One of the questions that I have been confused for a long time:

Should you try and time the equity markets?

Now, in the first place, why do you want to time the markets?

Simple.

All of us, being the typical us, want long term equity returns but with minimal short term fluctuations!

Umm ok! I get the intent. But let us also listen to what few of the investing legends have to say regarding this

“There are only two types of people: those who can’t market time, and those who don’t know they can’t market time.” Terry Smith

“I can’t time stocks.. I don’t know anybody else who can either.” Warren Buffett

“I don’t think we would want a manager who thought he could just go to cash based on macroeconomic notions and then hop back in when it was no longer advantageous to be in cash. Since we can’t do that ourselves.” Charlie Munger

“We wish we had perfect market timing (as well as the ability to fly). The reality is that no one does or ever will.” Seth Klarman

“Active market timers usually fail.” David Swenson

“After nearly 50 years in this business, I do not know of anybody who has timed the market successfully. I don’t even know of anybody who knows anybody who has done it.” Jack Bogle

What does that leave us with?

Equity markets in the short term can’t be predicted. Period!

So far, so good.

But, here is where my confusion starts.

Does it mean, we stick to our same equity allocation indifferent to whether it was a period like 2007 (the peak of bull market) or 2009 (bottom of bear market).

Now we all know that, equity returns are in effect a sum of Valuation changes (PE Ratio change) + Earnings growth + Dividend yield (usually around 1.5%)

Valuations while not a great predictor of the short term returns, has been a reasonably good predictor of longer term returns (say over 5 years) as they usually mean revert. This topic has been covered in detail by an amazing blogger called Dev in his blog Stable Investor here. So let me not reinvent the wheel.

The higher the starting valuations the higher the odds of lower returns in the future. The lower the starting valuations, the higher the odds of higher returns in the future.

Further, Earnings growth is also cyclical and mean reverts. So a high earnings growth period, is usually followed by a lower earnings growth period and vice versa.

If we apply both of these together, we can get a rough sense of future returns. So shouldn’t we also adjust our equity allocations based on this view.

But wait a minute, doesn’t this mean we are getting into the dreaded market timing territory?

How do we solve for this conundrum?

My eureka moment came from a very normal mundane activity that we get to do almost everyday –

Driving in Indian roads

Yes! You heard that right.

The Indian roads have actually taught me more about risk management than any other investment book.

Let me explain..

The Inevitable Dents and Scratches

Let me start off with the current condition of my car 🙂

It’s five years since we bought this car. In the first year, both me and my wife were super obsessed about keeping our car scratch free. Then as with everything else in life, when our driving skills met the reality of Indian roads, we realized the sad truth. How ever careful we try to be, small dents and scratches were almost unavoidable.

Sometimes it is the neighbor’s kid who practices his new handwriting lessons on my car with a stone, the unexpected biker who just whizzes past knocking off my mirror, the all pervasive chennai auto guys who have mastered the art of turning right after signalling left. The list goes on..

For all those used to Indian roads, you know the story right.

Small scratches and dents are known risks which we have to live with if we want the comfort of travelling in a car. These are risks not under our control.

Similarly, in equity markets there are these small scratches and dents which we will have to incur regularly. These regular temporary declines is the emotional fees that we have to pay for participating in equities.

There is no wishing away this reality, and trying to predict every decline on a consistent basis is just not possible.

Historically for Nifty the intra year declines excluding the extremes has averaged around 20% decline.

Lesson 1: Regular moderate declines in the short run is the emotional cost that you have to pay for long term equity returns. You can’t predict and avoid them.

Major Accidents but not under our Control

My wife Shalini met with an accident a year back. She had parked the car in the side of the road and was waiting for her friend. A call taxi driver who was coming from behind unfortunately fell asleep, didn’t notice the car and banged right into the car from behind.

Thankfully while our car was badly damaged, Shalini was safe. The more we thought about this after the event, on how we could have prevented it, the harsh reality dawned upon us. Even if the same event was to happen the next time, there is absolutely nothing we could do about this to prevent it. The truth is that we have no way to keep every other driver on the road awake.

I once had a bad experience with a dog running into the wheels of my bike. Landed up in hospital for a day!

A few days back a large branch of a tree suddenly fell two feet in front of my bike while returning back home. Had I been 2 seconds early, I would have had a damaged head by now!

What if the road below you suddenly caves?

Now I am not making this up. This happened in Chennai 2 years back.

How in the world can someone predict this?

There are unknown risks which can cause major accidents, and unfortunately we have no control over them. The only solace being they are pretty rare.

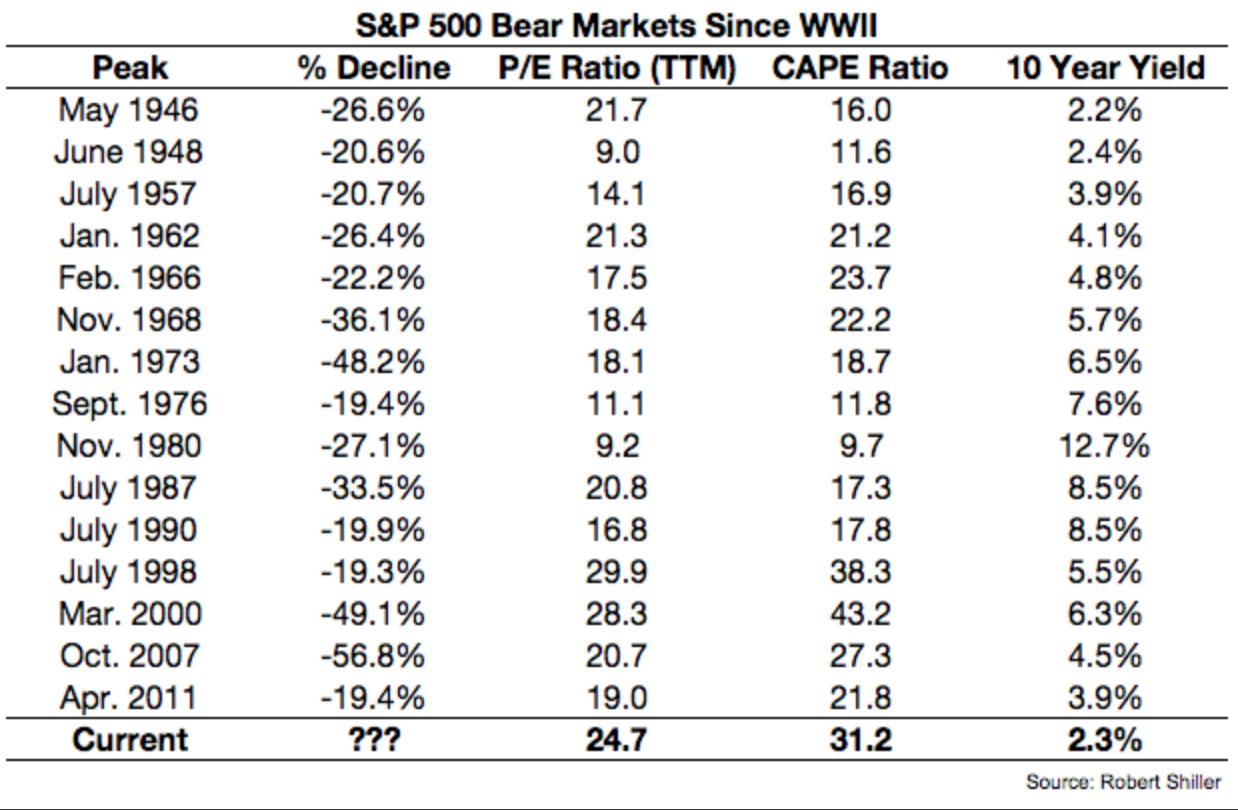

Similarly in equity markets, there will always be risks which are not under our control and can’t be foreseen. Negative unknown events can hit valuations at any point in time and cause them to go down further. Even if valuations are low, there can still be a sharp fall as the emotions can go from pessimism to extreme pessimism.

As seen in US markets, bear markets can also start at low valuations.

Lesson 2: Accept humbly that you and I won’t be able to predict every major risk out there. A large correction once in a while will definitely happen.

Accidents under our Control

Now before we give up completely, hang on.

While there are risks which we don’t have control over, this doesn’t mean we become complacent and paint every risk with the same brush – unpredictable risk. In reality, a lot of risks are still under our control or can be managed.

In my college years, there were those occasional times when I used to drive back to my hostel drunk. The fact that the outcome turned favorable, doesn’t mean that the risk was not there. If I had continued that behavior on a regular basis, most likely I might not be writing this post.

Similarly there are several other risks such as over speeding, rash driving, driving when you are sleepy, talking over the phone while driving, texting while driving, triples in bike etc which are risks completely under our control. Yet we do indulge in these risks time and again.

Applying the same analogy, just like there are risks that cannot be known, there are also known risks which can be evaluated and identified in equity markets.

Most of these known risks stem from repeated patterns in human behavior.

So instead of taking a black or white approach to predict or not to predict, I would prefer a grey area approach, where the idea is to try and manage for known risks while acknowledging the fact that once in a while extreme events will happen and can’t be predicted.

The market goes through cycles – Bull, Bubble, Bust, Best. While I won’t be able to predict the markets, I prefer to prepare by identifying in which part of the cycle are we currently in.

The big errors are usually made during the Bubble phase which carry over to the Bust phase. The Bubble phase is where several of our emotional biases combine together. Greed, Overconfidence, Illusion of control, Herding, Fear of missing out, Envy combine together to form a lethal combination. The market also shows bubble signs in terms of high valuations, high earnings growth, euphoric sentiments, high flows from FII and DII etc.

This is a phase where the risk is at its highest and hence we must cut risk. But given the strong push from our behavioral biases, we end up increasing our risks.

Of course the identification of a bubble in not a precise science. But nevertheless a reasonable framework which gauges the valuations, earnings growth, sentiment and macro can give us a good sense of where we are in the cycle. You can check how I go about with this here

Similarly, we can build different frameworks to check risks in various market cap segments (mid cap, small caps etc), sectors, stocks, debt funds etc. You can check my earlier post on how I used frameworks to identify risks in mid and small cap segment (link) and credit risk segment (link).

Lesson 3: There are risks that can be evaluated and managed. Understanding and evaluating where we are in the cycle remains the key.

Putting it all together

- There are small but regular corrections all equity investors will have to withstand. These are not predictable and not under our control.

Translation to my portfolio: On a 6 month time frame, a decline up to 30% in equities would be considered normal - Sometimes, there might be major corrections, due to some unknown-unknowns.

Translation to my portfolio: I am mentally prepared for a 50%+ decline atleast once every decade. Though I will attempt at controlling the known risks, there will be many times I won’t be able to see the risks. I will have to be humble and accept this as an emotional cost to be paid for investing in equities. A “what-if-things-go-wrong” plan will be used to address this (link). - There are risks which can be evaluated and managed.

Respecting Equity markets cycles: While I wont be able to predict, I will try to prepare by identifying which part of the cycle the market is currently in. I will use this framework for evaluating the markets. When markets enter a bubble zone, I will attempt to reduce risk and will increase equities when market enters the “Bust” and “Best” zone. Now how successful I will be in identifying the cycles, only time will tell. But the idea of me publishing the framework, is for me to go back and check as to what went right and wrong. Thus the framework will gradually evolve over a period of time as we improve based on feedback. - The above thinking translates into my Asset Allocation Framework

- A portion of equity allocation will take the view that markets can’t be predicted and will always remain – Buy and Hold

- For the remaining portion, my framework will reduce equities in Bubble zone

- This will involve the use of trend following strategies (switched on only in Bubble Phase)

- The debt portion and the trend following portion, will be used to increase equity allocation during a bear market

- Increase in Equities during a bear market will include few moves but significant ones (instead of too many moves at small increments)

- Given the usual behavioral flaws, I have designed the portfolio in such a way that, even if I fail to act in a bear market, still the solution will do well as I have automated a part of the decision making. But if I get my act together, and execute as per my plan, the solution can do even better!

- Someday in future, I will explain my whole asset allocation framework in detail

- If you are young, just ignore this entire post as noise. All you need is to save more and invest every month.

- This framework is more relevant to people who have already accumulated decent amounts of money and for whom large declines may lead to loss in sleep.

In the next week, we will apply this thinking and revisit our framework for evaluating market cycles.

If you loved this post, share it with your friends and don’t forget to subscribe to the blog (1 article per week) or Twitter along with the 6000+ awesome people. Look out for some fresh, super interesting investment insights delivered straight to your inbox.

P.S

One small request. I have been trying to do away with the ads in my blog and hence planning to move to a direct reader pay-if-you-like-the-post model. If you found this post useful you can convey your love and support by sending Rs 25 bucks or more to my

UPI account: rarun86@okhdfcbank

You can also follow me on twitter

Check out my other articles here

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments.