Backdrop

I have been running a live Equity SIP portfolio with the intent of motivating you to start yours.

Here is how it was done:

- Rs 30,000 per month since Aug-2018 till Jul-19

- Rs 40,000 per month since Aug-2019 till Jul-20

- Rs 50,000 per month since Aug-2020 till Jul-21

- Rs 60,000 per month since Aug-2021 till Jul-22

If you are interested in how it all began, you can read the story here.

Now if you don’t have the time to read the original post, here is the plan in a nutshell…

You can check the previous reviews below

It is three years and time for our yearly review!

Checklist

- Did you invest every month?

Yup! - Did you increase the savings amount after every year?

Yup! Last month, I have increased by another 10K (from 50K to 60K) exactly as per plan. - Do you have a long time horizon to even out the ups and downs?

Yup. 10-15 years easily. - Does the overall performance fall within your 6 month return expectation range?

- Any change in fund manager?

- Did the fund manager stick to the stated investment style?

- Does the original investment rationale hold?

- Do they continue to communicate their strategy?

- Is the churn low?

- Is the expense ratio reasonable?

- Fund Performance

- Risk

Let us address the questions from 4-12

Performance Check

One of the biggest issues when it comes to performance evaluation, is that we are sold equities with the wrong expectations. Mostly the pitch is 12-15% returns over the long run.

So anytime, the performance is below the expectation of say 12%, we get a doubt that “Hey! Maybe this is not working”.

The reality is that long term, is simply made up of several short terms where the returns have a wide range of outcomes. As several short term periods accumulate, the wide range of ups and downs even out to provide reasonable returns.

We needed a framework, to make sure short term expectations were set right so that we can hang on for the long run.

Now in the last review, based on the 6 month expectations framework that I discussed in that post, the expectations were…

In the next six months, that is on 04-Aug-2021,

I would expect my portfolio (actual investments of Rs 14.4 lakhs) to be between Rs 14.2 lakhs to Rs 28 lakhs. This would be considered as normal behavior from my portfolio.

Let us check the results as on 04-Aug-2021,

Great! The value is within our expected range. Equity asset class is behaving normally as per expectation and as we continue investing over longer time frames, the returns will be decent.

Overall the performance was better than the benchmark index Nifty 500 TRI, Nifty 50 TRI and Nifty Next 50 TRI as seen above.

So both the asset class and fund selection are working out as expected. The key is not to get too carried away by the higher than expected current returns and let us continue to focus on the process and keep things simple.

Now with that out of the way, let us dive into the two funds..

Fund 1: Parag Parikh Flexicap Fund

You can refer to the original rationale here

Latest Factsheet (as on 31-Aug-2021):

High Conviction

Original Rationale: The entire fund house just has one single equity fund – and this single fund runs a concentrated portfolio of around 20-25 stocks. So all the resources will be focused on this single fund and shows their conviction and belief. This is a welcome change from the majority of AMCs where they have several funds running different strategies so that at all points in time there will be one fund or the other performing.

Current View: Logic pretty much continues to hold true. As explained in previous reviews, they have launched an ELSS fund. But this will be very similar to the Parag Parikh Long Term Equity Fund except for the global exposure (which again is because regulation doesn’t allow global exposure for ELSS category)

Skin in the game

Original Rationale: Their own employees own around 10% of the scheme

View: While this has no prediction capabilities on the future performance, this is a sign that we are partnering with people of integrity and the intention will be do the right thing as their money is also invested.

Currently 156 crs (i.e ~1%) of the fund is owned by company employees. While it optically looks like the ownership is coming down, this is because the fund size has also grown. As more outside investors like us invest in the fund their ownership comes down.

Focused & Simple to track

The current portfolio has around 25 stocks and is very easy to track.

Clear communication

Original Rationale: These guys are way ahead of the industry and have phenomenal transparency in communicating their views and process. They have a good youtube channel (link) where the fund managers regularly communicate their views and also their annual investor meeting is available where they talk about the investment thesis behind their stocks.

View: They continue with their frequent communication via their youtube channel.

Investment Process & Style

You can find them discussing details on their investment philosophy and thought process here

The portfolio remains more or less the same with minor changes and the earlier discussed thesis continues.

There were:

No new additions to the Portfolio

2 exit from the portfolio – CAMS and Zydus Wellness

Low Churn:

The churn is very low at 16% indicating that they are walking the talk of a buy and hold strategy.

Fund Managers

The fund managers Rajeev Thakkar and Raunak Onkar continue to manage the fund which was my original thesis. So no worries!

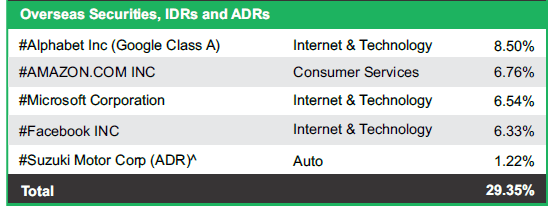

Exposure to global stocks

The fund provides diversification via 1/3rd exposure to global stocks. The global equity exposure remains around the same levels at ~29% (vs 29% six months back).

Expense Ratio

Their expense ratio has consistently been coming down.

Their expense ratio when I started was around 1.4%. It has been consistently coming down. During previous review it was 0.96%. Now its 0.87%. This is great. Lower the cost the better for us!

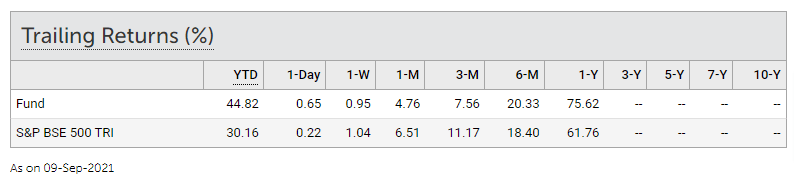

Performance

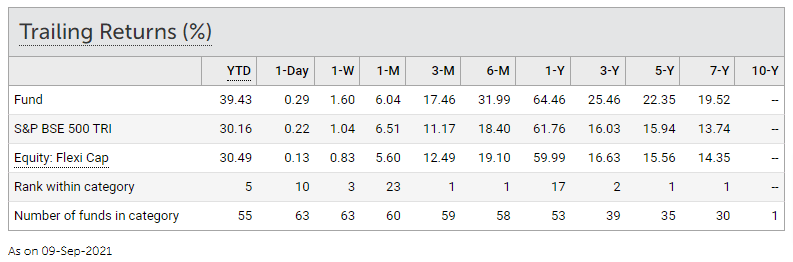

Here is how the fund has performed in the past

As seen above, the 5Y & 7Y performance indicates significant out performance against the benchmark and peer group. The fund is doing good as per my expectation.

Cash Allocation

In 2019 they had cash allocation of around 14%. I personally don’t prefer fund managers taking cash calls and hence had mentioned this as a concern. But as the markets corrected in February and March 2020, they had deployed the entire cash into equities.

Right now the debt + arbitrage allocation is around 7% and this is pretty normal and no worries as of now.

Overall View

Overall, my thesis remains intact and I will continue with my SIP in Parag Parikh Flexicap Fund

Fund no 2: ICICI Prudential India Opportunities Fund

The primary thesis (refer here) was based on the fund manager Naren. Here is a snapshot of why I like him

- 27+ years of Market experience covering 3 cycles

- 13+ years of fund management experience

- Robust long term performance track record

- Consistent Investment Style = Value investing + Contrarian + Evaluating Cycles + Top Down (using the big picture to arrive at stocks to invest in) + Bottom Up

- Macro overlay + takes advantage of cycles

- Knowledge of credit markets and credit cycles – its interplay with equities

- Ability to withstand and stick to investment process during occasional periods of short term under performance

- Widely read

- Investment Gurus – James Montier, Howard Marks, Michael Mauboussin

- Deploys checklists for investing – inspired from Atul Gawande’s Checklist Manifesto

- Communicates strategies and thought process regularly on public forums (making our lives a lot more easier)

To play the contrarian style, you need to be willing to look wrong often in the short term, before the mean reversion takes place. This means you need the support and trust from both the AMC and investors. Naren’s experience and stature allows him the rare luxury to take near term pain and stay patient till the contrarian call plays out (which a lot of new fund managers will never have as the short sighted industry won’t let him/her survive)

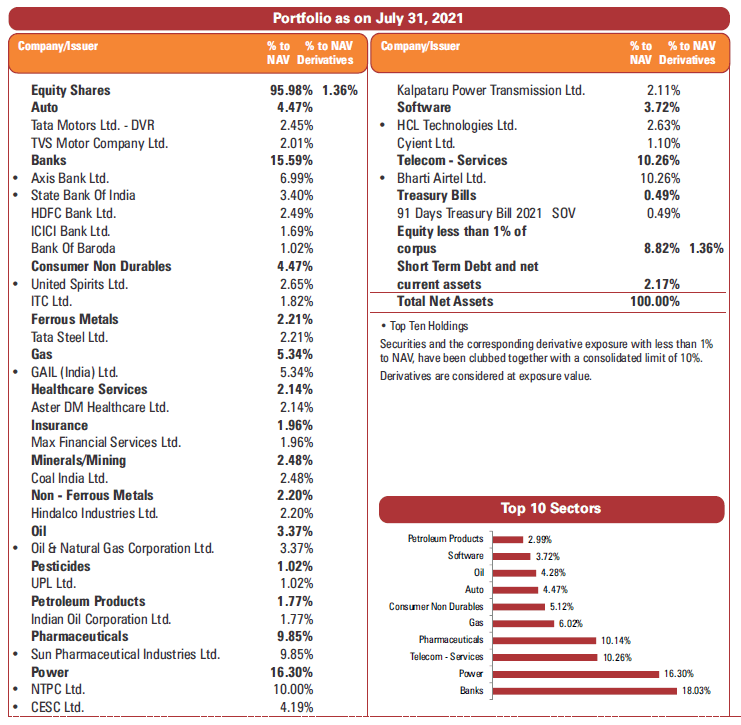

Portfolio Positioning of ICICI Prudential India Opportunities Fund

It is a top heavy concentrated fund with top 10 stocks accounting for 62% of the portfolio and 15 stocks accounting for ~75% of the portfolio. Overall it has around 41 stocks.

AUM size at Rs 4,090 crs implies significant flexibility to manage the portfolio across market caps.

Currently the portfolio has around 38% in Mid and Small caps which is similar to the positioning 6 months back.

Sector Views

Investments were predominantly into sectors which were going through near term pain thereby providing attractive valuations. Some of the positions have already started to play out. The portfolio is positioned for cyclicals and can do extremely well if economic recovery is strong.

Overweight:

- Power – 16% – NTPC, CESC, Kalpataru Power Transmission etc

- Corporate Oriented Lenders – 13% – Axis, SBI, ICICI, BOB etc

- Telecom – 10% – Bharti Airtel

- Oil & Gas – 10% – ONGC, GAIL, IOCL

- Metals – 7% – Coal India, Hindalco, Tata Steel etc

- Positioned for Cyclical recovery + PSUs + Dividend Yield plays

- 1/3rd of Portfolio Exposure to small and midcaps

Underweight: Retail Lenders, Quality theme

Valuations

Price to Earnings Ratio: 14.4

Price to Book Ratio: 1.7

(source: value research)

PE ratio at 14.4 times is also reasonable – providing significant valuation re-rating potential.

This is something I will monitor to get a sense of the value orientation of the portfolio.

Expense Ratio

The expense ratio is around 0.56% ( 0.64% in Feb-21) which is still pretty low and good!

Portfolio Churn

Portfolio Churn is neither to high nor too low at 56%. Given the part tactical nature of the portfolio I expect this to be around this range.

Performance

The fund was launched on 15-Jan-19 and hence has a short performance track record.

What was my view before 1 year…

The performance at that point in time was nothing to write home about. To be honest it was really bad.

This is what I wrote in my previous review:

This is in line with all value oriented fund managers under performing. If you notice all the celebrated value oriented fund managers before 2013 – Prashant Jain, Anoop Bhaskar, Quantum Mutual Fund, Sankaran Naren, Anand Radhakrishnan etc are underperforming big time. The new breed of Quality oriented fund managers have been strong performers in the last 7 years. I expect mean reversion to play out sometime similar to what happened to value oriented fund managers previously and the quality oriented managers to go through their lean patch.

What happened in the last 6 months

Post that there was a significant pick up in returns (not that I knew about the timing) and thankfully the thesis has started to play out.

That being said, this fund is not for the fainthearted and will have significant performance differential with indices in the short term (negative and positive) given the divergent and concentrated portfolio of beaten down stocks.

Personally, I would give it 3-5 years to see some strong outperformance.

Overall View

Overall, my original thesis remains intact, that I would want to play the contrarian style via Sankaran Naren.

Things under my control – Time & Discipline

Now while I have no control on the markets, the biggest determinant of my future portfolio thankfully is still under my control – Time + Discipline

Time – I have easily 10-15 years time frame. This would take care of most of the near term volatility and I can ride it out.

Discipline – To save and invest consistently, come what may. Call it the pressure of social accountability, I have managed to invest Rs 30,000 every month for the first 1 year, Rs 40,000 every month for the 2nd year, Rs 50,000 every month for the 3rd year. Now for the current 4th year, I have been investing Rs 60,000 equally split across both the above funds.

I continue to focus on the above two – Time and Discipline and hopefully in 10-15 years should have a good enough outcome

Next 6 month return expectation

I had discussed a new framework to set expectations for equities as an asset class here.

The rough math goes like this,

For a 6 month SIP of Rs 10,000 (i.e an investment of Rs 60,000 in total) – the portfolio value usually (read as 95% of the times) has ended up in the range between Rs 50,000 to Rs 80,000.

The worst ever value has been at Rs 40,000.

The above value has been calculated using Nifty (from the year 1990)

So for my Rs 60,000 SIP, I expect my portfolio to be normally between Rs 3 lakhs to Rs 4.8 lakhs after 6 months.

But I have already accumulated around ~Rs 22.9 lakhs as on 4-Aug-2021. (Just to make sure the six month review time lines are kept the same)

This Rs 22.9 lakhs is like a lumpsum amount going forward as the entire amount is exposed to equity market ups and downs. So, while the next six month SIP of Rs 60,000 normally will give me between Rs 3 to 4.8 lakhs , we also need to figure out the 6 month 95% probability range for my Rs 22.9 lakhs which has already been accumulated.

Based on historical data, the 6 month 95% probability return range for equities has been anywhere between -26% to +52%. Applying this to Rs 22.9 lakhs we get a 6 month outcome range of Rs 17 lakhs to Rs 35 lakhs

So adding both we can get our normal range of expected outcome for the next 6 months.

In the next six months, that is on 04-Feb-2022,

I would expect my portfolio (actual investments of Rs 18 lakhs) to be between Rs 20 lakhs to Rs 40 lakhs. This would be considered as normal behavior from my portfolio.

That being said, if there is a large market crash (whose reason we will know only in retrospect), then my portfolio can fall much more than this. It is reasonable to expect one or two major crisis event every ten years. (the covid crash of 2020 is a nice reminder of this)

I have a 10-15 year time frame for my SIP. This means I have 20 to 30 six month periods to stay invested. Even if I lose out on a few periods, going by history of equities, majority of six month periods will be in my favor and hence I get to experience better returns over the long run.

In a similar manner, you can start building reasonable volatility expectations over the next 6 month period for your SIP portfolio.

The key idea is to stay for long term returns, one six month period at a time!

Summing it up

The whole idea is not to ask you to pick these 2 funds. That is irrelevant. The actual intent is to encourage you to save and invest steadily across your working careers. 10-15 years down the line, irrespective of which fund you pick (as long as you don’t mess it up big time) you will end up with a great outcome.

I honestly think if we plan our money well, then it can make a huge difference to our lives and the people around us. The idea behind this blog is that in a small way, if I can help you make good money decisions today, maybe I can someday create a big difference to your lives.

Ok, sentiments aside – the next review will be on Feb-2022.

See you folks. As always Happy investing!

If you have any feedback you can also mail me at rarun86@gmail.com.

If you loved this post, share it with your friends and don’t forget to subscribe to the blog (1 article per week) or Twitter along with the 8000+ awesome people. Look out for some fresh, super interesting investment insights delivered straight to your inbox.

You can also check out my other articles here

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments.

Hi Good to see your post.

I had started with you in PP Flexicap Fund. It was great decision.

I did manual SIPs only and did not automate every month. So, now a days, as markets are ATHs , I am finding it difficult to put more money.

One question, will you take any decision on stopping SIP or do you have any model , in case, markets rise to very high levels going further?

Thanks.

LikeLike

Hi, Right now since I have a long career ahead with regular cash flows expected, I don’t want to time the markets and its very difficult to get it consistently right. If markets correct that will be great, as I can accumulate a lot more mf units at lower prices. So since I have a long time frame and I dont need to withdraw money from this portfolio, I have the advantage of applying ‘wait for some more time’ strategy of required.

LikeLike

Great Work Arun! Hats off to your committment towards the blog among your schedule!

LikeLike

Arun I’m so grateful for all the hard work you are doing for community. I truly feel the I am fortunate to be able meet you here and twitter. Thank Arun from heart. keep it up man.

LikeLike

Thanks a lot Deepak for the kind words and support

LikeLike

The data, review and outlook are so useful. Thanks for sharing, keep it up.

LikeLike

Thanks a lot for the support and kind words 🙂

LikeLike

Where do u get the churn ratio?

LikeLike

Factsheet

LikeLike

Two points:

1. Your expectation has a very wide range (14.2 to 28 earlier and now 20 to 40 lakhs) to make a decent and fair comparison between your expectation and reality. It is like saying anything between earth, Sun and Moon is acceptable.

2. From 2019 onwards (i.e. around two years) is too short a period to again evaluate the performance. While I am not making any comment on the fund selection (they are exceptionally good), the fact that your fund selection has to undergo a market cycle to withstand the ravages. And during that time, it would be prudent to compare your selected funds’ performance vis-a-vis some other top rated funds just to draw some inference where other funds stand versus your selected funds in a down turn cycle.

LikeLike

The short term periods have a wide range of outcomes and these ranges are set based on historical volatility of equity. So being in the asset class I cant wish away the volatility.

The fund selection is not the real point. Any half decent fund will do a great job over the next 10-15 years. And the best fund will be known only on retrospect. The real idea is that – if someone simply starts their SIP and continues for 10-15 years, learning to live with volatility and ignoring all the distractions of which fund is better, is equity overvalued etc , the final outcome will come as a pleasant surprise.

LikeLike

1. Agreed with the implied volatility aspect. But as you are investing in a mf scheme, therefore, would volatility not be one of the parameters of shortlisting/selection of a mf scheme. Direct equity volatility would be different than mf scheme volatility. And if that’s the case, then, is the range ok.

2. Your point is well taken that if you invest for 10-15 years, then, one would get great returns (means beating all inflation and other parameters) among all asset classes and that one should remain focused and invested and that’s the crux.

LikeLike

You’ve provided detailed information about your whole SIP portfolio for the last three years. Thank you for sharing this information. Your blog has made me realize the investment opportunity I’m missing out on. I’m going to start investing in a SIP as soon as possible.

LikeLike

Thanks Jaswant. You made my day!

Happy Investing 🙂

LikeLike

Hey Arun, I just spent the last hour & a half reading your entire SIP journey.

Your posts are well written. I really like how you keep things simple. Also, that checklist at the top is something that I plan to steal for my bi-annual portfolio reviews!

I started my investment journey in Jan 2021, having missed out on both the crash & the bull-run that followed in 2020.

I wanted to know (only if you’re okay with sharing the info) – what other savings do you have?

People talk about having an “emergency fund” – for me that is a 3 lac FD in a bank account. What instrument do you use?

Then there are “tax savings” – I top up my PPF every year, but I read you use an ELSS. Which one in particular?

Anything else that a new investor should be looking into?

LikeLike

Hi Shadab,

Thanks for the kind words. I invest some more money in mutual funds (both equity and debt) and have around 20% in direct stocks. Since I have a long runway of cashflows and high risk taking abilities I have a high allocation to equities. For emergency fund, I use Liquid funds and for tax I use ELSS.

LikeLiked by 1 person

Hi Arun,

considering the uptick in AUM and exposure limits to foreign stocks, would you still continue with PPFAS?

LikeLike

As of now, yes!

LikeLike