias helped us because the recent correction was largely in mid- and small-caps. As a result, the worry about overvaluation in mid- and smallcaps has also come down. Across market cap segments, on an average, valuations remain slightly above average. Just like the large-cap space, we see opportunity in the mid- and small-cap spaces now as there are pockets that are cheap while some continue to remain expensive. In other words, we have shifted from a large-cap bias to a multicap bias.

We are of the view the NPA cycle has bottomed out. We have more of corporate facing banks in our portfolios now. Regarding the losses, lot of it is because of NPA provisioning recognised earlier. The operating profits of corporate banks are steadily improving. ” – Naren interview

Source: Link

As seen above, the fund has around 40% in mid and small caps – in line with what he has communicated. True to his contrarian style, he has reasonable exposure to Corporate lenders, Power sector and Metals.

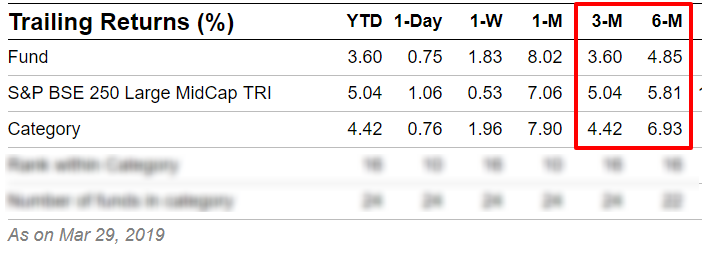

Performance:

As mentioned earlier 6 months is too short a period. But anyways just for our reference

Worry point:

Recently there have been few fund manager exits from ICICI Prudential Mutual Fund. Now a lot of funds have Naren’s name attached to it as a fund manager. This is completely opposite to PPFAS where the entire team has just one fund to manage. Bandwidth can become an issue and there is always a concern on whether enough attention would be paid to our selected fund.

View:

As of now, I will continue with the fund and I don’t see any deviation from the stated style of contrarian value investing. Naren’s bandwidth issues will be something which will be nagging at the back of my mind.

Actual SIP Performance

8 months of investing Rs 30,000 per month (As on 15-Mar-2019)

Strange Realization

If not for this public commitment to invest every month, I would have most probably spent this money at some pub, on late night cravings at Swiggy, some unwanted item at a huge discount on Amazon or some new fancy gadget. Suddenly I have realized something which is extremely understated – More than the fund selection, I guess for the first few years, my new found ability to save regularly will actually have a far larger impact on my portfolio value!

What to expect in the next 6 months?

I had discussed a new framework to set expectations for equities as an asset class here.

The rough math goes like this,

For a 6 month SIP of Rs 10,000 (i.e an investment of Rs 60,000 in total) – the portfolio value usually (read as 95% of the times) has ended up in the range between Rs 50,000 to Rs 80,000.

The worst ever value has been at Rs 40,000.

The above value has been calculated using Nifty (from 1990)

So for my Rs 30,000 SIP, I expect my portfolio to be usually between Rs 1.5 to 2.4 lakhs post 6 months.

But here is the catch. Since my first six months is over, as on 05-Feb-2019, I had already accumulated around Rs 1,75,000 (I have not included the Rs 30,000 invested on that day).

This Rs 1,75,000 is like a lumpsum amount going forward as the entire amount is exposed to equity market ups and downs. So, while the next six month SIP of Rs 30,000 normally will give me between Rs 1.5 to 2.4 lakhs , we also need to figure out the 6 month 95% probability range for my Rs 1.75 lakhs which has already been accumulated.

Based on historical data, the 6 month 95% probability return range for equities has been anywhere between -26% to +52%. Applying this to 1.75 lakhs we get a 6 month outcome range of Rs 1.3 to Rs 2.6 lakhs

So adding both we can get our normal range of expected outcome for the next 6 months.

In the next six months, that is on 05-Aug-19,

I would expect my portfolio (actual investments of Rs 3.6 lakhs) to be between Rs 2.8 to Rs 5 lakhs. This would be considered as normal behavior from my portfolio.

That being said, if there is a major crisis event, then my portfolio can fall even more than this. It is reasonable to expect one or two major crisis event every ten years.

I have a 10+ year time frame for my SIP. This means I have 20 six month periods to stay invested. Even if I lose out on a few periods, going by history of equities, majority of six month periods will be in my favor and hence I get to experience better returns over the long run.

In a similar manner, you can start building reasonable volatility expectations over the next 6 month period for your SIP portfolio.

The key idea is to stay for long term returns, one six month period at a time!

See you folks. Happy investing 🙂

Do share your feedback and let me know if it works for you. If you need any help regarding your investments you can also mail me at rarun86@gmail.com.

Happy investing as always!

If you loved this post, share it with your friends and don’t forget to subscribe to the blog via Email (1 article per week) or Twitter along with the 6000+ awesome people. Look out for some fresh, super interesting investment insights delivered straight to your inbox.

You can also check out my other articles here

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments.

First of all, again many thanks for your honest portfolio review which was promised periodically.

But, more important is the fact that it is extremely honest review of the portfolio and that too, with real ‘skin in the game’.

On Business Channels, there are numerous analysts and experts come and almost all of them, admit that the stock they have recommended are ‘not’ in their portfolio; they might have advised their clients for the same. How nonsensical it is. You are advising and recommending something which you yourself do not have the conviction of putting into your own portfolio.

You are not only holding it, but, even have given an honest and fair analysis of your portfolio.

LikeLike

Thank you so much for the kind words. Your feedback really means a lot to me.

LikeLike

Would love to see a hypothetical post on how would you incorporate asset allocation strategy – assuming (i) the current portfolio has gone beyond the normal portfolio range, (ii) You have some money in debt (elf/ppf/fd/nsc/…), (iii) after few years, so that corpus is of decent size, say 8th year.

Thank you for writing these posts and sharing frameworks. I really admire your effort. I always learn something from them, even on repeated reads.

LikeLike

Thanks a ton Shree. I will soon publish a post on how to handle asset allocation.

LikeLike

Additionally, how would you go about dealing with change in fund manager ?

I have been investing in DSP Top 100 for ~9 years. I am not happy with fund performances and many fund manager changes. It would be nice to hear your strategy. How much weightage should one give to LTCG when gains are more 1L?

LikeLike

The call needs to be taken on 1) How the fund was earlier positioned in the Portfolio (for playing value, growth, mid cap , small cap, focused etc) 2) View on new fund manager 3) How does his investing style and strategy fit into our overall portfolio.

If you are not satisfied by the long term performance of your fund then you should just go ahead and change. LTCG shouldn’t affect your decision.

LikeLike

Hii Arun what is your view about below sip and lumpsum portfolio.

SIP

L&T midcap direct fund-5000

Reliance largecap direct fund-2500

SBI smallcap direct fund-5000

Mirae asset emerging bluechip fund-5000

Axis bluechip direct fund-5000

JM core 11 direct fund-2500

Lumpsum basically for swp

L&T midcap-100000

Canara robeco emerging equity direct fund-100000

Tata equity pe direct fund-100000

HDFC smallcap direct fund-50000

Mirae asset India equity direct fund-50000

ICICI Bharat 22FOF DIRECT fund-25000

Tata index direct fund-50000

Kindly advise

LikeLike

Too many funds!

LikeLike

Hello Arun,

Recently discovered your blog and i find it interesting for a new investor like me

Please comment on my portfolio

ICICI Pru Liquid Direct-G – 10,00,000

UTI Liquid Cash Direct-G – 10,00,000

Investment horizon – less than 2 years

ICICI Pru Multi Asset Direct-G – 5,50,000

Parag Parikh Long Term Equity Direct-G – 5,50,000

Quantum Long Term Equity Value Direct-G – 5,50,000

UTI Nifty Index Fund Direct-G – 5,50,000

UTI Nifty Next 50 Index Fund Direct-G – 5,50,000

Investment horizon – 20 years

Monthly SIP

ICICI Pru Multi Asset Direct-G – 30,000

Parag Parikh Long Term Equity Direct-G – 30,000

Quantum Long Term Equity Value Direct-G – 30,000

UTI Nifty Index Fund Direct-G – 30,000

UTI Nifty Next 50 Index Fund Direct-G – 30,000

LikeLike

With that kind of investment every month i.e. 1.5lacs pm you are better off with a Advisor

LikeLike

Hi Vinay…investments are made by me after consulting with a freelancer financial advisor ….thanks.

LikeLike

Another awesome post. Neat ideas on how to do a methodical review and “range check” the corpus accumulated so far. Perhaps you could make a simple 10min fund review check list out of these?

LikeLike

Great idea. I will do that. Thanks 🙂

LikeLike

Hi Arun,

Just dropped in. Interesting and GENUINE fundas.

Request if you could add DIY excel sheets and where one can get data for it.

Regards

LikeLike

Thanks Gopikrishna! I didn’t get the DIY excel sheets part. What details do you want?

LikeLike

I am a 35-year old- private sector employee. I am planning to start SIPs of Rs 7,0000 in below funds

DSP Blackrock Microcap -INR 5000/-

SBI Small Cap-INR 5000/

Mirae Asset Emerging Bluechip Fund (G)- INR 25000/-

Parah Pareek-INR 25000/

L&T Midcap-INR10000

I have an Investment horizon of 10+years. I have a High moderate risk profile. Please share your thought. Your blog has been really helpful for beginners like me,

LikeLike

Sir, you are having only 2 funds in your portflio?

How should a noob divide the percentage in equity, debt etc.? Please share the link if you already have written an article on the same.

LikeLike

Hi Arun, Can you look into my portfolio and provide information. My aim is retirement funding and have no plan of touching the investment for 10 Years. Apart from mandatory investments like PF/VPF/NPS ,I have started the below SIP’s .

1)Quant Active Fund-Direct Growth-INR 2500

2)ICICI Pru Technology Fund-Direct Growth-INR 2500

3)PPFAS Long Term Equity Fund-Direct Growth INR 2500

4)PPFAS Tax Saver Fund – INR 1500

5)SBI Small Cap Fund Direct Growth -INR3000

6)SBI Focused Equity Fund Direct Growth -INR3000

7)Mirae Asset Emerging Bluechip Fund (G)-INR2500

8)Axis Focussed 25 Direct Plan Growth-INR 2500

I have invested in Aditya Birla

Aditya Birla Sun Life Tax Relief’96 Fund- (ELSS U/S 80C of IT ACT) – Growth-Direct Plan-INR 60000-SIP Stopped this month(3000/-)

DSP Tax Saver Fund – Direct Plan – Growth-INR40000-SIP Stopped this month(2000/-)

Also I have an investment of INR 50000 in Kotak Gold Fund – Growth.

kindly advise if the choices are appropriate for a long term wealth generation. 10 Years plus is what my plan is for the SIP’s.

LikeLike