If you have been following my debt fund related posts, you would have noticed that I generally tend to avoid credit risk in debt fund portfolios. In today’s post we will explore the thought process that goes behind my decision to avoid credit risk.

If you are new to the blog, you can go through my earlier post here to get an understanding of credit risk in debt MF portfolios.

What is a credit fund?

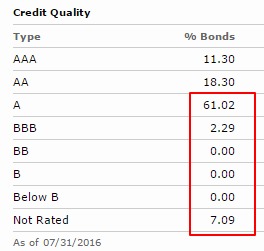

Credit funds are basically debt mutual funds which lend a major proportion of our money to relatively riskier corporate companies and in turn earn higher interest rates for us. So when you look at the fund portfolios, you will see a relatively larger proportion of debt papers which are rated below AA. (Credit rating is an indication of the underlying company’s health and its ability to repay its debt. The lower the rating, the lower are its chances to repay its debt on time.)

Eg Franklin India Dynamic Accrual Fund

Higher proportion of “below AA” rated papers..

Source: Morningstar

which helps in providing higher interest rates..

See that.. a whopping 10.87% compared to a current YTM of ~7.5-8% for most of the short term funds which invest in high quality papers (i.e predominantly AAA rated papers). These funds generally have Yield to Maturity (i.e interest rate return) which are 1 to 2% above short term funds which invest only in high credit quality papers.

Credit funds generally invest in short maturity papers between 1-3 years and the modified duration is mostly around 1-2 years. Thereby the “interest rate” risk taken to improve returns is kept at moderate levels and these funds primarily depend on the “credit risk” taken to generate additional returns.

The basic idea behind credit funds is that – by deploying their own analysis to these lower rated papers, the fund management research team would be able to identify certain companies which have much better health (than evaluated by credit rating agencies) or is expected to improve and hence the company’s ability to repay its debt is much better than perceived. This allows the fund to benefit from higher interest rate paid by these companies provided the fund manager’s evaluation is correct and the underlying companies to which they have lent repay their debt and interest on time.

Certain fund houses also take sufficient collaterals (in the form of covenants, shares, real estate securities etc) to offset the losses if there is a default from the issuer. Some have inbuilt agreements for priority in repayments to ensure that they exit when they see any small sign of distress.

Credit funds generally come under different names such as accrual funds, corporate bond funds, credit opportunities funds, income opportunities etc. If you need to know the subtle difference refer here. Given so many confusing names used to refer to various credit fund schemes, the best way for us will be to check for the credit quality of the underlying portfolio and decide 😦

The chances of us getting attracted to credit funds is very high given 2 reasons:

- Higher past returns compared to short term funds in the recent past

Source: Valueresearch

Source: Valueresearch

- Expense ratios are higher and hence more incentive for advisors to sell these funds to usExpense ratios compared to short term funds are higher by atleast 0.5 to 0.8%.

Now the key is to understand the underlying risk behind the higher returns..For that we need to find the answer to a simple question.

What happens when some of the underlying borrowers get downgraded in terms of credit rating or worst case, default and do not repay the interest and borrowed amount?

For the purpose of understanding, let us hypothetically assume that, a credit fund has lent our money out to 20 corporate borrowers equally and has 5% equal exposure to each debt security. Now assume that the financial health of one particular company to which the fund has lent starts deteriorating and hence its chances of paying back its borrowing and servicing interest reduce. Usually the credit rating agencies evaluate this scenario and reduce the rating provided to the company. This is technically called a credit rating downgrade. To understand better, you can check the actual Amtek Auto downgrade credit rating reports here and here.

This leads to an immediate price drop for the debt security of the company. Logic being lower rated papers will need to have a higher interest rate given the reduced rating and higher risk. But as the underlying interest payment for a debt security is prefixed, the prices of the debt security will have to adjust (in this case, decline to a certain extent) to match with the higher interest currently demanded by the new investor.

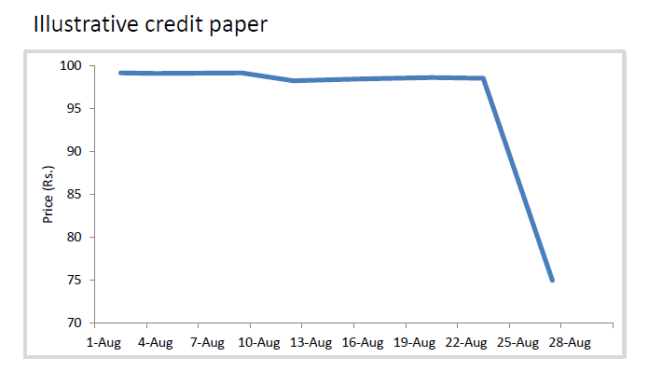

This is an impact on a paper which was downgraded from AA- to C. Below chart data is only for illustration purpose.

Source: Axis Mutual Fund Presentation (Link to presentation), CRISIL/ICRA.

Now while the exact decline in prices would be dependent primarily on the nature and severity of downgrade, going by past history, we will assume that approximately 30-50% of the debt security price will get eroded under a credit downgrade situation. This will mean that there will be a negative price impact of -1.5% to -2.5% in the fund (30% to 50% decline on a 5% allocation). Worst case if it is a default then the entire 100% of the security holding will have to be written off i.e 5% decline for the fund.

This risk is called credit risk and as seen above is very simple to understand. At the first look, it seems like an “ok” kind of risk to take provided we ensure that the fund is adequately diversified among many borrowers and the additional returns (which we get more often than not) are high enough to compensate for the risk taken. Credit downgrades and defaults are not very frequent. And even assuming the fund manager gets 2 calls wrong and has 2.5% exposure each, the overall downside may be around 1.5% to 2.5% on the NAV. But if everything goes right we end up making around 1-2% extra returns.

All fine till now. But unfortunately, there is another risk which we have forgotten to take into account. Liquidity risk. What the heck is that??. In simple words, it means that there are not enough buyers, so even if there is a price being theoretically quoted, finding a buyer at the quoted price is not easy (think of real estate).

This is precisely, in my opinion, the biggest issue when it comes to credit funds. Indian bond markets are still underdeveloped and most of the lower rated papers are extremely illiquid which means they are extremely difficult to sell in bad times.

Let’s listen to what the great investor Mr Howard Marks has to say about liquidity..

“Usually, just as a holder’s desire to sell an asset increases (because he has become afraid to hold it), his ability to sell it decreases (because everyone else has also become afraid to hold it). Thus (a) things tend to be liquid when you don’t need liquidity, and (b) just when you need liquidity most, it tends not to be there.”

If you have some time, do read his entire writing here . Trust me. It will be well worth your time.

Think of it this way. On one side you have the lender (that is us who have invested in the fund) who can take out money anytime and on the other side the fund has invested in a few illiquid debt securities which cannot be immediately sold off in the market. Now if due to some reason (generally a credit downgrade or default event) a lot us panic and decide to take our money from the fund you can imagine the plight of the fund. The fund may get stuck with the downgraded paper and be forced to sell its more liquid holdings as there is a rush to redeem units. And as the pace of redemptions increase, both its security selection and its portfolio concentration can go completely out of whack leaving the existing investors with a far more riskier portfolio for no fault of theirs. And there lies the crux of the entire problem!!

Let’s get back to our earlier example where the fund has lost 1.5% due to 30% decline in one debt paper which was earlier 5% of the overall portfolio (now the same paper would be ~3.5% of the portfolio). Generally, the biggest investors in debt mutual funds are the corporates. They have large treasury teams who are in charge of the investments and keep monitoring every fund day in and day out. Now they realise that 1.5% knock is fine, but if the paper defaults then it will lead to an additional loss of the remaining 3.5% in the debt paper. So they decide to take their money off. Now every other corporate and savvy investors do a similar sort of calculation and decide to pull off the money before the situation worsens. So suddenly there is a large amount of people removing their money from the mutual fund (called redemption pressure). Now the fund manager unfortunately is not able to sell off the downgraded debt security as its difficult to find a buyer even even at its so-called market value. So the fund manager has no choice but to sell the high quality debt papers which are liquid. Now assume the redemptions are large and almost 50% of the fund money is taken out (I am exaggerating but you get the point). Now all this while the dumb me who is also the investor in the fund remains blissfully unaware of all this happening and see my fund’s portfolio after a month. I am shocked to see that now I am stuck with not 3.5% of the original downgraded highly risky paper in my portfolio but rather 7% of the same security in the portfolio as the 50% of the liquid higher rated debt securities of the fund is already sold. And my existing fund portfolio looks a whole lot different with most of the high rated and liquid securities being sold off. Oh shit how unfair.

Relax. The fund house obviously realizes this and tries to address this by two ways

- Side Gate – The fund simply doesn’t allow anyone to take their entire money out. It puts a restriction on the amount an investor can redeem from the fund. Now if that sounds ridiculous and completely unfair. Read here to see what happened to two credit funds managed by JP Morgan when one of its debt security Amtek Auto got downgraded. And remember my rant about the corporates being the smarter and more resourceful guys. Go on check this link.

Recently the market regulator SEBI obviously concerned by the proceedings, post this event, has put in a new rule that, even in case of a systemic liquidity crisis, no redemption requests of up to Rs.2 lakh can be subject to restrictions. For redemption requests above Rs.2 lakh, AMCs will redeem the first Rs.2 lakh without restriction while the remaining money can be subject to any restriction imposed by the AMC. Further, restrictions on redemptions can be imposed only for a specified period of time that cannot exceed 10 working days in any given 90-day period.

- Side pocket – The fund simply isolates the affected portion as a separate fund with a seperate NAV. So except for the affected portion you are free to redeem the remaining portion if they want. The proportion of investor money (in the scheme) linked to stressed assets gets locked until the fund recovers dues from a stressed company.

Out of these two options, “side pockets” seem like a better option as explained here. The argument goes like this – the side pocket concept would provide the required liquidity to the investor and ensures that their entire money is not stuck. Further it also ensures that the early sellers in the fund do not benefit at the cost of the remaining investors.

Now the only flipside is the subtle unintended consequences. A fund manager who knows that the side pocket option is not available will be forced to be much more prudent and aware of the risks he is taking. If the option of a side pocket exists, then the fund manager may venture out to take unwarranted higher risks to provide higher returns as anyway they can use a “side pocket” if something goes wrong.

For once, the regulator SEBI also seems to share my concerns and post the recent JP Morgan – Amtek Auto debacle has warned against the future usage of side pockets by Indian mutual funds (see here)

So adding to the problems, the funds from now on cannot use the side pocket option in future and the side gate option also has several new restrictions imposed by SEBI. This means the credit funds will find it more difficult to handle redemption pressures if at all it arises. And since the side pocket option is not there, investors will want to exit as fast as possible fearing possible “redemption freeze” scenario which ironically will only exacerbate the redemption frenzy. Phew.

Assuming you survived the post till here, the simple summary is that more than the credit risk it is actually the liquidity risk which is the real problem in credit funds.

Since these credit events are not very frequent, the bigger risk is that we may tend to under appreciate the very nature of risk!!

Now my thought process has always remained very simple. From heart I am an equity guy. All my chase for returns happens in equities. Debt funds personally has always been about safety. A few percentage plus or minus in debt returns, really doesn’t make a huge difference to me.

My primary usage of debt fund is a parking space for near term needs and as a part of my asset allocation strategy (i.e changing the mix of equity and debt based on valuations). So typically I will be needing this debt money desperately to buy equities when there is a crisis and equity markets have crashed (now whether I am able to pull it off in reality is a different issue). The last thing I want is for my debt fund to say that “Sorry boss, we have stopped redemptions due to a liquidity crisis”. Credit funds given their inherent structure have a high probability of getting screwed up in these scenarios. So my simple laymanistic reasoning being – why take so much tension for debt returns. As it is equities give me enough of it, but at least the long term payoff is worth the pain 🙂

As always, investing is a very personal thing and you are free to invest in credit funds but please ensure that you are not buying only because of the past returns and make sure you really understand the underlying risks (especially the liquidity risk).

Happy Investing 🙂

“Now my thought process has always remained very simple. From heart I am an equity guy. All my chase for returns happens in equities” Exactly my opinion on debt investment, I prefer to protect my principal that additional returns. Though however, I’m for the return chase philosophy by investing in securities which may be re-rated. The investor and his advisor ought to be aware of the implications of the risk event on their portfolio.

LikeLike

Hi Obu .. Good to hear from you.. As you mentioned as long as the investor is aware of the issues that may crop up in case of a credit event it is fine .. The problem is most of them are lured just seeing the returns

LikeLike