These are difficult times for all of us. Most of us have aged parents and young kids about whom we are really worried. I am no exception. I really hope a solution is found soon and we get back to our normal lives.

If you have benefited from reading this blog, as a small favor, please do contribute and help the impacted people in your neighborhood. I am doing my small bit, and hope we as a community can be of some help.

Unfortunately, in a time like this, the equity market is not making our lives any easier. With a decline of around 30-35% in such a short span, our portfolios are adding to our anxiety levels.

While I am no market guru or expert, for whatever it may help, I thought sharing my thought process, struggles and journey through this bear market may provide some perspectives both for you and me!

One of the best things personally, is that thankfully I had a framework which I evolved over the last few years on how to approach bear markets whenever it happened.

Now, you may ask,

What is the big deal about a framework?

- Delayed Feedback

- Humans respond much better to prompt feedback than they do to delayed feedback

- Unfortunately, in equity investing, it takes at least 3-5 years (sometime even longer) to get the feedback on the correctness of your decisions

- Near term outcomes can sometimes be completely contradictory to long term outcomes

- I-Knew-It-All-Along effect

- After an event has occurred, we have a tendency to see the event as having been predictable even if we had little or no logical means for predicting it

- The problem is that too often while we actually didn’t know it all along, we feel as though we did

- This concept is referred to as hindsight effect or the knew-it-all-along effect

A combination of the above two means that 3-5 years down the line, based on the outcome there is a high chance that we will convince ourselves, that we knew it all along.

So the idea of a framework, is to check based on the feedback (maybe several years later) on whether it worked or not.

If not, we can always find out the loopholes and evolve the framework.

My Current Approach

A good starting point in investing, is to understand yourself better.

There are few things which I know reasonably well about me

Things I cannot do

- Personally I don’t enjoy stock picking much and hence have outsourced it to decent fund managers with experience and track record

- I cannot predict the exact level at which markets will bottom

- I have no expertise in analyzing a biological virus and how it spreads

My Strengths

- Long time frame – at least 15-20 years + Still Young + Long Career ahead

- Optimism + Faith in Equities: By nature I am an optimist and have strong faith in entrepreneurship

- Patience: I can hang on

- Ability to withstand declines: I can take up to 50-60% temporary paper losses

Keeping the above context in mind, I had a simple plan which goes like

- If markets fall 20% then I will: Invest 20% of my cash

- If markets fall 30% then I will: Invest 30% of my cash

- If markets fall 40% then I will: Invest 40% of my cash

- If markets fall 50% then I will: Invest 10% of my cash

I am reasonably sure about – my Long time frame and Faith in Equities. However Patience and Ability to withstand declines is something which is partly tested but unless this whole bear market ends, I am still not sure.

This leaves me with two challenges

- I might panic and sell my equities

- I might not be able to execute the plan as fear takes over

How do I protect myself from this ?

A few years back I had given a presentation to Tamil Nadu Investor Association on the psychological biases which we may encounter during a bear market.

You can go through the presentation here

Broadly I had identified 5 psychological biases which impact us in a bear market..

- Loss Aversion + Amygdala Hijack

- Obsessive Portfolio Monitoring

- Social Proof

- Expert Bias

- Regret

Given the last one month live bear market experience, I think there are few more in play

- Recency Bias

- Anchoring

The above mentioned psychological biases are most likely to get me in trouble.

Let me explain, how I plan to address all the above..

- Loss Aversion + Amygdala Hijack

- Obsessive Portfolio Monitoring

A million years of evolution has installed the ‘fear response’ in our brain. This response mechanism ensured that our ancestors were able to survive in a hostile and dangerous predatory environment.

But this survival response, when applied to investing can lead to bad outcomes.

What is my biggest risk?

Given the instant access to my investment app, it will take only ten minutes to exit my entire portfolio.

So I am just ten minutes away from a BIG MISTAKE if in case I panic.

How am I trying to address this?

Rule 1: See Me Not

The more I tend to see the losses in my portfolio the higher the emotional pain and increased odds of me panicking.

You can read more about this here

Since I hold only few funds managed by decent fund managers, I don’t have to worry too much on frequent monitoring.

So while I can roughly guess the degree of fall in my portfolio, I have never looked at the actual portfolio in the last one month.

This is working well for me.

Rule 2: Delay Investment Decisions by 48 hours

Any new decision beyond my plan that I have to make will be taken after a 48 hour cool down period and after market hours. This makes sure I have thought through the whole thing clearly.

The next psychological bias to address is

- Social Proof (When in doubt follow others)

- Expert Bias

When most of the people around us are becoming negative, it is extremely difficult to stand out and take a positive view.

We also have a natural tendency to give disproportional importance to the views of Investment Experts.

You can read more about both the tendencies from here and here

Rule 3: Be greedy when others are fearful

While everyone knows this Buffet Quote, how do you quantify this

I use a combination of the below factors to gauge the fear levels

- Valuations: MCAP/GDP, PB Ratio, PE Ratio, Earnings Yield vs Gsec Yields

- Volatility Index: India VIX

- Flows: Both FII and DII turning negative would indicate high fear (currently FII outflows indicate fear – but DIIs still holding on)

Rule 4: Remind yourself everyday – No one Knows

In a scenario where uncertainty remains high, we all crave for certainty.

Expert tag + Confidence + Precise Prediction = Wow! I Believe You.

The key is to keep reminding us that ‘no one really knows for sure’.

Just because it comes from a reputed investor or an investment expert it doesn’t necessarily have to be true.

We need to concentrate on their logic rather than their position, and should be open to challenge the claims they make.

Rule 5: Evaluate only views of experienced investors with a public track record of more than 15 years

I personally like to listen to views of experienced investors who

- Have a public performance track record over long periods

- Stay humble

- Prepare rather than Predict

Given the amount of noise, almost everyone seems to be a coronavirus expert. Everyone has a view on how the markets will play out.

In times like this, I prefer to keep the list of people I follow very minimal.

The next psychological bias to address is

- Regret

I know that from today’s valuation levels my odds of a good return over the next 3-5 years is significantly high.

But if I deploy the entire amount, what happens if markets fall further. I will regret having bought too early.

If I don’t invest and wait for a further fall, then if the markets suddenly rally, I will regret not buying at lower levels.

Rule 6: Opt for Regret Minimization rather than Return Maximization

The idea is to balance between – the regret of missing out if markets rally from here vs regret of entering too early if markets correct further .

My plan takes this into account as it takes a measured approach and incrementally deploys when markets fall. In this way, if the markets suddenly rally, at least I have some portion deployed, and if markets fall further I have cash to deploy.

Overall, the idea is to manage for our ‘regrets’ rather than trying to predict a precise outcome.

Am I sticking to my plan?

So far I have stuck to my plan and invested around 50% of my additional cash.

The levels in Sensex that I had planned goes like this

- Sensex at 34,000 – 20% of Cash

- Sensex at 30,000 – 30% of Cash

- Sensex at 26,000 – 40% of Cash

- Sensex at 22,000 – 10% of Cash

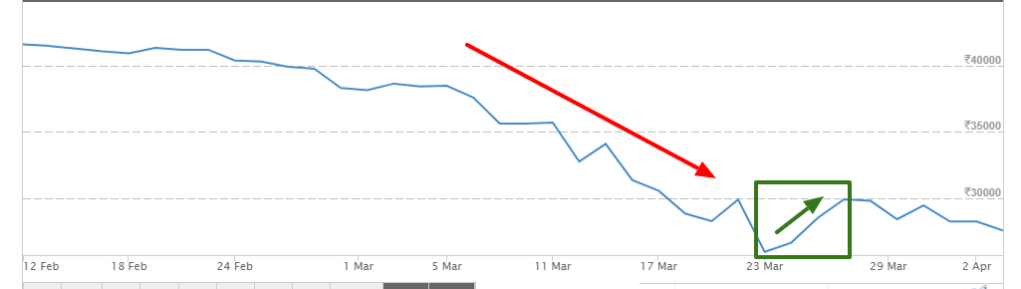

I had a small lapse in execution on 23-March where the Sensex cut 26,000 levels. I should have invested 40% of my initial cash. But I didn’t.

I fell for two traps – Recency Bias & Anchoring Bias

Because the markets had been continuously going down for almost 3 weeks, the recent falling trend started to play with my mind. Add to it the lock down announcements and day-to-day updates on new virus episodes.

Finally when Sensex reached, 26,000 which was my execution point, recency effect kicked in and I said let me wait.

And all of a sudden, markets started rallying. In the next 3 days it was up by 15% close to 30,000 levels.

I know there are usually several false rallies in a bear market. But I also know markets would recover much before the real economy. Market recovery usually doesn’t need good news but a small perception change from ‘things are really bad” to “things are bad but not to the extent we imagined”.

So suddenly, on one side there was the fear of what if this was the start of the recovery. I still have 50% of my amount not deployed. These type of falls are very rare. Have I missed the opportunity?

But strangely, I was also anchored to the 26,000 number. Somehow, because it had already hit the number, I also believed that it would come back soon. This was a live lesson for me in anchoring effect.

Now I am able to appreciate as to why people miss out on investing in recoveries. Because a lot of these false rallies, lull you into complacency. The news continues to be bad. Even a real recovery has lots of false intermittent declines. And most importantly we are still anchored to the lower levels.

With everything happening together, no wonder most of us miss the recovery bus.

And here comes the killer – the recoveries are extremely fast. Sample this: in 2009 recovery, the markets were up a whopping 85% in 3 months!

Phew. I don’t trust myself to handle this pressure.

For the remaining amount, I am contemplating a slight change in strategy considering the below factors

- The correction this time unlike 2008 was not from insane valuation levels

- The Earnings Growth Cycle is close to its bottom

- A 40% correction this time has brought most valuation metrics (except PE ratio) close to 2008 lows

While I have no clue where the bottom is, the regret of missing out will be more painful for me than the regret of possible near term temporary losses.

With my remaining amount, I am planning to participate with a daily staggered investment approach with lump sum allocation if Sensex cuts 26,000, 24000 and 22000.

Here is how it works

- Invest 1% every day into equities – do it via a Systematic Transfer Plan

- If Sensex cuts 26,000 – Do a lumpsum and invest upto 50% into equities

- If Sensex cuts 24,000 – Do a lumpsum and invest upto 75% into equities

- If Sensex cuts 22,000 – Do a lumpsum and invest 100% into equities

If interested you can read the complete detailed thought process here

Summing it up

Now the above thought process is not meant to be an advice. The plan will have to be evolved based on your time frame, risk appetite and own behavioral strengths and weakness.

The idea is to put in place a logical framework, so that in the future we can come back and see how it played out. If this works, great. If not, we can always find out where we went wrong and improve this.

Stay Safe, Stay Home and Stay Invested!

If you loved this post, share it with your friends and don’t forget to subscribe to the blog (1 article per week) or Twitter along with the 8000+ awesome people. Look out for some fresh, super interesting investment insights delivered straight to your inbox.

You can also check out my other blog articles here

I also write for my firm here

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments.

thank you for this detailed advise Arun! I’m keeping my mind of actively trading or trying to catch bottoms, by reading some good books on investing. Finished the little book of investing, now reading the intelligent investor. Interestingly, with markets at these levels we’re able ti find quite a good bucnh of low PB ratio and low PE scrips. Any other books/material you recommend for reading?

LikeLike

HI

What is your asset allocation ratio. I am more interested on the % of cash component. All equity + just emergency-funds (or) you have cash component that is used to deploy for bear market cases?

This 100% cash component you have to invest – is it coming from emergency fund?

I am following your advice ….thanks a lot for explaining your thought processes. A fellow chennaite !

LikeLike

This is so well written and so wonderful. Thank you so much for this! I’m bookmarking this article:-)

LikeLike

Very nice article! I enjoyed a lot Reading it. Thanks for sharing.

LikeLike