Why did I avoid Credit risk funds?

I had previously communicated my views on Credit risk funds here

- Credit funds – Don’t count your returns before they hatch (Link)

- Here’s why I don’t invest in credit funds (Link)

- Debt Funds – Revisiting the framework (Link)

The gist was, I would be avoiding credit funds as I was concerned on 3 fronts

- Liquidity – Since the underlying market for lower rated bonds in India is extremely illiquid, the ability of a fund manager to manage risk based on evolving views (by reducing or exiting the bonds), is severely limited

- Outrageous Costs – The expense ratios are usually significantly higher for credit risk funds – mostly eating away a significant portion of the extra return potential

- Not a good diversifier to equities during downturns: The driver of equity risks and credit risks are very similar. During bad markets in equities, when you want to rebalance and move from debt to equity to take advantage of lower valuations, credit funds might be in trouble themselves leading to loss of rebalancing opportunity

Now if you noticed the last three points, it looks like I am missing out a very obvious risk. Any guesses?

Yup! Credit risk in the form of downgrades or defaults.

Credit risk is not the real risk

This was intentional. To be honest, I think this is not a risk for which you avoid the category.

It is obvious that if you are buying a credit risk fund, downgrades should be a normal part of the course and defaults while rare will happen once in a while.

Theoretically, if your Net YTM (read as YTM post the expense ratio) is 2-3% above the Net YTM which you would get in a High Quality Short Term fund, then even if your fund loses 2-3% due to downgrades/defaults every year, you should still be fine.

You will end up with returns similar to the high quality short term funds which was your initial alternative.

As long as the fund is well diversified across sectors and companies with smaller allocations across several companies things should be fine. In fact we can also further diversify from our side by using 2-4 credit risk funds which are well diversified and not so concentrated.

Post the recent credit events, most fund houses have taken cognizance of the concentration risk and going forward I expect most of the funds to have far lower concentrations risks.

But, the real risk lies in..

So the next time, somebody is scaremongering citing a downgrade or default in your credit risk fund, logically as long as the percentage of exposure to the affected paper is low, you should be fine.

Buy wait. Unfortunately this is also where we have the possibility of the scariest risk playing out.

Remember our first risk – liquidity risk. This can be the killer!

While you may choose to remain sane and logical, you cannot expect the same out of other investors.

What if many of them panic and suddenly start redeeming from the fund due to default/downgrade concerns?

The fund manager now suddenly has to sell his underlying bonds to provide money to the redeeming investors.

Given that most of the lower rated papers can’t be sold as they are illiquid, he will be forced to sell his more liquid higher quality papers. This gradually leads to much higher concentration in existing lower quality papers with lower liquidity which he is not able to reduce/exit.

Now as you remain calm and relaxed knowing that few credit downgrades and defaults are more than compensated for by your higher Net YTM, you are in for a shock.

In a few months, what seemed to be a reasonably well diversified portfolio when you bought, has become a high risk, concentrated portfolio of low quality papers.

So the key point for you is:

If other investors panic, what was otherwise a reasonably well diversified credit risk fund can suddenly become a high risk high concentration fund with significant exposure to lower rated papers.

Sounds too theoretical. Let us take a live example of a fund where the above risks are currently playing out.

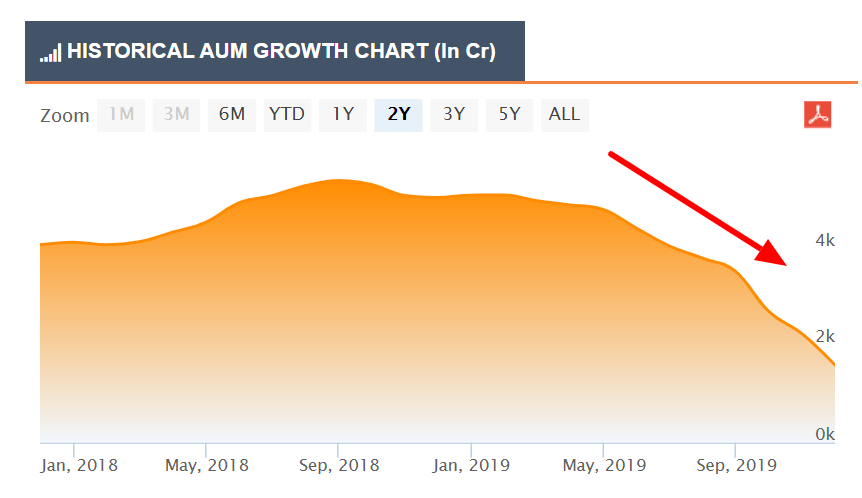

What is happening to UTI Credit Risk Fund?

The fund has been impacted by two major credit events during the year..

As expected there has been heavy outflows from the fund..

Source: Fundzbazar

The fund’s AUM has dropped from Rs 4,983 cr on 28-Feb-19 to Rs 1,596 cr on 31-Nov-19. This has further dropped to Rs 1,473 cr as on 20-Dec-19!

That is a whopping 50% outflows in a such a short period.

Based on our logic, this means due to low liquidity the fund should most likely end up with a far concentrated and higher risk portfolio.

Let us test if our intuition is right..

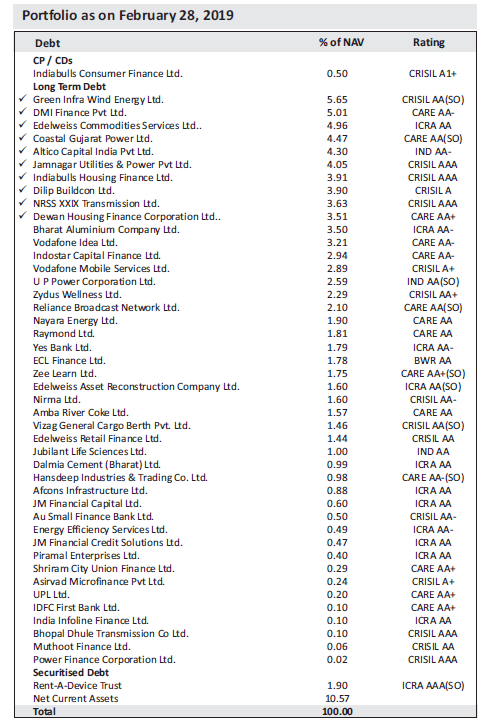

How did the portfolio look like in Feb-19?

How did the portfolio look like in May-19?

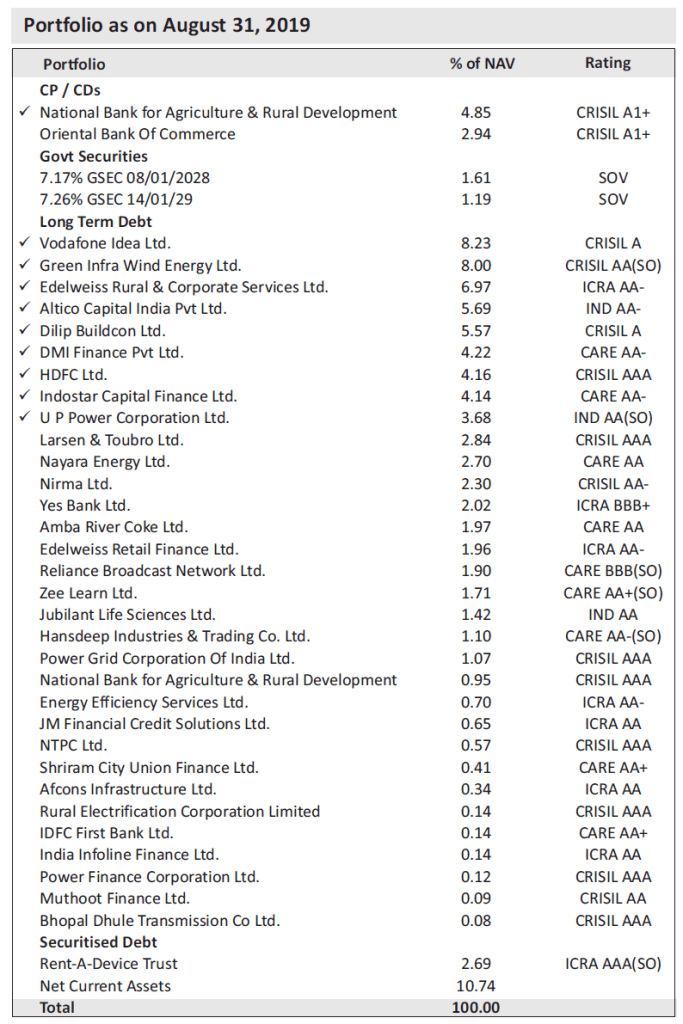

How did the portfolio look like in Aug-19?

How did the portfolio look now in Nov-19?

Saw that?

- Vodafone Idea is at 15.7%. In Feb, it was only at 6.1%!

- Dilip Buildcon is at 11.4%. In Feb, it was only at 3.9%!

- DMI Finance is at 9.4%. In Feb, it was only at 5.0%!

- Indostar Capital Finance is at 9.1%. In Feb, it was only at 2.9%!

- Nayara Energy is at 6.0%. In Feb, it was only at 1.9%!

- Yes Bank is at 4.5%. In Feb, it was only at 1.8%!

You get the drift.

While the fund manager has not bought additional exposure in these papers, the huge redemption and the underlying illiquid nature of these papers has forced him to sell out of the other liquid names, leading to significant unintended concentration risks for existing investors.

This is precisely why I am super scared of this category.

The biggest risk is always about other investors panicking out. Then you have no choice but to act fast as otherwise you are left with a far riskier portfolio for no fault of yours.

Imagine a crisis scenario like 2008. While your equity portfolio is getting hammered, the last thing you want to deal with is your debt portfolio also getting into trouble.

The above example is a live case of how the fund manager and you end up with far more concentrated higher risk portfolios unintentionally, due to other investors panicking out of the fund.

Now for those who think I am getting overly worried about liquidity risks, google and find out what happened to investors invested with one of UKs most popular equity fund manager Neil Woodford (once referred to as “Britain’s answer to Warren Buffet”). Here is the link.

If this can happen in a developed market like UK, then we obviously need to be worried about this from an Indian context.

Earlier I had provided my debt fund evaluation framework

- Net YTM = Yield to Maturity – Expense Ratio

- Credit Quality: % of government, AAA and AA rated bonds

- Modified Duration

- Average Maturity

- Size – Higher the better + check for sharp fall

- Exit Load

- Historical NAV movement graph

- Past Returns

- Concentration Risk – check for no of securities above 5% allocation (especially non AAA) and group exposure above 5%

- AMC Reputation and Track Record

Improving the existing debt fund evaluation framework

While I did include asset size trend as a parameter, I honestly didn’t know it was this critical a risk factor to monitor.

So I will be improving on this framework, by adding more stringent checks in the asset trend.

If the asset outflow for a month is greater than 5% in a month – this calls for preliminary investigation.

If the asset outflow is sharp and greater than 20% within the last 6 months, this usually indicates that investors are panicking out and this becomes a red flag to immediately evaluate exiting the fund.

This becomes more critical if the fund is credit risk oriented fund.

The best part is now we also have access to daily AUMs of the funds and don’t need to wait till month end.

You can check this data for any fund from AMFI website – Link

New Debt Fund Framework

- Net YTM = Yield to Maturity – Expense Ratio

- Credit Quality: % of government, AAA and AA rated bonds

- Modified Duration

- Average Maturity

- Size – Higher the better + check for sharp fall (5% in a month and 20% within 6 months)

- Exit Load

- Historical NAV movement graph

- Past Returns

- Concentration Risk – check for no of securities above 3% allocation (especially non AAA) and group exposure above 5%

- AMC Reputation and Track Record

Parting thoughts

Summing it up, I will continue to avoid Credit Risk funds at the current juncture and will change my view if

- Liquidity situation for low credit papers improves in India

- Funds start disclosing individual paper YTMs in fact sheet (so that I can check if one or two papers with extremely high YTMs is not skewing the overall portfolio YTM)

- Net YTM is 3% more than Net YTM I get in short term high quality funds

- Expense ratios become reasonable

- 2-3 decent credit risk fund options are available to diversify

- I don’t need that portion to re-balance back into equities

There are few other funds going through similar problems, make sure you have a word with your advisor and ensure you are not into one of these funds.

As always Happy Investing 🙂

If you loved this post, share it with your friends and don’t forget to subscribe to the blog (1 article per week) or Twitter along with the 8000+ awesome people. Look out for some fresh, super interesting investment insights delivered straight to your inbox.

You can also check out my other articles here

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments.

Excellent write up Arun. Thank you mashe.

On Sun, Dec 22, 2019 at 12:28 PM The Eighty Twenty Investor wrote:

> Arun posted: ” Why did I avoid Credit risk funds? I had previously > communicated my views on Credit risk funds here Credit funds – Don’t count > your returns before they hatch (Link)Here’s why I don’t invest in > credit funds (Link)Debt Funds – Revisiting th” >

LikeLike

Thanks for the very simple to understand article.Easily understood. No clutter, no big phrases,no big sentences. You have the gift of gab and knowledge of the subject.

Keep it up.

LikeLike