In our last week’s post here, we had explored how our lizard brains which evolved millions of years ago are still stuck with their primary functions of ensuring our survival and hence end up doing a messy job when it comes to handling falling markets.

Today, we will explore the second behavioral enemy – Loss Aversion

Loss Aversion – Pain from a financial loss is twice the pleasure from a similar gain..

Behavioral scientists Daniel Kahneman and Amos Tversky have done several experiments to understand how we humans psychologically react to losses vs gains.

Their key finding was that:

- We all hate losses more than we love gains (duh, didn’t we all know this)

But here is where it gets interesting

The pain from a financial loss is almost two times the pleasure derived from a similar gain!

- The result is that investors tend to make poor decisions as a consequence of trying to avoid the pain of a relative or absolute loss

- This phenomenon is called loss aversion

Source: Franklin Templeton

So as the equity markets fall, the emotional pain that we experience is much more intense than the pleasure we had earlier experienced from similar gains.

Frequent monitoring of portfolios aggravates loss aversion..

Now as if this emotional pain was not enough, we further aggravate it with yet another behavior of ours – frequent monitoring of portfolios

The advent of mobile apps, has made it much more convenient to track our portfolios anytime, anywhere.

But this has a flip side, as it has been found out that:

The more we evaluate our portfolios, the higher our chance of seeing a loss and, thus, the more susceptible we are to loss aversion

In a market correction usually we are anxious of what if this extends and becomes permanent. This usually leads us to monitor our portfolios more frequently during a market correction (based on anecdotal evidence witnessed from our clients).

Suddenly we have a deadly situation – Loss aversion on steroids!

The reason why most of us panic and sell during a market correction must be obvious to you by now..

The lethal combination of loss aversion and frequent portfolio monitoring implies significant emotional pain during a market correction. In an attempt to avoid the pain we end up selling our equities.

But wait a minute, are we missing out something..

More than what meets the eye..

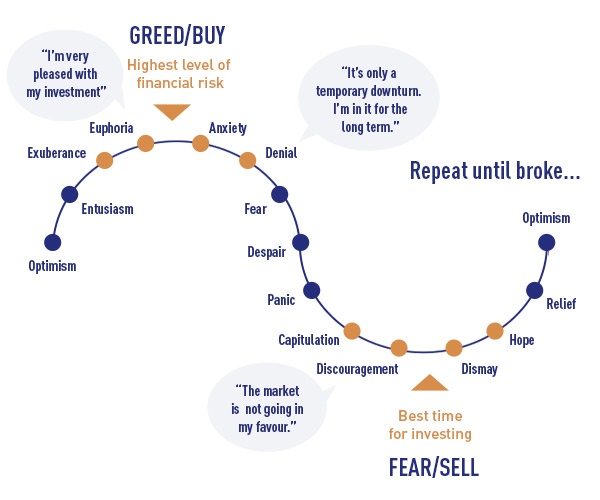

Now if this was the case, then most of us must actually end up selling our equities in the initial stages of a correction. However, historically investor behavior during a bear market suggests that majority of investors hang on for the initial part of the correction and usually cave in close to the bottom of the market.

Investor emotions gradually moves across..

Initial stages of fall – “It is only a temporary decline. I am in for the long run”

As the fall continues and prolongs – “Phew. I give up. Maybe the markets just aren’t meant for me”

What explains this?

To understand this peculiar behavior we need to explore two more behavioral quirks

- Our Pattern Seeking Brain

- Cognitive Dissonance

Our Pattern Seeking Brain – The desire to see patterns in the market and extrapolate them into the future..

“Humans have a remarkable ability to detect patterns. That’s helped our species survive, enabling us to plant crops at the right time of year and evade wild animals. But when it comes to investing, this incessant search for patterns causes more heartache than anything else.” – Jason Zweig

Our brains are hard-wired to believe we can predict the future and make sense out of random patterns. In fact, it even, it even rewards us for doing so.

Further, according to the author Dan Solin,

The brain of a person engaged in pattern seeking and prediction, experiences the same kind of pleasure that drug addicts get from cocaine or gamblers experience in a casino.

Thus our never ending search for patterns in the equity markets leads us to assume that order exists in the markets. However the harsh reality is that stock markets are far more random and unpredictable than we like to admit.

Let’s put his insight into the current context..

The Indian equity market (represented by Sensex) is down ~10%

What will happen to the markets going forward? Will the correction continue?

The honest answer is “I don’t know” (an even more honest answer is no-one knows)

But unfortunately our pattern seeking brain is already on to its prediction mode..

All recent market corrections have been followed by a sharp recovery – Taper Tantrum in 2013, China concerns & Oil crash in 2015-2016, Demonetization in fag end of 2016

So our pattern seeking brain expects the same pattern to repeat this time too.

So we ride out the initial part of the decline as we expect the earlier pattern of quick recovery to repeat. Now if it repeats, well and good. Else we are in for a shock!

Eventually in equity markets, it is only a matter of time before which the pattern gets broken and the market decline prolongs. (but when it happens is anyone’s guess)

And the moment our identified pattern is broken, all hell breaks loose. We panic, our predictions go for a toss and you know the rest of the story –

We end up selling near the bottom!

Let us move on to the second explanation of why we panic close to the bottom.

Cognitive Dissonance: The action-belief mismatch..

The psychological discomfort that we feel when our actions are not aligned with our beliefs is called cognitive dissonance. All of us strive to avoid this as much as possible.

When cognitive dissonance happens, we try to reduce in different ways.

Remember the Aesop’s fable – ‘The Fox and the Grapes”..

Driven by hunger, a fox tried to reach some grapes hanging high on the vine but was unable to, although he leaped with all his strength.

As he went away, the fox remarked, “Oh, you aren’t even ripe yet! I don’t need any sour grapes.”

The problem is that in order to reduce the dissonant feeling we can sometimes become biased to self-deception. We can be drawn into simplifying narratives or illusions or become guilty of rejecting valid but contrary viewpoints.

In a bear market, here is how cognitive-dissonance plays out in an investor

Most investors have created a self image of being a good decision maker. They believe they are intelligent and diligent investors and can predict the markets.

In a falling market, as our investments decline in value, we don’t like to admit that we were wrong. Cognitive dissonance sets in as the new reality – that our investments have declined conflicts with our own view of us being good decision makers.

Selling and realizing a loss only reinforces this and hence we will be reluctant to realize losses even when investment performance is bad. This leads to what is called the “disposition effect.” i.e we stick to our investment holdings despite loss.

As the market fall continues, the cognitive dissonance continues to increase, but at the same time we cannot sell as it would hurt our ego and self image.

How do we find a way out of this?

As always, we come up with a cunning solution..

Looking for someone to blame

The solution is simple – Let us put the blame on someone..

“My advisor is a cheat..he should have seen this coming”

“My fund manager sucks”

“The broker recommended me this dud stock”

Phew. Now that we have a scapegoat, we can relax. We suddenly find this a behaviorally easier solution to resolve our cognitive dissonance as we can still can maintain our positive self-image.

And hence we end up selling, and at the same time manage to keep our self image intact!

Bear market behavior – Complex interplay of loss aversion, frequent monitoring, pattern seeking brains and cognitive dissonance

In the initial part of the market decline, the tendency to sell due to emotional pain from loss aversion and frequent monitoring is negated by our pattern seeking brain (which expects a quick recovery as seen earlier) and cognitive dissonance (which doesn’t allow us to sell to maintain our self image)

But as the decline extends and takes the form of a bear market, the emotional pain pain from loss aversion and frequent monitoring significantly increases. Further the earlier patterns are also broken and we seek to resolve our dissonance by blaming someone else.

As all these factors come together, we usually end up selling near the bottom of the bear market.

This post is not designed to argue that we should not sell equities in a bear market – in fact if the earlier investments were bad it makes all sense to sell out as early as possible.

However if the investments are good and a long term investment strategy is in place, panicking and not sticking to the plan can have disastrous consequences for us.

Thus the idea is to highlight the distinct behavioral challenge that all of us will face in a bear market.

Quick Summary

- Loss Aversion

- The pain from a financial loss is almost two times the pleasure derived from a similar gain!

- The result is that investors tend to make poor decisions as a consequence of trying to avoid the pain of a relative or absolute loss

- Frequent Monitoring

- The more we evaluate our portfolios, the higher our chance of seeing a loss and, thus, the more susceptible we are to loss aversion

- The lethal combination of loss aversion and frequent portfolio monitoring implies significant emotional pain during a market correction.

- Pattern Seeking Brain

- Our brains are wired to seek patterns

- Our brains are still stuck in the earlier patterns of intermittent declines followed by quick recovery which is common in a bull market

- The brain expects this correction to be no different and hence doesn’t want to sell right now

- As the market fall extends, the pattern breaks, we panic and its the same story – we sell close to the bottom!

- Cognitive Dissonance

- The psychological discomfort that we feel when our actions are not aligned with our beliefs is called cognitive dissonance

- Most investors have created a self image of being a good decision maker

- A falling market conflicts with the self image

- In the initial part of the fall, we hold on our equities to maintain self image

- As the fall extends, we remove cognitive dissonance by blaming the poor decision on the advisor, broker or fund manager – and at the same time maintaining our self image

- Thus we end up selling close to the bottom

- In the initial part of the market decline, the tendency to sell due to emotional pain from loss aversion and frequent monitoring is negated by our pattern seeking brain (which expects a quick recovery as seen earlier) and cognitive dissonance (which doesn’t allow us to sell to maintain our self image)

- But as the decline extends and takes the form of a bear market, the emotional pain pain from loss aversion and frequent monitoring significantly increases. Further the earlier patterns are also broken and we seek to resolve our dissonance by blaming someone else.

- As all these factors come together, we usually end up selling near the bottom of the bear market

Now while there is an urge to come up with a solution to address this, the idea is to explore all other enemies, gain a holistic perspective as we connect the dots and at the end of it come with a solution to fight them all (hopefully).

So I plead patience for a few more weeks.

Till then, happy investing as always

For the rest of us, if you loved what you just read, share it with your friends and don’t forget to subscribe to the blog along with the 3500+ awesome people. Look out for some free, super interesting investment insights delivered straight to your inbox. Cheers!

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments

One thought on “Oops the markets are falling – Spying on investor behavior – Part 2”