Franklin India Ultra Short Bond Fund has been one amongst the popular debt funds in India and has a had a long runway of strong performance.

The fund while it belongs to the Ultra Short Term category was run as a quasi credit risk fund with high exposure to lower rated debt securities for providing extra returns.

I had written about why I am not too big a fan of the credit strategy in my earlier articles

- Credit Funds – Don’t count your chickens before they hatch – Link

- Here’s why I don’t invest in credit funds – Link

- Debt Funds – Revisiting the framework – Link

In a recent article, I had also discussed on why the real risk in credit funds is not weaker credit quality but actually liquidity risk (read as you can’t sell the lower rated papers easily)

- This Might Be The Scariest Thing You Heard About Credit Risk Funds – Link

Ok. Enough about the past.

What happened now?

Recently Franklin India Ultra Short Bond Fund had written off its entire exposure in Vodafone Idea debt security (~4.3%) on increasing concerns of a possible default (due to supreme court rejecting the plea to reconsider its judgement regarding Adjusted Gross Revenue (AGR) related payments for telecom companies).

This led to a one day fall of 4.3% in its NAV!

For the last few years, there were no instances of major defaults in the fund and hence there was a perception that the fund always provides higher returns without risk.

Now suddenly as the risk has finally played out, everyone has shifted their focus on “credit risk” and perceive the fund to be “very risky” all of a sudden.

This approach of looking at only risk or return without considering both together is detrimental to us as investors.

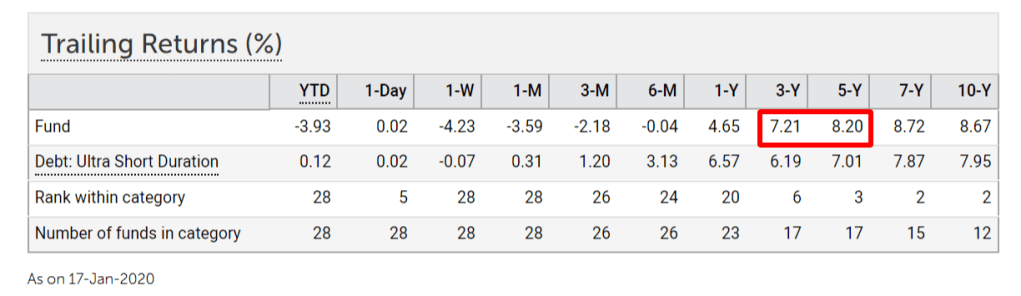

Returns in the context of risk taken..

Let us see how the returns fare in the context of the risk that has played out..

Despite a 4.3% fall in the fund NAV, check out the 3 year and 5 year returns

The returns still seem to be decent.

This in other words is the closest we get to appreciate and understand the otherwise too theoretical term – “risk-adjusted-returns”.

The fund because of the risks it took by lending to lower rated companies, was able to receive higher interest rates which was reflected in the higher YTM (Yield To Maturity) of around 1-2% compared to other 100% AAA oriented debt funds.

Now in simple terms it means that even if there is a default of around 1-2% every year you will end up with more or less the same returns as the AAA funds.

So despite the 4.3% write off, the fund is still able to pull off a decent 3 and 5 year return.

So the first simple take away is that

In a credit risk fund, downgrades and defaults are not a bug but a feature.

Now the choice of a credit fund (if at all you decide to invest) has to be based on

1) Margin of safety via the higher Net YTM over 100% AAA fund

2) Your evaluation of the fund manager’s ability to manage the default/downgrade risks (don’t assume the fund manager to have zero defaults – but rather evaluate if he/she will be able to contain it at a lower level compared to the extra Net YTM potential)

Under this framework, Franklin India Ultra Short Bond fund writing off one of its security is still fine. I mean it is the risk that you took for higher returns but the risk has played out instead of returns. This is perfectly normal.

This is also precisely why, the fund manager diversifies across various companies – to manage the risk of defaults or downgrades.

How should you evaluate your current holding?

You can evaluate the rest of the portfolio holdings (as anyway the Vodafone Idea exposure is marked down to zero) and if you think the risk in other securities are fine, your earlier thesis of investing in this fund should logically still hold.

However if you think there are concerns with other securities and it is not adequately compensated by the extra Net YTM then you should immediately exit.

So far so good. Simple plain vanilla analysis.

But wait.

Here comes the killer.

What if other investors panic and start redeeming their funds?

A few minutes spent on twitter or reading media articles and you will know why this can be a possibility.

The fund manager now suddenly has to sell his underlying bonds to provide money to the redeeming investors.

Given that most of the lower rated papers can’t be sold as they are illiquid, the fund manager will be forced to sell his more liquid higher quality papers. This gradually leads to much higher concentration in existing lower quality papers with lower liquidity which the fund manager is not able to reduce/exit.

Now as you remain calm and relaxed knowing that few credit downgrades and defaults are more than compensated for by your higher Net YTM, you are suddenly in for a shock.

In a few months, what seemed to be a reasonably well diversified portfolio when you bought, has become a high risk, concentrated portfolio of low quality papers.

So the key point for you is:

If other investors panic, what was otherwise a reasonably well diversified credit risk fund can suddenly become a high risk high concentration fund with significant exposure to lower rated papers.

Then you have no choice but to act fast as otherwise you are left with a far riskier portfolio for no fault of yours.

In fact if you really think about the reason why the AMC wrote it down much before the rating agencies, they must obviously be as worried about the liquidity risk as we are.

The smart money would have moved out immediately leading to a possible “run on the fund” if they hadn’t done this move.

What to do now?

For the next few weeks, keep a watch on the outflows for these affected funds.

You can check this data for any fund from AMFI website – Link

If there are excessive redemptions exit as soon as possible.

So the key is to monitor two critical variables and take a decision:

- Outflows for the next few weeks

- Credit Risks in remaining portfolio

Parting Thoughts..

Credit defaults and downgrades are perfectly normal for a credit risk fund.

But the underlying illiquid market for lower rated securities, can blow up this otherwise normal risk into a significant crisis for the fund if investors panic and start redeeming.

In a world of social media, panic can spread faster than we imagine.

Keep a watch on the outflow trend!

Now if you are wondering, why should I go through all this trouble for an extra few bps, the honest answer is –

“You need not!”

As always Happy Investing 🙂

You can also share your feedback or queries at rarun86@gmail.com. Not that I have got it all sorted, but I maybe of some help:)

If you loved this post, share it with your friends and don’t forget to subscribe to the blog (1 article per week) or Twitter along with the 8000+ awesome people. Look out for some fresh, super interesting investment insights delivered straight to your inbox.

You can also check out my other articles here

Disclaimer: All blog posts are my personal views and do not reflect the views of my organization. I do not provide any investment advisory service via this blog. No content on this blog should be construed to be investment advice. You should consult a qualified financial advisor prior to making any actual investment or trading decisions. All information is a point of view, and is for educational and informational use only. The author accepts no liability for any interpretation of articles or comments on this blog being used for actual investments.

Tha is for this article. I have always loved the way you explain concepts and issues like these.

LikeLike

Thanks a ton Shashi. Gald you found it useful 🙂

LikeLike

Thanks

LikeLike

This in other words is the closest we get to appreciate and understand the otherwise too theoretical term – “risk-adjusted-returns”.

In a credit risk fund, downgrades and defaults are not a bug but a feature.

EXCELLENT, Arun !!

LikeLike